To read DALBAR's response to this article, go here.

DALBAR’s Quantitative Analysis of Investor Behavior report is commonly cited as “proof” that mutual fund investors have historically made poor market-timing decisions. While DALBAR does not publicly disclose its approach, in this article I use a transparent and industry-accepted methodology, based on publicly available data[1], to demonstrate that investors’ returns have not been nearly as bad as DALBAR claims.

Two recent Advisor Perspectives articles, the first by Michael Edesess and the more recent by Wade Pfau, explored whether the market-timing decisions made by mutual fund investors were rational and intelligent. The majority of the research suggests that the average mutual fund investor doesn’t do a very good job timing the market (i.e., is “dumb”). But there are significant differences in the estimates of how much these poor decisions have affected performance. For example, DALBAR suggests that equity mutual fund investors have underperformed the S&P 500 by over 600 basis points annually. In contrast, Russ Kinnel, my colleague at Morningstar Research Services[2], has noted a more muted impact in his annual Mind the Gap report, typically in the neighborhood of 100 basis points annually.

In this piece, I’ll conduct my own analysis using historical mutual fund data to better calibrate the intelligence of mutual fund investors’ market-timing decisions.

Winners and losers

Every active investor (i.e., one who doesn’t hold the market-capitalization weighted portfolio) will lose or make money, and there will be a corresponding, offsetting winner or loser. While there can be more winners than losers (and vice versa), the asset-weighted alpha must be zero before fees (i.e., a lot of investors can win if one large investor loses). This is an important point Edesess made regarding the potential impact of timing decisions, whereby any “alpha,” be it positive or negative, is a zero-sum game in the aggregate (before fees).

One of the most commonly cited examples of the zero-sum game nature of alpha is that actively managed portfolios can’t (or shouldn’t) collectively outperform passive (i.e., index-tracking) investments. This is because passive investments, at least those that are market-cap weighted, hold the market.[3] Active funds can change only the relative weights of individual holdings; the market universe is the same. Therefore, for every dollar invested actively, one must lose.

This same zero-sum paradigm applies to timing decisions, which we can think of as how weighting decisions change over time. One important wrinkle when thinking about this paradigm for a specific set of investments, such as mutual funds, is that mutual fund investors don’t represent the entire market. Most mutual funds are actively managed, and there are a variety of other vehicles an investor could use to gain exposure to the stock or bond markets, such as purchasing securities directly, buying a passive ETF or some type of collective vehicle, futures, forwards, etc. So the average alpha for mutual fund investors as a whole could be positive or negative.

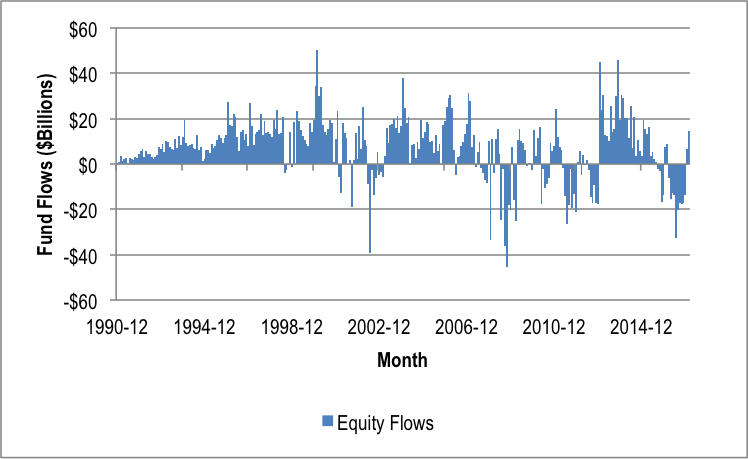

When thinking about the potential alpha related to timing, empirical evidence suggests mutual fund investors have been losers, on average. We see this in Exhibit 1, which includes historical monthly data on net flows for mutual funds obtained from Morningstar Direct.

Exhibit 1: Monthly Flows for US Equity Mutual Funds

If mutual fund investors on average made “smart” market-timing trades, there would most likely be inflows into equity funds at market bottoms and outflows at market tops. What we see, though, is effectively the opposite, where net equity mutual fund flows are positive after the market does well and negative after the market does poorly (such as following the dot-com and 2007 market crashes). This is not a wealth-maximizing decision by investors. I don’t know who was on the other side of these trades making money, but there is relatively strong evidence just looking at fund flows that mutual fund investors as a whole have made bad timing decisions.

But what has been the cost of these poor decisions?

