Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

of Advisor Perspectives.

“We wanted flying cars, instead we got 140 characters.” – Peter Thiel

Think about recent innovations that have changed the way you live:

-

With a click or two on your smart phone, a sedan appears to take you to your destination.

-

Yesterday, you could film a video of your daughter riding a horse and instantly share it with 500 of your

closest friends. Today, you can stream the same video live to anyone with a smart phone.

-

A wristband can track your exercise activity, weight and even sleep cycles.

-

Credit card and mortgage payments can be made while lounging by the pool.

-

Finding a boyfriend or girlfriend is possible without cheesy pickup lines.

-

And of course, most importantly, you can shop anytime, at any major store, from anywhere.

These and many other new innovations save us a lot of time and effort but, believe it or not, they do little to

generate sustainable economic growth. Sustainable economic growth depends on productivity. Despite these new

innovations, domestic productivity is flat lining.

In 2014, the annual growth rate of economic productivity in the U.S. was merely 0.10%. Sadly, our negligible

productivity growth (or total factor productivity, TFP) compares favorably to Europe (-0.44%), China (-0.10%), Japan

(-1.20%), the United Kingdom (-.10%) and most other developed economies. Not surprisingly, global productivity,

weighted GDP, declined in 2014.

Despite all of the wonderful innovations that make our lives easier, productivity growth has trended lower since the

1970s, except for a few years around the tech boom of the late 1990s. Economic growth (GDP) in America and much of

the rest of the world since the 1970s has trended lower as well. A previous article, “The

Humility of Rates and the Arrogance of Equities,” illustrated that secular GDP currently resides at

the troughs of prior recessions despite the long, slow recovery from the financial crisis of 2008.

With zero productivity growth, GDP simply becomes a measure of labor and capital deployment. Because labor and

capital are limited resources, productivity, or our ability to leverage labor and capital, is the one factor that

can produce sustainable economic growth over the long run. The confluence of sub-trend economic growth and

declining productivity growth is not a coincidence, and it is not getting the attention it deserves. The U.S. and

other leading world economies are consuming the limited resources of capital and labor predominantly for

unproductive uses.

“Corporate Buybacks; Connecting Dots to the

F-word,” suggested that leadership in corporate America is shirking its responsibility to

shareholders. Through the extensive and growing use of share buybacks, today’s corporate executives have opted

for actions producing hollow short-term stock price gains and the generous compensation that accompanies such

actions. This self-serving use of corporate cash, often borrowed under the guise of expressing confidence in the

company’s future prospects, has been undertaken at the expense of longer-term strategic planning and

expenditures aimed at growth-enhancing innovation.

Share buybacks, however, are merely exemplary of a bigger problem – that of corporations focusing on

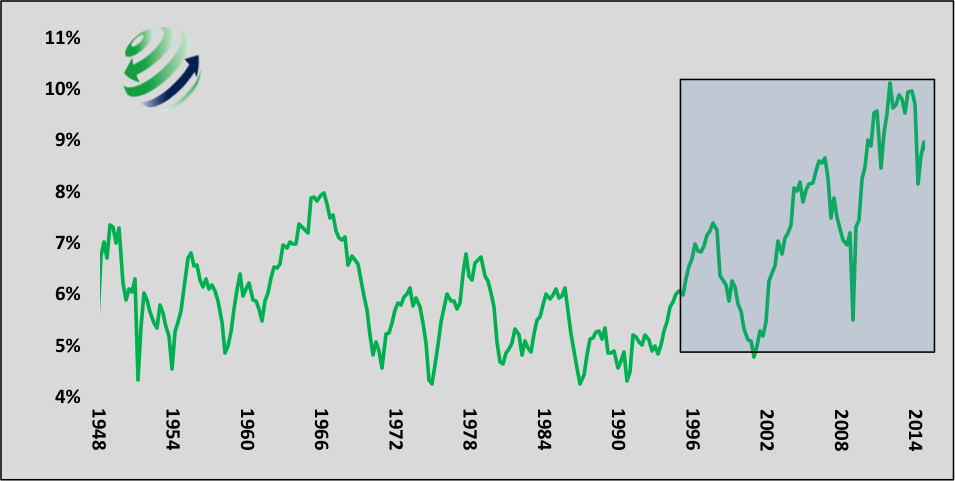

maximizing today’s earnings instead of tomorrow’s growth. Corporate profit margins, as shown below, are

just one of many clues that corporate management has changed its modus operandi. The first graph shows the upward

