Incentives don’t matter, tradeoffs don’t exist and there are no limits to what the government can give you. Those who believe this dogma are likely to still have faith in the tooth fairy. In Seven Bad Ideas, a critique of the neoclassical revival in economics that surrounded Milton Friedman and that affected policy and politics worldwide for more than a generation, Jeff Madrick emerges as tooth-fairy economics’ chief exponent.

Briefly, Seven Bad Ideas argues that the influence of a group of free-market economists led by Friedman over a period from the late 1960s until the 2007-2009 global financial crisis caused a worldwide turn to the political right that destroyed rewards for labor, enhanced the position of elites, hindered growth and generated a series of destructive financial-market booms and crashes.

It’s hard to overstate just how bad Seven Bad Ideas is. Most leftist rants – and that’s what this book is – express a critique of society with which almost anyone can sympathize. This one does not. It is an unsupported claim that the great defining ideas of mainstream economics – the salutary effects of open competition, the efficiency of capital markets and so forth – are flat-out wrong.

They are not wrong. They are generalizations and points of departure, not intended to reflect reality exactly. For example, tests of market efficiency often reveal that prices do not fully reflect all available information and that one can trade profitably on the inefficiencies. Such tests and trading strategies would not be possible without a null hypothesis of market efficiency. The same principle holds for political arguments in which governments are asked to remedy market imperfections: first one must ask what the market would be achieving if it worked perfectly. Only then can one weigh the costs against the benefits of a non-market (government) remedy and come up with a decision.

If you told a group of economists in the 1930s that the worst economic event in the subsequent 80 years would be a long, shallow depression during which U.S. per capita GDP did not fall below $46,795, they would have done a happy dance like no other. (Per capita GDP in the pre-Depression peak year, 1929, was $11,324.1 Both numbers are in 2009 dollars.) Those economists would have regarded capitalism, specifically the mixed and regulated capitalism that produced that astonishing rate of growth, as a stunning and unexpected success.

Yet, according to Madrick, the poor performance of 2008-2014 is proof that capitalism has failed. That is like saying that the internal-combustion engine has failed because motorists sometimes crash their cars. Even if per capita GDP never grows again, which is absurd, the mostly free-market system under which we live has achieved a level of consumption 17 times higher than that of the world’s richest country in 1820.2

There is a glimmer of wisdom in Madrick’s questioning of several ideas that are close to the heart of financial professionals. As Madrick argues, the stock and bond markets are not perfectly efficient. Speculative bubbles exist and often end in crashes. Economics is not a science, but a social science. If there is value in Seven Bad Ideas, it is in the sections that raise these questions.

But first, Milton Friedman was a good-hearted man with good ideas…

…not an ogre who sought to destroy the world. (I knew him slightly.) The ability of political debaters to ascribe malign motives to people with whom they disagree never ceases to astound me. In a democracy, most people in positions of power, including those few economists who do have power, do what they do because they believe it is right. Reasonable people differ on what is right. Polemicists should not sling mud, accusing opponents of only trying to please their cronies and enrich themselves and other members of their social class. Madrick plays this kind of foul ball with some regularity.

Madrick’s seven bad ideas

My review is organized along the same lines as Madrick’s book: each bad idea gets a chapter, the title of which identifies the idea that Madrick doesn’t like. They are (in my own words):

The invisible hand

Say’s law (“supply creates its own demand”)

The desirability of a limited social role for government

The desirability of low inflation

The impossibility or nonexistence of speculative bubbles

The desirability of globalization

The idea that economics is a science

Let’s consider each of these (except #3, because my blood pressure is high enough already).

The invisible hand

Madrick admits to having been seduced, early in life, by Adam Smith’s comment that markets, particularly the interaction of supply, demand and prices, cause resources to be deployed properly and efficiently as if “led by an invisible hand.” Madrick calls this a “beautiful idea,” but warns – rather elegantly – that it is a “source of clean economics in a dirty world.”

But theories are supposed to be generalizations! Newton’s laws are a source of clean physics in a dirty world: they predict that a feather and a brick will fall at the same rate when they do not, because they ignore air resistance. People instinctively know this and do not expect physics to make perfect predictions. The imperfections are what’s interesting and worth studying, and one must always make adjustments for them.