This brings us to DALBAR’s “Quantitative Analysis of Investor Behavior” report (which I will refer to as DALBAR or DALBAR’s research), which is published annually. DALBAR’s research is one the best-known and frequently advisor-cited pieces of investors behaving poorly. The numbers in the DALBAR report suggest that the “average investor” has been very poor market-timing decisions. For example, in its 2016 analysis (data as of December 31, 2015) DALBAR noted that while the S&P 500 has had an average annual return of 10.35%, the average investor return has only been 3.66%.

What gives? Like Edesess, Pfau and others who’ve commented on this topic, there are a few significant issues with the DALBAR analysis, which I’ll dig into.

The problems with DALBAR’s calculation

DALBAR has a significant flaw in its calculation. It considers its methodology proprietary and, based on publicly available information, Pfau conducted a relatively comprehensive analysis. He concluded that DALBAR is likely comparing the return for a lump-sum investment to the return for a dollar-cost-averaged investment. This means the results are meaningless – essentially comparing apples to oranges.

Pfau also noted that while there is the potential for there to be a difference in returns realized by mutual fund investors and the general return of the market, it should be much smaller than the figures DALBAR cites in its report. Along these lines Morningstar, Inc. has been estimating the returns realized by “average” mutual fund investors since 2006, when it introduced its “investor return” metric. Investor return is an internal rate-of-return calculation based on the beginning total net assets, all net monthly cash flows and ending total net assets. The approach Morningstar uses to estimate investor return should be very similar to DALBAR’s approach: a dollar-weighted analysis of mutual fund returns. While Morningstar has a methodology document that is publicly available, DALBAR does not publicly release its methodology.

Each year Kinnel puts out a report summarizing Investor Returns in a piece titled, Mind the Gap. The “gap” is the difference in the total return (i.e., mutual fund reported performance) and the investor return (i.e., average investor return accounting for cash flows). Consistent with the results of DALBAR, the gap Kinnel has noted in his reports is generally negative. This suggests investors have made poor timing decisions, on average, which would be consistent with the net equity flows data we see in Exhibit 1. The actual gap, though, has only been about 1% annually. This is significantly lower than DALBAR’s estimate and is worth exploring in greater detail.

Analysis

I performed my own analysis to quantify how timing decisions have affected the realized return for the average mutual fund investor. I estimated investor returns and total returns based entirely on historical mutual fund assets and net fund flow data obtained from Morningstar. The investor return I calculated uses the identical approach Morningstar describes in the methodology document referenced above.

Instead of using investor returns that were pre-calculated by Morningstar (available in Morningstar DirectSM), I performed all calculations myself in Excel using the IRR function (with the total return as the initial guess). As a reminder, the total return is the conventional time-weighted return, which is also commonly referred to as the compound rate of return or the geometric mean return. It reflects a buy-and-hold strategy, and is the return figure most commonly cited by mutual fund companies when presenting performance.

I used monthly mutual fund total assets and net monthly flows obtained from Morningstar Direct from December 1990 to December 2016 (26 years). I selected December 1990 as the start date because asset data before this for many mutual funds was available only quarterly. The dataset covers 60,488 funds over the entire time period and is survivorship-bias free (i.e., it includes all U.S.-based mutual funds that have existed over the period regardless if they were still in existence as of December 2016).

Since I’m using the same data to estimate both the investor return and the total return, any differences can be attributed entirely to differences in cash-flow timing. This is important since it better isolates the true impact of timing decisions. In contrast, DALBAR compares the performance of all equity fund investors to the S&P 500 Index. While the S&P 500 is a well-known and widely used index, this isn’t a fair comparison because it isn’t representative of all the underlying securities in mutual funds. The Index also doesn’t include expense ratios, which are an obvious drag on returns (but irrelevant to the timing discussion).

For the analysis, I grouped individual mutual funds either by Morningstar category[4] or by broad asset class. For the Morningstar categories, I included all mutual funds that had a Morningstar category assigned for that respective month. The fund group is reconstituted monthly, so if a mutual fund changed category it would be excluded from the respective month. Style drift has a potential to impact the analysis, but I included the category analysis for robustness. Only large categories that are relatively stable are included in the analysis to minimize the impact of style drift.

I included the three broad asset classes: equities, fixed income and allocation funds. Those asset classes include all their underlying categories. For example, the broad asset class “equities” includes all U.S.-based equity funds. Many of these funds may invest abroad, but they are being purchased by U.S. investors. Allocation investments are prepackaged allocation strategies, such as balanced funds or target-date funds. Assets and net flow data are aggregated across funds within the broad asset class each month.

Exhibit 2 includes the results of my analysis over the 26-year test period. As a reminder, the “gap” return is the simple difference between the total return and the investor return for the respective test group.

