If you thought a stretch of subpar performance would shake a fund manager’s confidence, you’d be wrong in the case of Robert Arnott.

Through Research Affiliates, his Newport Beach firm most famous for its fundamental indexing strategies, Arnott manages PIMCO’s All Asset funds. These include PIMCO All Asset (PAAIX) and PIMCO All Asset All Authority (PAUIX).

Despite the funds’ recent struggles, Arnott displayed an assured mien during a wide-ranging interview on a warm, late March afternoon at PIMCO’s offices. Asset classes poised to beat inflation (especially commodities and emerging markets stocks and bonds) have gotten cheaper lately, he claimed, as deflationary fears have increased, and this has Arnott reasonably upbeat about his All Asset funds’ prospects.

Buy what’s cheap, sell what’s dear, beat inflation

Inflation protection is a key driver behind the strategy of the All Asset funds. The other driver is looking for cheap asset classes. The All Asset funds are funds of funds, where Arnott uses his PIMCO fundamental index funds and a slew of other PIMCO stock and bond funds to get his asset class exposure. The portfolios may look complicated, but the strategy behind them is simple: buy what’s cheap, sell what’s dear and beat inflation in the process.

And if Arnott himself has a relaxed demeanor, the funds have ambitious return goals. All Asset is designed to return inflation plus five percentage points on an annualized basis. All Asset All Authority, which uses leverage and some of PIMCO’s funds that short asset classes, is designed to produce inflation plus 6.5 percentage points.

Beating inflation, but lagging the stated goal

The funds have beaten inflation, which has run at 2.01% per year, but fallen short of their stated goals over the past decade. For the 10-year period through the end of March 2014, All Asset has produced a 5.67% annualized return, while All Asset All Authority has produced a 5.32% annualized return.

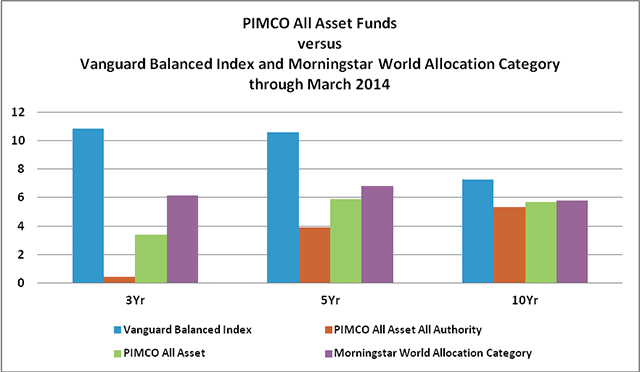

Despite inflation-beating returns, the funds have also struggled when benchmarked against a balanced portfolio of domestic stocks and bonds over 3-, 5-, and 10-year periods, represented by the Vanguard Balanced Index Fund (VBINX) in Exhibit 1.

Exhibit 1

That’s because what’s been expensive and poised to barely match inflation (U.S. stocks and bonds primarily) has gotten even more expensive. Also, what’s been cheap and poised to overcome inflation (especially emerging markets stocks and bonds) has gotten cheaper. Arnott has mostly avoided the former and owned the latter.

The funds are heavily exposed to emerging markets stocks and bonds, which have not done well, and Arnott has bet on the local currencies at a time when the dollar has surged. Accordingly, the funds match up much better against the Morningstar World Allocation Category average over the 10-year period.

Moreover, in the All Asset All Authority Fund, he has been short the S&P 500 through the PIMCO Stocks Plus Short Fund (PSTIX) both because of domestic stocks’ expensive valuations and as a way to manufacture extra capacity for more emerging markets stocks exposure. Shorting domestic stocks theoretically allows for more emerging markets stocks exposure without incurring more equity-based volatility.

All these bets have caused the funds to struggle.

In dollar terms, the MSCI EM Index is up 0.12% annualized for the 3-year period through March 30, 2014. In local currency, it’s up 6.27% annualized. The lower return, when translated back to the dollar, reflects the dollar’s strengthening. Accordingly, the PIMCO Emerging Markets Currency Fund, to which All Asset All Authority currently has 10% of its asset allocated, has declined 2.95% annualized over the same 3-year period.

Finally, over the same period, the S&P 500 Index is up a breathtaking 16.45% annualized.

Bets on emerging markets stocks and currencies and shorting the S&P 500 (the latter at least in All Asset All Authority) over the past few years have been painful.

First- and second-pillar assets are expensive

Indeed, the more recent the frame of comparison in Exhibit 1, the more unflattering it is to the All Asset funds. But this is precisely why Arnott is confident. What he calls “first pillar” assets, or developed markets stocks and bonds, have rallied hard, setting them up for very low future returns. Emerging markets stocks, by contrast, have stagnated for a few years now, setting them up for better future returns.

Domestic securities have raced so far in recent years that a classic balanced portfolio like the Vanguard fund is poised to deliver less than 1%, real over the next decade by Arnott’s lights. The BarCap Aggregate U.S. Index (AGG) may deliver 0.50%, real, for the next decade, while the S&P 500 may only deliver 1%, real, he claims.

Bond returns will basically equal their starting yields. Stock returns will depend on starting valuations and dividends. Unfortunately, starting valuations are high and dividend yields are low. The S&P 500 is trading at a Shiller P/E (current price divided by past 10-years’ inflation-adjusted average earnings) of 27 and delivering a dividend yield of less than 2%. The average Shiller P/E over the past century or so is around 16, and the market’s future 10-year returns have been decidedly subpar from this valuation starting point.