So it is in economics. Bankers “sell…complex securities without informing [the] buyers [of the complexities]” (p. 42). This should be against the law, but -- to some people -- Treasury bonds are complex, so one can debate just how the law should be written. Madrick emphasizes that people are not rational and buy stocks after they have gone up, and they follow fashion in other pernicious ways, even “buying an Hermès Birkin bag” (p. 44) from time to time. This is a familiar complaint about markets, dating back to Thorstein Veblen [1899] and beyond.

We can all agree that markets have imperfections. And we have to have a government that regulates markets in some aspects. But only a writer blinded by anti-market ideology would argue, as Madrick does, that the mere existence of imperfections invalidates the market system, while treating government as an almost unalloyed good.

Say’s Law (supply creates its own demand)

Madrick’s actual chapter title is “Say’s Law and austerity economics,” which is revealing. Austerity economics doesn’t exist. Ignoring second-order effects, governments don’t create or destroy resources, they just redistribute them (after the market has distributed them once, hence the “re” prefix). Austerity, once a meaningful word (an austerity program in World War II might have involved not eating butter so the soldiers could have more), is now code talk for “giving less of other people’s money to politically favored groups.” Stimulus – which may or may not stimulate anything – means “giving more of other people’s money to politically favored groups.” Just making sure we understand each other, Mr. Madrick.3

But I digress. What is Say’s Law, and what does it have to do with austerity?

Say’s Law, named after the 19th century French economist Jean-Baptiste Say (pronounced “sigh”), is usually expressed as “supply creates its own demand,” but that statement is unclear. In plain English, Say’s Law states that if one adds up all the payments received by those whose work, raw materials, and so forth were used to produce a good, that sum is sufficient to buy the good. In other words, there is enough money around that someone can afford to buy the goods.

There is, of course, no guarantee that every single widget produced will find a buyer. There are market imperfections and waste. At the aggregate level, however, Say’s Law implies that there cannot be a general glut of goods or labor -- that is, a general economic depression -- because the prices of goods and other resources (such as labor) will fall until they’re all being used.

Furthermore, Say’s Law suggests that if recessions and depressions do occur, they are self-correcting. Thus, policymakers should avoid interfering with market processes, such as wage and price deflation and asset liquidation, which help to end the depression. By “austerity economics,” then, Madrick and others mean allowing these processes to happen naturally without government intervention. What is proposed as an alternative is “Keynesian” deficit spending by the government, believed by Keynes and his many followers to move the economy from a condition of depression back to “full employment” (of all resources, not just labor).

Keynes himself advocated deficit spending only as a temporary measure, to be used in depressions. He assumed or hoped that governments would run surpluses in more normal times, building a kind of savings account to be used in the next depression. (“Keynesians,” in contrast, often want to run deficits all the time.) Thus, while drawing a distinction between the natures of family budgets and government budgets, Keynes acknowledged an essential similarity between them: each must balance in the long run. He just wanted the government to spend countercyclically, to ramp up spending when families were ramping it down. Yet what is often remembered about Keynes is that he said governments are not [exactly] like families.

“But…governments are not at all like families,” echoes Madrick. He then stumbles badly: “In hard times, a family saves to improve its future prospects; its savings do not affect the prospects of others” (pp. 54-55).

Really? If I decide to do my own plumbing repairs, cook my own meals and vacation in my backyard, does it not affect the prospects of the plumber, restaurateur, and resort hotel owner? Does the lowering of those tradesmen’s incomes not have additional, follow-on effects? In elaborating on a familiar and correct idea (the fallacy of aggregation), Madrick makes a very basic mistake, one that he could have avoided by looking at the circular-flow diagram in the first chapter of his undergraduate economics textbook.

And mistakes like this one pervade the book – one does not have to look hard for them; they are not isolated examples of carelessness. They reflect a profound lack of understanding of economics, and of the economy, by the author.

The desirability of low inflation

Madrick rails against economists who – like Milton Friedman -- advocate for low inflation. Madrick’s desire for more inflation reflects two misunderstandings: (1) a naïve faith in the Phillips curve, which asserts an inverse connection between inflation and unemployment but only works in the short run, and (2) the post hoc ergo propter hoc association of postwar inflation with strong growth in developed countries.

