One of the most provocative sessions at last week’s Schwab Impact conference was given by Dan Ariely, who deftly summarized his current research in the important field of behavioral finance. Ariely is a professor of economics at Duke University and a visiting professor at MIT’s Media Laboratory. He is also the author of the popular book, Predictably Irrational.

Ariely’s message was that, no matter how good their intentions or how deep their experience, people – investors specifically – consistently make the wrong decisions. They behave irrationally, and predictably so.

Advisors who understand the natural biases in individual behavior can frame questions that will steer their decision-making process in a more rational – and economically better – direction.

How to remove a bandage

While serving in the Israeli army, Ariely was injured in an accident and suffered third-degree burns over 70% of his body. A painful aspect of his long recovery was the process of nurses repeatedly removing and replacing the bandages that covered his wounds, in sessions that often lasted an hour.

His nurses removed his bandages as quickly as possible, leaving Ariely to question whether removing them slowly and methodically would be less painful.

His experience inspired him to conduct a series of experiments into the psychological effects of enduring pain. He found that:

- Prolonging a painful experience does not make it much worse; it is changing that amplitude of pain that makes the experience much better or much worse

- Pain that starts at a low level and gets high is much worse than the reverse

- It’s good to take breaks when dealing with pain, to provide a chance to recuperate

The nurses were wrong, despite having their years of experience and good intentions.

Ariely’s subsequent research has focused on understanding why people make consistently wrong decisions, in spite of conclusive evidence that should lead them to the correct decision.

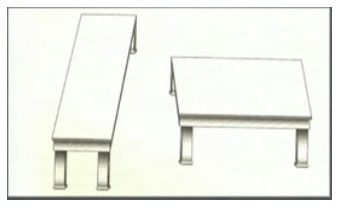

Optical illusions and the power of the default option

Ariely showed the audience a familiar optical illusion, asking them whether the length of the table on the left is greater than the width of the table on the right: :

The audience’s selections mirrored the results in Ariely’s experiments showed that people consistently chose one table over the other, despite the fact that both are the same length. “Your brains are fooling you in a repeated, systematic way, and they are doing the same for everybody,” he said.

Vision is one of our most reliable senses; it occupies a significant portion of our brains and we use it constantly throughout the day. Investors make decisions far less frequently and subconscious biases that operate in the context of complex financial choices can lead to even more frequent wrong decisions and, consequently, economic harm, Ariely said.

For another illustration, Ariely showed why organ donor participation rates are strikingly different among European countries. Those countries that present an opt-out choice (e.g., “check this box if you don’t want to participate in the program”) have far higher participation rates than those countries where participants have to check a box to opt-in.

“We think we are making decisions, but they are largely decided by the design used by the person presenting the choice,” he said.

In another study, a group of doctors had to decide whether to call back a hypothetical patient they had previously referred to a hip replacement surgeon. After they made the referral, they were told they had forgotten to try additional medications before recommending surgery. Some doctors were told that they could tell the patient to first try only one other medication, while the other group was told that they could tell the patient to first try one of two other mediations.

In the first case, the majority of doctors said they would call the patient back and have them try the additional medication. In the second case, the majority would not call the patient back.

“The more complex the problem, the more likely we are to choose the default option,” Ariely said, even though the right decision was clearly to try additional medications.

Default options are enormously powerful, especially in situations involving complex or difficult decisions.

Ariely offered one other experiment to illustrate the power of default options. Consumers in a supermarket were offered the chance to try different jams. In one scenario there were six different jams on the display table; in the other there were 24.

The researchers recorded the percentages of people that approached the tables, tried the jams, and purchased a jam:

| |

6 jams |

24 jams |

| Approached the table |

40% |

60% |

| Tried a jam |

1.4 |

1.5 |

| Purchased a jam |

30% |

3% |

Presenting only six choices instead of 24 made it ten times more likely that someone would purchase a jam. In fact, 3% is the rate at which people bought jam if there was no display table. Overwhelming customers with 24 options totally negated the enticing effect of offering a free sample.

When presenting clients with investment options – a choice among mutual funds, for example – the greater the number of choices, the more likely it is that the client will not do anything, Ariely said.

“Defaults are neither good nor bad,” Ariely said, “it’s a question of how to use them.”

“If you take the ideas of default and complexity, and look at how these work together as the decision becomes more complex, the default becomes more likely,” he said. In the world in which advisors operate, almost all decisions are complex, making the power of the default option even greater.

The architecture of choice

Ariely asked half the audience to come up with three reasons why they loved their significant other, and the other half to come up with 10 reasons why they did. Those in the latter group had a much harder time coming up with reasons.

If you make the question too difficult, people won’t try to answer it.

The same thing happens when you ask people for 10 reasons to buy a BMW, for good reason: “There aren’t 10 reasons,” Ariely said.

For advisors, the implication is that questions for clients should be framed with the least number of applicable answers. “If you think about the process by which people come up with answers, and understand how central this process is to the answer they come up with, you will think very carefully about how to customize choices for your clients,” Ariely said.