Developed markets international stocks are slightly cheaper, but they also don’t get Arnott too excited. European bonds, some with negative yields, are positively awful, according to Arnott.

Incidentally, Arnott’s analysis has significant implications for advisors plugging in the customary 7% nominal return (4%-5% real return) for a standard balanced portfolio in their clients’ savings and planning models. Barring continued multiple expansion for stocks, which doesn’t seem justified, current domestic bond yields and stock valuations make that very long-term historical 7% look virtually impossible to Arnott.

Third-pillar assets are cheap

If standard developed markets stocks and bonds won’t get investors to their retirement goals, something else – a “third pillar” – is required. Third-pillar assets provide yield and uncorrelated return to mainstream stocks and bonds. They also provide a measure of inflation protection when they’re reasonably priced. They consist of emerging-market stocks and bonds, commodities, REITs, TIPS and high-yield bonds.

Third-pillar assets aren’t always guarantees to beat inflation, though Arnott says they have at least an inherent bias to counter a rising U.S. yield curve. Like any other asset class, third-pillar assets can get too expensive to counter inflation and to be worth owning, and Arnott is sensitive to their valuations rather than buying them indiscriminately.

Indeed Arnott had less confidence many months ago that even third-pillar assets were priced to meet the funds’ lofty goals. And he still doesn’t think some of them, such as REITs, are priced to do so.

However he said that a time would come when at least some of those assets would be more attractively priced, and that time would arrive when investors stopped worrying about inflation. In two of his three monthly letters (and also in conversation with me) he has argued that the time for most third-pillar assets to deliver strong long-term returns is now. (Those letters are here, here, and here.)

Arnott believes emerging-market stocks and bonds, emerging-market currencies, domestic high-yield bonds and commodities are cheap enough to deliver 4.5% real returns into the future He indicated to me that the Shiller P/E of many emerging stock markets is less than half that of the S&P 500. Moreover, his 4.5% forecast is for simply buying and holding cap-weighted indices. He said his fundamental index products and PIMCO’s fixed-income expertise can both add at least a bit more.

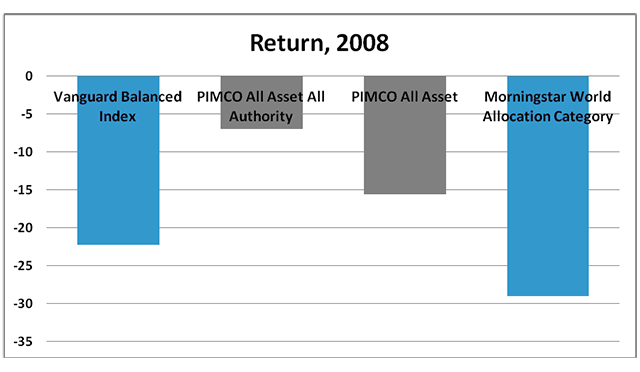

Arnott will buy first- and second-pillar assets if their valuations argue for places in the portfolios. For example, he increased the funds’ exposures to domestic long-maturity and core bonds immediately before and during the financial crisis. This move, in part, allowed All Asset and All Asset All Authority to drop 15.48% and 6.93% respectively in 2008, when the Vanguard Balanced Index Fund swooned 22.21% and the Morningstar World Allocation Category average was down 28.98%.

Exhibit 2

The absence of then-expensive third pillar holdings such as emerging markets equities and REITs was also helpful to the funds during the crisis.

Conclusion

Arnott concedes that his own studies of demographic trends indicate a low probability of severe inflation. Nevertheless, investors will have to contend with it at some point after so much “money printing.” As Warren Buffett noted in his 2014 Berkshire Hathaway shareholder letter, investors have had their purchasing power eroded over the past half-century, and that this likely to happen over the next half-century.

Even with a dramatic drop in the price of oil and stagnating median household income, there’s still some inflation, Arnott argues, thanks mostly to surging rents and healthcare costs. He said there will eventually be more inflation, and he is happy to pick up the assets that provide the most protection against it precisely when everyone’s attention on deflation has made them available at cheap prices.

Arnott makes a compelling case for the poor prospects of mainstream stocks and bonds for the next decade based on starting valuations and yields. He believes in the predictive value of starting yields for bonds and of the Shiller P/E for stocks. These methodologies can’t predict returns for 3-year periods; expensive stocks can get more expensive, for example. But Arnott remains confident in the longer term validity of his valuation methods. There is only one period in history when a starting Shiller P/E of 27 (the current multiple) produced something close to a normal market return for the next decade.

It isn’t easy for investors to arrange their portfolios around valuation metrics that only exhibit their merit over longer periods of time, but Arnott doesn’t know of a better way of approaching investing. Investors would do well to heed his warnings, and to put part of their portfolios in Third-pillar assets with higher return prospects. Inflation protection can be had relatively cheaply now; that won’t always be the case. Arnott’s funds are convenient, thoughtfully-arranged ways to access it.

John Coumarianos is a freelance writer. He has worked as a branch representative at Fidelity Investments, a mutual fund and equity analyst at Morningstar and a writer at Capital Group. He also runs the website/blog Institutional Imperative.

Read more articles by John Coumarianos