Madrick seems to believe inflation is good because he assumes that the Phillips curve is stable over time. If one can move along the curve but the curve does not itself move, then unemployment could be reduced if central bankers would simply allow inflation rates to move upward.

But this is tooth-fairy economics at its silliest. The Phillips curve “works” only in the short run: inflation and unemployment move opposite each other (we move along the curve) as we glide in and out of recessions. But, over longer periods of time, the curve itself moves; that is, the orderly relationship associating higher inflation with lower unemployment breaks down.

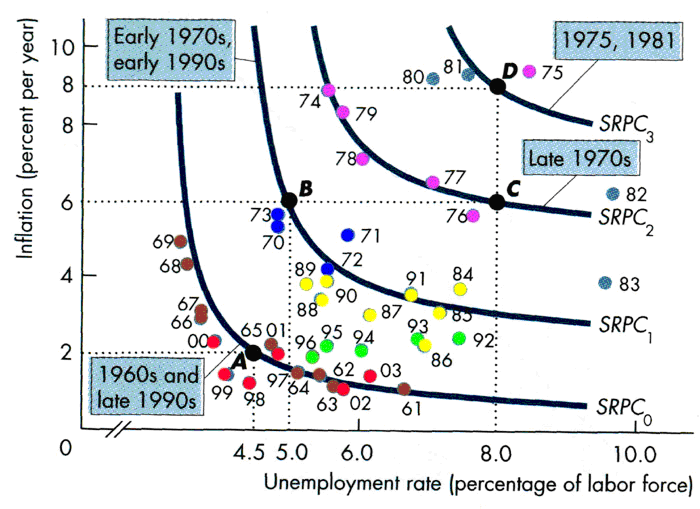

As Figure 1 shows, the Phillips curve moved outward for decades, with ever-higher inflation rates associated with each given level of unemployment. Then, after about 1981, it started to move inward. The inflation-unemployment relationship is not stable, and – surprise! – you can’t cure unemployment by debasing the currency, or we would have done so a long time ago.4

Figure 1

Movement of Phillips Curve over Time, 1961-2003

Source: Gabriel Aidar, Brazilian Development Bank. Accessed at http://grupolujan-circus.blogspot.com/2012/05/phillips-curve-during-dark-age-of.html on November 22, 2014.

Note: The number on the y-axis between 8 and 10 should be 9, not 8. The error is in the original.

Madrick also strongly suggests (pp. 120-121) that growth was faster when inflation was allowed to accelerate, particularly in the 1960s and 1970s, and would be again if we pursued a dovish inflation policy.5 Inflationism ruled during the second half of the trente glorieuses (the 30 glorious years after World War II) and destroyed the real value of just about all the fixed-income investments in the world, but tooth-fairy economists don’t care about bondholders. If we treat bondholders and other savers as expendable, can we find a justification for high inflation in some kind of connection to long-term real growth?

No justification exists in the data. The U.S. had rapid growth with deflation in the late 1800s and then again in the 1920s. Inflation was very low (although positive) through the best years of the trente glorieuses, from about 1953 to 1966, and then again during the late 1990s boom time. The exceptional growth during the postwar period was not due to inflation, but to a low starting point (the Great Depression), the dynamism of a country – the U.S. – with a young, booming population and cheap resources, and lots and lots of capitalism. Keynes may have ruled the academy, but the Fortune 500 ruled the world. There has rarely, if ever, been a time when large corporations had as much power as they did then.6

Speculative bubbles: Are financial markets efficient? Can we make them more efficient?

When Madrick expresses doubts about the efficient market hypothesis and other basics of classical finance, he is not alone. Just about every investor questions whether the market is really as efficient as the Nobel prize-winning University of Chicago professor Eugene Fama says it is, and as many other finance professors used to believe it was, but now tend not to. Additional Nobel Prize winners, notably the Yale professor Robert Shiller, have provided evidence of market inefficiencies and the existence of speculative bubbles.7

Nevertheless, Madrick’s tone in discussing the state of modern finance is combative and not particularly helpful. He starts by describing the efficient market hypothesis or EMH, which he renames the efficient market theory (EMT) even though it is not a theory, as “a destructive set of ideas” (p. 138). Far from being destructive, EMH is the foundational idea of modern finance and has saved investors hundreds of billions of dollars in fees. EMH is also not exactly correct.