Presenting choices in scale – such as asking a client to rank their risk tolerance between 1 and 10 – can lead to misleading outcomes. For example, assume people are asked how often they floss their teeth.

In the first case, they can choose from a scale of daily, starting with 1 on the left and increasing to “10 or more” on the right. In the second case, they can choose from a monthly scale with the same choices. Someone who flosses daily will choose the left-most option on the first scale, but someone who flosses only every other day will choose the right-most option on the second scale. In the latter case, the person might easily conclude that they don’t need to see a hygienist, since they are at the right, most extreme end of the scale, and the in the former case the person might conclude the opposite.

“The scales that we use to get people to think about problems influence greatly what they end up deciding,” Ariely said.

The decoy effect

In another experiment, people were offered either a free trip to Rome or a free trip to Paris. A second group was also offered a third choice – also a free trip to Rome, except that it did not include coffee in the morning. This third choice is a useless option and should not affect the decision to go to Rome or Paris.

The useless option, however, greatly influences behavior – people in that group chose Rome far more frequently (with the morning coffee).

It turns out that a great way to influence decisions, especially between two alternatives, is to present a third alternative similar but clearly inferior to one of the choices. That choice will then more likely be selected.

“When we face a situation we focus on those things that are easy to compare,” Ariely said.

Ariely illustrated this effect in an experiment where women were asked which of two men they found more attractive. When a third choice was introduced – a picture of a man identical to one of the two choices but with an unattractive feature added – the women chose the man similar to the third choice, but without the unattractive feature.

We often have a view that we can ask questions and people “open a drawer” revealing their attitudes, Ariely said. “But in most cases people have no idea what their attitudes are.”

Moreover, once people make a decision – a decision to reallocate their portfolio, for example – it can have an enduring effect.

The role of emotions in decision making

“When it comes to emotions, we have two sides to ourselves,” Ariely said. While we may have good intentions, for example when it comes to healthy eating, those intentions are often compromised in the face of temptation.

Part of the role of advisors is to help clients avoid the injurious effects of temptation.

Most people choose to have a half box of Godiva chocolates immediately, rather than full a box in a week. But given the choice of half a box of chocolates in year, or a full box in a year and a week, most people choose to wait the extra week for a full box.

Ariely calls this bias hyperbolic discounting. When decisions affect events further in the future, people act more rationally. As time frames shorten, temptation plays a greater role and decisions become more irrational.

Hyperbolic discounting explains why people don’t save, diet or exercise – the rewards of immediate temptations are valued too greatly.

To counteract temptation, clients can create binding contracts with themselves to avoid it. Those contracts need to be drawn up before the temptation arises, and must specify exactly how the investor plans to behave in certain circumstances. For example, a contract might specify how the portfolio will be rebalanced if the market goes down by a certain percentage.

“Advisors need to see if they can be this bridge between their clients’ long-term goals and short-term impulses,” Ariely said.

The power of trust and revenge

Ariely described an experiment where player A has the choice of receiving $10 or giving the $10 to player B. If he gives it to player B, the money quadruples and player B has the option to give $20 back to player A.

The rational choice is for player A to keep the $10. Experiment results, however, show that people are really nicer than theory predicts – player A ends up doing better by giving money to player B, because player B will reciprocate.

If player A is given an additional choice – to spend a dollar to take two dollars away from player B in cases where player B has betrayed him – most people will do so, despite the fact that the decision is irrational.

Swedish scientists showed that those people contemplating revenge have brain patterns resembling pleasure, which helps explain why revenge is frequently sought-after.

“This seemingly irrational tendency for revenge is actually inherently useful,” Ariely said, because people understand that if they betray trust, others will go to extremes to seek revenge.

Trust is difficult to restore, Ariely said, and this is challenge faced by regulators and the investment industry in the wake of the financial crisis.

Some final thoughts

Ariely concluded with these five points of advice:

- The advisor’s role is to guide decisions, and to understand what your clients can and cannot compute. Be wary of the curse of knowledge: When you know something well, there is a tendency to assume others know subjects as well as you do.

- Your job is to aid clients and be an expert.

- Think carefully about choice architecture, defaults, and decoys.

- Emotions are a powerful force in short-term thinking.

- Clients are irrational, and an advisor’s job is to protect them from that irrationality.

“You are not just an impartial observer who allows people to express their preferences,” Ariely said. “You have a huge influence, through the questions you ask, and a huge moral burden to get clients to think about choices in the right terms.”

Ariely went back and talked with the nurses who treated him to ask why they insisted on pulling off his bandages quickly. They said his analysis failed to take into account the emotional pain that they experience during the process, but they quickly agreed that was not the goal of the treatment.

The nurses explained that their reluctance arose from two factors: pulling the bandages off slowly was against their intuition, and it would cost them additional time.

Acting against one’s intuition can be incredibly difficult, and Ariely urged advisors to carefully guard against that bias. Be careful of decisions that are not based on data or evidence, and always ask what kind of tests can be constructed to test your assumptions.

More Schwab IMPACT Conference Topics >