Exhibit 2: Minding the Gap: December 1990-December 2016

|

Morningstar Category

|

Investor Return

|

Total Return

|

Gap

|

|

Large Growth

|

10.04%

|

12.94%

|

-2.90%

|

|

Large Blend

|

8.09%

|

9.48%

|

-1.39%

|

|

Large Value

|

9.36%

|

10.16%

|

-0.80%

|

|

Foreign Large Blend

|

2.79%

|

5.03%

|

-2.25%

|

|

World Stock

|

8.01%

|

9.90%

|

-1.90%

|

|

Intermediate-Term Bond

|

5.25%

|

6.72%

|

-1.47%

|

|

Intermediate Government

|

7.06%

|

6.46%

|

0.60%

|

| |

|

|

|

|

Broad Asset Class

|

Investor Return

|

Total Return

|

"Gap"

|

|

Equity

|

7.13%

|

8.69%

|

-1.56%

|

|

Fixed Income

|

4.80%

|

6.09%

|

-1.28%

|

|

Allocation

|

6.61%

|

8.43%

|

-1.82%

|

For each of the Morningstar categories except intermediate-government bond, and for all of the broad asset classes, the gap was negative. The investor return was lower than total return by about 150 basis points on average. The negative gap is consistent with what we should expect given historical equity net flows, which suggest the average mutual fund investor has not made smart timing decisions.

My numbers are significantly lower than those estimated by DALBAR, but are more consistent with other published research on mutual fund time-weighted returns.

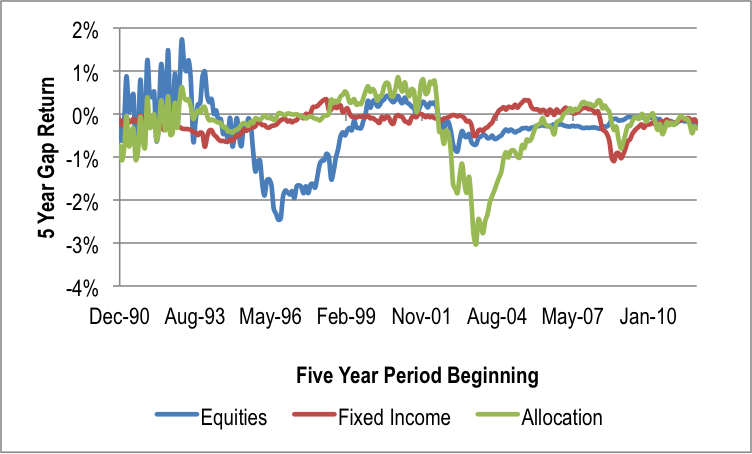

Investor returns differ significantly by period, even more so the shorter the period. For example, Exhibit 3 includes the gap return for rolling five-year periods for the 26 calendar years of the analysis for the three broad asset classes.

Exhibit 3: Rolling Annualized 5-Year Return Gap for Various Broad Asset Classes

Looking at rolling five-year periods, the average investor doesn’t look nearly as bad. For example, the average five-year gap is much lower than the average gap return over the entire period, averaging -0.32%, -0.16%, and -0.23%, for equities, fixed income, and allocation, respectively. These findings are more consistent with what one would expect based on Edesess’ piece and demonstrate how important the time frame is for the analysis. Overall, it provides strong evidence that while mutual investors have not necessarily been good market timers, they haven’t been as off-base as the DALBAR analysis claims.

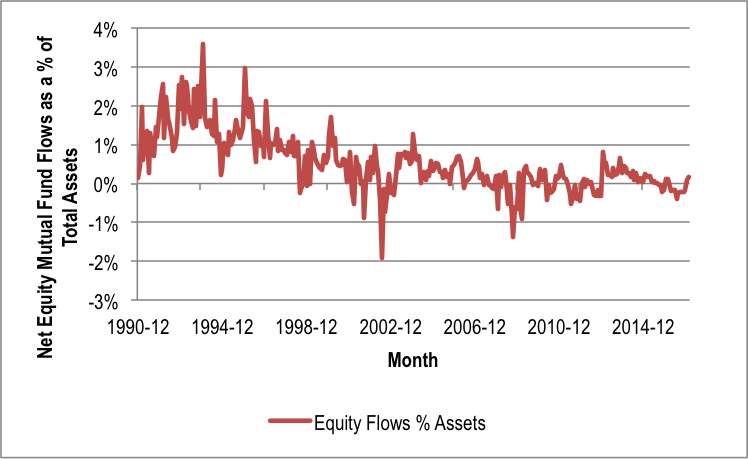

Another takeaway from Exhibit 3 is that investors are getting smarter; that the gap has been narrowing toward 0% over time. A key reason for this is that net flows as a percentage of total assets have declined over time. For example, net equity flows in my dataset didn’t exceed 0.3% of assets in 2015 on an absolute basis (positive or negative) for a single month, which is very similar to the flows noted by DALBAR (page 10), which also appear to be roughly between 0.3% of assets. Equity mutual fund flows have declined since December 1990, as shown in Exhibit 4.