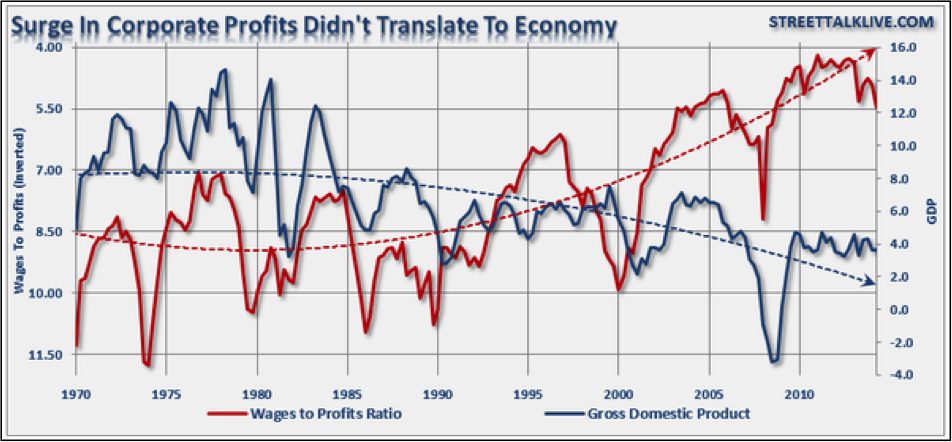

trend in corporate margins since 1990. The second graph shows the relationship of wages to profits and plots GDP.

The declining trend in wages relative to profits explains a good portion of expanding corporate profit margins.

Corporate Profit Margins as a % of GDP

Data Courtesy: St. Louis Federal Reserve (FRED)

Ratio of Wages to Profits Versus GDP

Chart courtesy: Lance Roberts streettalkalive.com

Corporate profit margins, which currently reside near 65-year highs, show that companies are making significant

efforts toward running as efficiently as possible. This is a good thing and should be applauded by shareholders.

However, before clapping, investors must ask if executives are neglecting future growth to run more efficiently

today, and, if so, what is the opportunity cost of this sacrifice?

The best way to assess whether future growth is being neglected is to observe productivity data such as in the graph

below. The 10-year average productivity growth rate (black line) has declined significantly from the levels prior to

1980. Similarly, note the widening gap between the pre-1980 trend (black dotted line) and the more recent trend of

the past 30+ years (red line).

Companies are indeed sacrificing market-creating or empowering innovations to become more efficient, as

supported by slowing national productivity gains. Companies are taking the excess earnings and increased free cash

flow, resulting from efficiency gains, and either returning it to shareholders or plowing it back into more efficiency

innovations and other expense minimization efforts. The intended effect is to rapidly improve financial

ratios, metrics used to gauge a company’s performance, which by no coincidence are also used to justify equity

prices and thus, often, executive compensation.

Total Factor Productivity (TFP) Trends

Data Courtesy: The Conference Board

The italicized terms in the passage above describe distinctions of innovations that were coined by Clayton

Christensen, professor of Business and Administration at the Harvard Business School, best-selling author and

co-founder of Clayton Christensen Institute for Disruptive Innovation. Christensen has long been at the forefront of

the study of innovation and productivity.

Christensen uses the computer as a great example of what he calls “market-creating or empowering innovation.”

Over the past 50+ years, computers progressed from the behemoth ENIAC, which weighed over 30 metric tons, to the

desktop/laptop PC and most recently to pocket-able smart phones. Over this period the number of users increased

sharply as costs decreased significantly. Inventing and producing market-creating innovations, like the computer,

have a long time horizon and typically involve significant dollar and labor investment. The risks of failure are

plentiful. However, despite the longer time frame, costs and many risks, the dividends resulting from such

innovations are long lasting and result in new products, jobs and company and industry creation. Needless to say,

durable economic growth for years to come is another benefit.