Hypotheses, of course, are not supposed to be exactly correct. They serve as a base case and point of departure for empirical tests that, in all but a few cases, find the hypotheses wanting. It turns out the market is not perfectly efficient (some would say not even close); some active managers beat their benchmarks and are worth their high fees; and speculative bubbles do exist.

But those findings, celebrated by Madrick in his positive description of behavioral finance, do not make the EMH destructive; the EMH is the null hypothesis for all investigations into market inefficiency and for all measurement of alpha or manager value-added. Without the EMH, and the related ideas of modern portfolio theory (MPT) and the Capital Asset Pricing Model (CAPM) that Madrick denigrates, investment finance would still be where it was in the 1940s: managers would buy some stocks and hope they go up.

Speculative bubbles do real harm, especially to those who buy when the bubble is inflating, and/or sell after the bubble bursts, missing the recovery. Bubbles also cause wider damage by misallocating capital. However, we do not know how to regulate them away. We expect market participants to obey the law, and if a bubble is caused by an epidemic of misrepresentation, as some think the Great Real Estate Bubble and subsequent crash were, sensible legislation and regulation can prevent those events from recurring. But no plausible government action can prevent people from more generally pushing asset prices above their fundamental value when irrational exuberance takes over. Madrick may yearn for regulation that accomplishes this, but none is possible.

Efforts to regulate markets so that there is substantially less volatility are about as likely to succeed as efforts to curb lust, greed, gluttony, pride and sloth. You’ll make a little dent but that is all. Part of human nature is the urge to overpay for whatever assets are in fashion and to sell, in a panic, whatever assets have disappointed. Momentum is likely to continue to be a factor in setting asset prices no matter what preventative actions we take.

As part of his larger critique of economists and financial markets, Madrick tries to draw a direct line of causation between EMH and the global financial crisis and its aftermath. His argument implicates EMH with the deregulation (or non-regulation) of financial markets, the repeal of Glass-Steagall, the abuse of derivatives during the housing bubble and the bankruptcies of Wall Street firms in the fall of 2008.

This logic contains a look-back bias: if the event you’re trying to explain is big enough, and the global financial crisis certainly qualifies, you can trace it back to almost any causative factor. It’s an accusation that can’t be refuted – how can you prove that the EMH didn’t cause the crash?

It’s more likely that the crash was caused by human nature – greed and fear – helped along greatly a government mandate to extend mortgages to unqualified buyers and by the misalignment of incentives between bank employees and shareholders. The next crash will be caused by something else and will be just as difficult to forecast and to avoid as the last one.

Economic ideas, including obscure theories, really do have real-world consequences.

However, it is a stretch to blame the EMH -- largely the brainchild of one young man, Eugene Fama, working at the University of Chicago in the early 1960s, for the many economic troubles that the world has faced between 2007 and the present.

Globalization

When Madrick discusses globalization, his tone is more sober than in much of the rest of the book. He helpfully sums up globalization, a word that too often goes undefined, as “the expansion of the world into one economy” (p. 174). He argues cogently that, with so many different cultures, standards of living, endowments of natural resources, and forms of government, globalization must necessarily be difficult to put into practice.

And, in fact, there have been many missteps: currency crises in Asia, a depression in Japan, an uncomfortable mix of prosperity and repression in China and Russia. Even the recent stirrings of growth in Africa can be read negatively; soaring commodity prices were the catalyst, and sustainable industrial development has been painfully slow.

Madrick isn’t against globalization per se; he just doesn’t think free markets do a good job of it. He notes that there was a great deal of successful globalization in the 19th century, “a time of substantial tariffs, fixed currencies, and robust government interventions” (p. 171). Point taken. But it was not the kind of government activism that today’s leftists envision; there was no welfare state, little protection of incomes, light regulation of business. (There were government-sponsored enterprises.) Nineteenth-century government action may well have been supportive of global growth, and we might look to that period for clues on how to do the job better.

