Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Citigroup’s Citi Surprise Index (CSI) is a real-time model, designed to analyze the accuracy of Wall Street’s economic forecasts. A positive index value indicates that recent economic data is stronger than the consensus of economists’ expectations. A negative reading denotes economic data that is worse than expectations. Unbeknownst to most investors, the CSI also serves as a gauge of sentiment and provides unique insight into how well economists understand the current economic cycle.

Appreciation for the multitude of messages provided by the CSI allows investors to stay a step ahead of the economic models that Wall Street, and -- by default -- most investors, rely heavily on to forecast market levels and securities prices. This is more important than ever now as markets are more concerned with how economic data deviates from forecasts and less concerned with the absolute reading of the very same data and what it signifies for economic growth.

The Citi Surprise Index

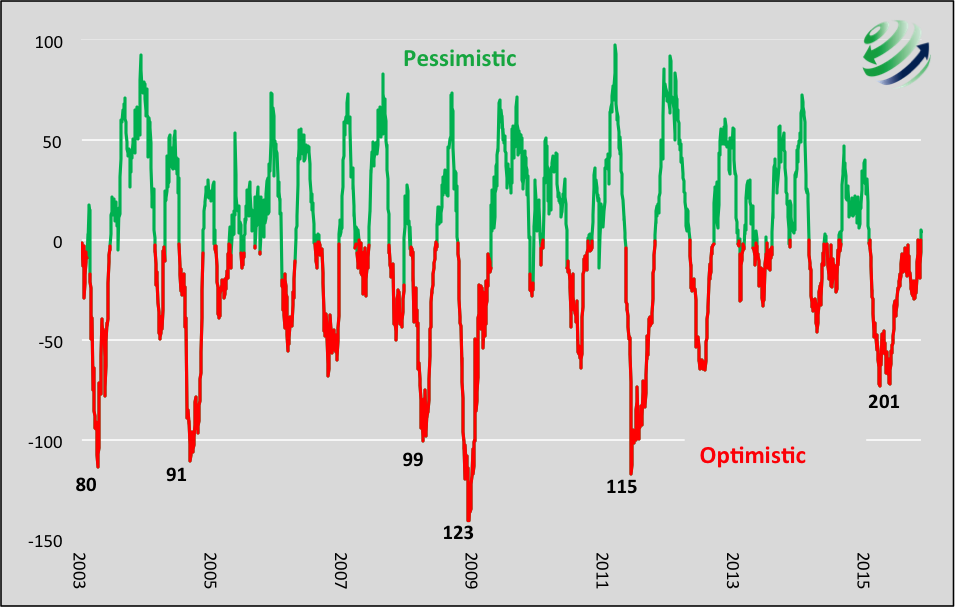

The graph below plots the CSI since 2003. Positive readings are in green and negative readings in red. A positive reading means economists have underestimated economic data, thus the label “pessimistic” in green at the top. Conversely, negative readings indicate economists have overestimated economic data, thus the label “optimistic” at the bottom. The figures below selected points are the number of days the index was consecutively negative (more on that later).

The simple takeaway from the chart is that economists constantly shift between periods in which they are overly optimistic and overly pessimistic. This gyration is to be expected as economists notice errors in their forecasts and adjust their models to reflect the current environment. Interestingly, the adjustments do not result in better forecasts, as evidenced by the continual seesaw pattern of the index.

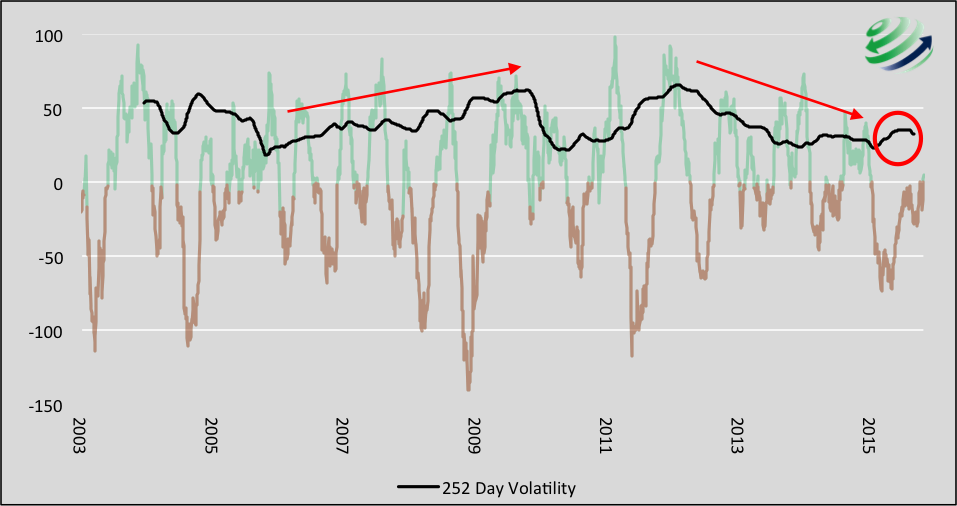

The second graph further highlights this point by plotting the one-year volatility (standard deviation) of the index. This graph illustrates the extent to which economists’ consensus forecasts deviated from the actual outcome without regard for direction. Since 2003, there were gradual ebbs and flows in the volatility of the index but not a clear sustainable downward trend, which would signal an improvement in forecasting skills.