Efficiency innovations produce benefits as well, but they are not multiplicative as are market-creating innovations.

Innovations in this group decrease the costs of producing or distributing goods, typically by reducing the man hours

or resources needed to manufacture or sell such goods. Self-checkout registers at supermarkets are a good example.

These registers do not increase sales, however, they decrease expenses as fewer employees are required for the same

amount of goods sold. The benefits of using automated registers are predominately cost savers and do not create

incremental efficiencies. They are one-hit wonders.

Efficiency innovations sustain economic growth by reducing costs and market-creating innovations produce incremental

economic growth through the development of new products or services that subsequently proliferate. When both types

of innovations are equally pursued, an economy has the best chance to reach its optimal growth rate. Efficiency

innovations reduce the need for labor and other resources resulting in higher profit margins and ultimately

additional profits to corporations. The additional cash flow and excess labor capacity can then be employed to

develop market-creating innovations. When market-creating innovations come to fruition, they create new jobs,

businesses and more efficiency innovations. This virtuous and reinforcing innovation cycle is essential to building

sustainable economic growth.

Today this cycle is clearly out of balance as exposed by increased profit margins and stagnating productivity data.

Additional profits resulting from efficiency gains are chasing more efficiency innovations instead of

market-creating innovations like the next computer, Model T, steam engine or telephone. Jobs are being lost due to

the gained efficiencies but new ones are not readily being created. As a result, economic growth is stagnating.

In an interview with Forbes in 2012, Christensen had this say about efficiency innovations: “Our

current economy, however, has gone off of the rails in large part because we are focused almost entirely on

efficiency innovations – on streamlining and wringing bottom line savings and additional profits out of

our existing organizations.”

A year later he followed it up with this from an interview in Inc. magazine: "My sense is over the last 20

years the American economy has generated about one-third the number of empowering innovations as was historically

the case." What's the potential toll of all this lost innovation on the future of the country? Christensen

hypothesized: "If you want to know what the future of America looks like, just look at Japan. You can feel the same

thing happen in the United States, and I worry a lot about that."

As noted above, GDP coupled with zero productivity growth is simply a measure of labor and capital deployment.

Productivity is the leverage that allows us to get more out of capital and labor. In the short run, efficiency

innovations accomplish this. However, in the longer run efficiency innovations can have a stagnating effect on

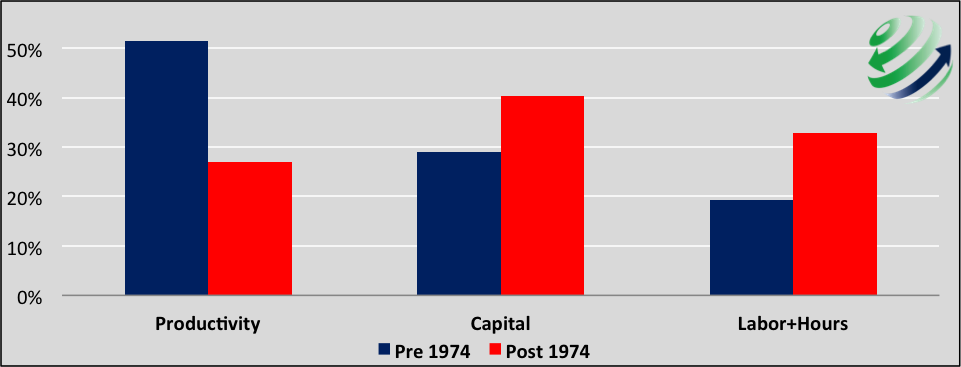

economic growth absent the development of market-creating innovation. The chart below shows how the contribution of

the three factors of economic growth (productivity, capital and labor) have changed over time in the U.S. This

highlights my concern that we are not using our finite capital and labor resources as productively as we should.

How much longer can we rely on the benefits of the baby-boom demographic and debt growth to account for a large and

growing portion of economic growth?