I understand the case against radical, immediate globalization. While developed countries benefit from trade by having access to cheap consumer goods, there is a real cost to American and other rich-country workers having to compete with workers in countries where wages are much lower. Wage differentials are gradually narrowing, and the U.S. will someday become competitive again, but workers can only adjust so fast and do not live forever, so their needs in the present must be taken into consideration.

Yet, as the British Prime Minister, Benjamin Disraeli, almost said, other countries will not allow the U.S. to be the workshop of the world forever.8 (What he actually said, in 1838, was that “the Continent will not suffer England to be the workshop of the world.”) People desire naturally to compete, and high wages right across the river or ocean are an easy target. Globalization will occur, the main question is how quickly.

According to the economic historian Deirdre McCloskey [2010], the “Great Fact,” the economic fact that makes all others seem unimportant, is the immense rise in standards of living since 1800. But the Great Fact of our own time is the newly global nature of this improvement. Hans Rosling, a statistician and popular TED lecturer, is fond of pointing out that “peak inequality,” when measured globally, occurred back in 1948. At that time, China, India, and Africa had not seen much improvement in living standards in 500 years, while the developed world was already rich and rapidly getting richer. The great convergence or catch-up of less developed countries did not begin in earnest until the 1980s and ran at its fastest pace after 2000.

It is the first really lucky break that the world’s poor have had in all of human history. I pray that it does not stop.

Is economics a science?

On this question of very long standing, Madrick is right to say that it is not. Economics is nothing like an exact science, as physics is; it’s a social science, a field originating in the humanities but informed with numbers. I hope I don’t insult too many economists by saying that economics might be better understood if it were taught as a branch of animal behavior.9

But, rather than asking how we should best understand economic analysis – as a science or as some other form of knowledge – Madrick plays “gotcha,” finding it scandalous that – get this! – economists sometimes make mistakes. Some researchers, led by a young graduate student, famously discovered a data error in Carmen Reinhart and Kenneth Rogoff’s This Time is Different, a book that traces the history of sovereign-debt-fueled crises over the last several centuries.10 Madrick ridicules President Clinton’s chief of staff, Erskine Bowles, for saying that the discovery of this error does not overturn Reinhart and Rogoff’s basic conclusion that too much government debt is bad.

Apparently, debt – any amount of it – is good until you can prove, without making a data error, what specific amount is bad. What would Madrick need to be convinced that there is such a thing as too much debt? Interest on government debt exceeding all taxes collected? Interest on government debt exceeding GDP itself? There are no limits when the tooth fairy is on your side.

Conclusion

Madrick started feeling sorry for us poor schlubs long ago. He wrote The End of Affluence in 1995, when incomes had risen 50% in the prior 20 years and would rise another 30% in the next 12. This growth rate doesn’t hold a candle to China’s or to our own history, but maybe it’s harder to grow high incomes than low incomes. (Isn’t it an achievement to maintain a steady state wherein we consume in a week what most people throughout human history consumed in a year?) Or maybe aging populations have slow economic growth.

We also may have made some policy mistakes, including failure to regulate more wisely. I wish we had required federally insured financial institutions to have CFOs who know the difference between AAA-rated mortgage securities and “toxic waste.” (Wishful thinking, I know.)

But, in general, we’ve chosen the path of more government, just as Madrick wanted all along. While he alleges that the world has followed Friedman’s siren song, government spending at all levels is 35-38% of GDP in the U.S.,11 and higher in almost all other countries, and is testimony to the fact that it has not. And the 174,545 pages of federal regulations show that the deregulation fever of which Madrick writes doesn’t actually exist.12

Yet we had a financial crash, one that would almost surely been milder – or, conceivably, avoided altogether – if the balance sheets of systemically important financial institutions had been more prudently regulated. Does this mean that we should seek to regulate financial markets in ways designed to prevent bubbles and crashes in the future?