|

Citi Surprise Index since 2003

|

|

|

Data Courtesy; Bloomberg, Citigroup, 720 Global

|

|

Citi Surprise Index with 252 day Volatility Overlay

|

|

|

Data Courtesy; Bloomberg, Citigroup 720 Global

|

720 Global considers three factors to interpret this data set:

- The duration of forecasting errors is the amount of time the index is consecutively positive or negative. Said another way, it is the length of time that economists consistently over- or under-estimate economic data. Longer periods of consistent over- or underestimation are a warning that economists are slow to recognize the economy is accelerating or decelerating at a different pace than that of the prior months.

- The magnitude of errors is how far the index is from zero. Readings significantly below or above zero indicate that consensus forecasts are missing by a wide margin. This alerts one to the magnitude in which economic trends are not being captured. More alarmingly though, it can signify that economists are tardy in their recognition of a change in the direction of the trend.

- Volatility measures the variability of forecasting errors over time. When volatility trends upwards, it is an indicator that economists have been experiencing increasing difficulty forecasting actual outcomes. Likewise, a downward sloping volatility trend signifies economists are more in tune with changes in the economy. In simple words, volatility trends indicate the grasp that economists have on the state of the economy.

Observations during the great financial crisis (2008-2009)

The great financial crisis of 2008-2009 took markets, economists and the Federal Reserve by surprise. Very few economists forecasted the recession, and even fewer predicted the punishment it would inflict on the banking sector and the markets as a whole.

Would the CSI, as viewed through the three aforementioned factors, have alerted investors to the increasing difficulty economists were having in forecasting the state of the economy and hopefully made them less reliant on such forecasts?

One-year volatility of CSI, a measure of longer-term volatility over a 252-business-day period, started rising in the first months of 2006, more than two years before the crisis took hold. In both January and October of 2007, 50-day volatility, a measure of shorter-term volatility experienced substantial shocks of over two standard deviations. So, while the pre-crisis years of 2006-2007 lacked a significant duration or magnitude change in the index, which typically accompanies economic change, the increasing trend in long-term volatility and bursts of short-term volatility should have raised awareness to the increasing risks building in the economy and the growing inaccuracy of Wall Street forecasts. In 2008, as crisis and recession set in, there was a 99-day and a 123-day period of negative consecutive readings, the longer of which was of record magnitude.

Current observations

The index just ended its longest period (201 days) of consecutively negative readings. Think of this as overly optimistic forecasting of economic data. However, as compared to 2008-2009, the magnitude of the over-optimism is relatively small.

While certainly not dire, this trend of excessive optimism is worth observing. After peaking in early 2012, longer term CSI volatility steadily decreased until the beginning of 2015 at which point it reversed. In March of 2015, the short-term volatility gauge spiked over one standard deviation higher but remained well below the levels witnessed prior to 2008.

Economists have been consistently over-estimating the strength of the economy this year. The magnitude of their misses is not particularly worrisome, but volatility measures and the recent record number of consecutive negative readings are suggesting that economists’ models are losing their grasp on the state of the economy.

Summary

The CSI is one of many tools offering deeper insight to investors attempting to gauge the market environment. Most observe the CSI superficially through a one-dimensional lens and fail to consider the broad implications it offers. The three factors described above give investors a better assessment of embedded information most do not consider.

The CSI allows one to evaluate:

- The length of time that actual economic data has been better or worse than expectations, and thus the optimistic or pessimistic leanings of economic forecasters;

- The amount forecasts deviate from actual results; and

- The consistency, or lack thereof, of forecast errors.

Paying attention to the signals the CSI sends in various forms allows one to see changes not readily apparent to the superficial observer.

Michael Lebowitz is the founding partner of 720 Global, an investment consultant specializing in macroeconomic research, valuations, asset allocation and risk management. Our objective is to provide professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and marketing. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. 720 Global research is available for re-branding and customization for distribution to your clients. For more information about our services please contact us at 301.466.1204 or email [email protected]

Read more articles by Michael Lebowitz