Contributions to Economic Growth

Data Courtesy: The Conference Board

As the data and Christensen make clear, we are reaching the limits of economic growth – barring new

market-creating innovations. Recent U.S. demographic changes, characterized by aging baby boomers reaching

retirement age and tougher immigration policies, are stunting work force growth. The current U.S. employment

participation rate is at a 38-year low (equaling the 62.6% in October 1977). The demographic tailwind is quickly

becoming a headwind as the burden of supporting a growing elderly population will become heavier. Facing this

headwind, we also must contend with the increasing challenges brought on by record-high debt levels restricting our

capacity to employ more capital. The ratio of total debt to GDP stands at 343%, the highest level in well over 100

years.

As a result, economic growth is becoming increasingly dependent on productivity gains as labor and capital growth

become harder to achieve. Within the last month, the IMF, World Bank and Goldman Sachs downgraded their long-term

economic growth projections for the United States. This was largely in response to dismal productivity data recently

released by the U.S. Conference Board for the years 2013 and 2014.

Implications for investors

As investors we need to clearly understand these trends and the potential implications. Proper valuation of a

company involves the estimation of earnings and cash flows for a long period of time. Most equity analysts form a

baseline of current or near-term earnings expectations and then compound the earnings at a pre-determined and

assumed growth rate(s). These growth expectations are typically tied to corporate, industry and overall economic

projected growth rates. Slight variations in expected growth rates can have an outsized effect. This sensitivity to

assumed growth rates is further magnified today by price-to-earnings ratios and other valuation measures that are at

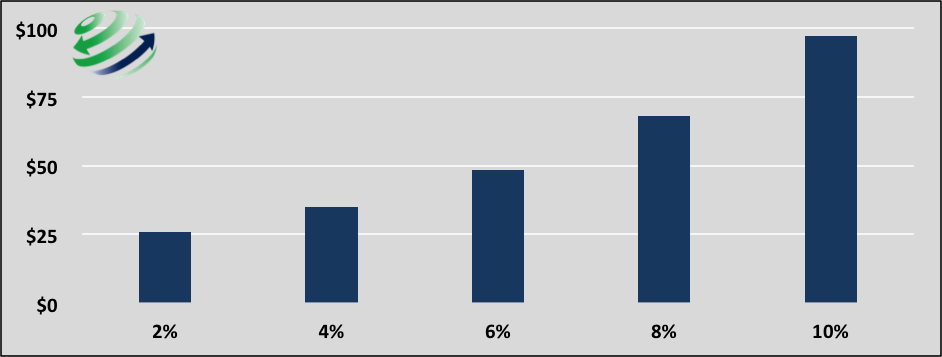

or near all-time highs. The chart below shows how a small 2% change in future earnings growth results in a 25-30%

reduction in the present value of that expected earnings stream. Needless to say the combination of a normalization

of valuations with a decrease in expected future earnings would be devastating for stock prices.

Present Value Sensitivity to Different Growth Rate Assumptions

Based on $1 of present earnings compounded using various growth rates as shown for 30 years

Public policy implications

America is an innovative society but we are putting too much emphasis on efficiency innovations and not enough on

market changing innovations. This imbalance is costing us dearly. The mindsets of investors, corporate America and

society as a whole needs to change. Focus needs to be redirected from the present to the future. For example:

-

Executive compensation structures need to reflect the long-term performance of companies.

-

The U.S. government should enact tax reforms that reward companies investing in market-changing innovations.

-

The Federal Reserve should acknowledge and re-consider the consequences of extreme monetary policy measures.

-

Investors should demand CEOs earn their exorbitant compensation by implementing thoughtful long-term

investment strategies.

Michael Lebowitz is the founding partner of 720 Global, an investment consultant specializing in macroeconomic

research, valuations, asset allocation and risk management. Our objective is to provide professional investment

managers with unique and relevant information that can be incorporated into their investment process to enhance

performance and marketing. We assist our clients in differentiating themselves from the crowd with a focus on

value, performance and a clear, lucid assessment of global market and economic dynamics. 720 Global research is

available for re-branding and customization for distribution to your clients. For more information about our

services please contact us at 301.466.1204 or email [email protected]

Read more articles by Michael Lebowitz