I would argue that it’s close to a lost cause. Human beings will try to reach for the sky in good times and to plumb the depths of despair in bad ones. These tendencies can be moderated – a little – through what modern economists call “macroprudential regulation” but are not going to go away.13 In an exchange of poison-pen letters with Paul Krugman over the question of what, if anything, economists should have done to predict the recent crash or help us avoid it, John Cochrane [2011], a financial economist at the University of Chicago (and Eugene Fama’s son-in-law), wrote:

The case for free markets never was that markets are perfect. [It] is that government control of markets, especially asset markets, has always been much worse.

In effect, [interventionists are] arguing that the government should massively intervene in financial markets and take charge of the allocation of capital...To reach this conclusion, you need evidence, experience, or some realistic hope that the alternative will be better. …[T]he...SEC...could not...find Bernie Madoff when he was handed to them on a silver platter. Fannie Mae, Freddie Mac, and Congress all did a dreadful job of managing the mortgage market. Is this system going to...guide financial markets to the right price, replace the stock market, and tell our society which new products are worth investment? Government regulators failed just as abysmally as private investors and economists to see the storm coming.

[Moreover,] the behavioral view gives us a new and stronger argument against regulation and control. Regulators are just as human and irrational as market participants. If bankers are...‘idiots’, then so must be the typical Treasury secretary, Fed chairman, and regulatory staff. Most of them are ex-bankers! Furthermore, regulators act alone or in committees, without the discipline of competition, where behavioral biases are much better documented than in market settings. [Regulators] are still easily captured by industries, and face politically distorted incentives. Careful behavioralists know this, and do not quickly run from ‘the market got it wrong’ to ‘the government can put it all right’...They do not even think of jumping from ‘irrational’ markets, which they believe in deeply, to government control of stock and house prices and allocation of capital.

We would do well to heed these words, and to have modest expectations about what economists can do.

Laurence B. Siegel is the Gary P. Brinson director of research at the CFA Institute Research Foundation in Charlottesville, VA. He lives in Wilmette, IL and can be reached at [email protected].

References

Adler, David E. The New Finance of Liquidity and Financial Frictions. CFA Institute Research Foundation, Charlottesville, VA.

Asness. Clifford, and John Liew. 2014. “The Great Divide over Market Efficiency.” Institutional Investor (March 3). Accessed at http://www.institutionalinvestor.com/Article/3315202/Asset-Management-Equities/The-Great-Divide-over-Market-Efficiency.html#.VHEwjkvKPwI on November 24, 2014.

Chambers, David, Elroy Dimson, and Justin Foo, “Keynes, King’s, and Endowment Asset Management,” forthcoming in Brown, Jeffrey and Caroline Hoxby, eds., How the Great Recession Affected Higher Education, University of Chicago Press, Chicago. Accessed at http://www.nber.org/chapters/c12860.pdf on November 24, 2014.

Cochrane, John H. 2011. “How Did Paul Krugman Get It So Wrong?” Economic Affairs (June), pp. 36-40. Accessed at http://faculty.chicagobooth.edu/john.cochrane/research/papers/ecaf_2077.pdf on November 25, 2014.

Crews, Wayne and Ryan Young. 2013. “Twenty Years Of Non-Stop Regulation,” The American Spectator (June 5), http://spectator.org/articles/55475/twenty-years-non-stop-regulation.

Hausman, Daniel M., editor. 2007. The Philosophy of Economics: An Anthology, Cambridge University Press, Cambridge, England, 2007, http://digamo.free.fr/hausman82.pdf.

Herndon, Thomas, Michael Ash, and Robert Pollin. 2013. “Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff.” University of Massachusetts Amherst working paper, accessed at http://www.peri.umass.edu/fileadmin/pdf/working_papers/working_papers_301-350/WP322.pdf on November 24, 2014.

McCloskey, Deirdre N. 2010. Bourgeois Dignity: Why Economics Can't Explain the Modern World, University of Chicago Press, Chicago.

Schuyler, Michael. 2014. “A Short History of Government Taxing and Spending in the United States,” Tax Foundation Fiscal Fact #415 (February 19). Accessed at http://taxfoundation.org/sites/taxfoundation.org/files/docs/FF415.pdf on November 27, 2014.

Veblen, Thorstein. 1899. The Theory of the Leisure Class: An Economic Study of Institutions. Macmillan, New York.

Read more articles by Laurence B. Siegel