Exhibit 4: Net Equity Mutual Fund Flows as a Percentage of Total Assets

The reduction in relative mutual fund flows can be attributed to a variety of factors, including competing products capturing assets (e.g., ETFs) and a general maturation of the industry. But we haven’t seen a significant change in how long investors are holding funds or mutual fund managers hold stocks. In other words, while fund investors are getting smarter (the decreasing gap return), this is just a byproduct of less money going into mutual funds. As relative flows decrease, the relative difference between the dollar-weighted (investor return) and time-weighted (total return) are going to shrink as well. If fund flows continue to contract, gap return will be relatively small in the future, especially for asset classes with low relative flows versus total assets.

Who is the average investor?

One incredibly important point that most studies ignore when discussing the market-timing intelligence of the “average investor” is that mutual fund flows reflect the decisions made by all investors. This includes not only do-it-yourself investors, which is often the implied average investor, but also individuals receiving advice from an investment professional (e.g., financial planners, financial advisors). Therefore, to suggest a client working with an advisor is going to be immune to poor timing decisions (as DALBAR infers) ignores the fact many advisors are (and have been) subject to the same poor timing biases as clients.

There is no way to perfectly isolate the flows from attributable to each type of investor relationship (i.e., self-directed or using an advisor). While it’s possible to look at individual share classes (e.g., C-shares that are sold only through intermediaries) this still wouldn’t capture the complete picture given the change in share class usage over time (i.e., assets have leaving funds because of compliance reasons, not advisor decisions).

Ironically, one type of advisor compensation that likely resulted in inferior market timing decisions was selling mutual funds with a front-loaded commission. If advisors get paid only when they sell a fund, they have less incentive to de-bias a client from making a poor decision. While some regulators bemoan fee-based accounts since they enable advisors to get paid to “do nothing,” the evidence from this research suggests that for many investors doing nothing may be a lot better than doing something.

Conclusions

DALBAR’s numbers are wrong and should not be cited in the context in which they are commonly used. My findings empirically verify what Pfau claimed DALBAR’s results should be.

While mutual fund investors as a group made poor timing decisions, that doesn’t mean all investors have underperformed an appropriate market benchmark. Outperformance (i.e., alpha from market timing) is a zero-sum game in the aggregate (this was Edesess’ point). While I’m relatively certain mutual fund investors have underperformed (i.e., are poor market timers), I don’t know who the winners were.

Finally, the “average investor” includes not only self-directed individuals, who DALBAR’s research commonly targets, but also those who receive advice from financial planners and investment professionals. Those professionals are subject to the same biases as self-directed investors.

Mutual fund investors haven’t made exceptional timing decisions, but they haven’t been nearly as dumb as the DALBAR numbers claim. It’s hard to beat the market – especially through market timing – and few investors have been able to do it consistently for any reasonable time period. Investors and financial advisors should follow a disciplined approach that is focused on staying invested for the long-term rather than trying to beat the average investor (whomever he or she may be).

David Blanchett, PhD, CFA, CFP® is the head of retirement research for Morningstar Investment Management, LLC.

Disclosures

The information, data, analyses, and opinions presented herein do not constitute investment advice; are provided as of the date written and solely for informational purposes only and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate.

This article contains certain forward-looking statements. I use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/ or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results.

[1] Available in Morningstar DirectSM

[2] I acknowledge there is some potential conflict of interest/bias here since Kinnel and I both work at Morningstar. We work in different silos, though – he for Morningstar Research Services LLC, a registered investment adviser and subsidiary of Morningstar, Inc., and I for Morningstar Investment Management LLC, a registered investment adviser and a separate Morningstar subsidiary.

[3] In reality, there can be notable potential differences in the true market and the actual index holdings, especially given the increasingly diverse definition of what is considered an “index” or “passive” today, but conceptually I think this statement is true.

[4] Morningstar Categories are a proprietary Morningstar data point. While the investment objective stated in a fund’s prospectus may or may not reflect how the fund actually invests, the Morningstar category is assigned based on the underlying securities in each portfolio. Morningstar categories help investors and investment professionals make meaningful comparisons between funds. The categories make it easier to build well-diversified portfolios, assess potential risk, and identify top-performing funds. We place funds in a given category based on their portfolio statistics and compositions over the past three years. If the fund is new and has no portfolio history, we estimate where it will fall before giving it a more permanent category assignment. When necessary, we may change a category assignment based on recent changes to the portfolio.

Read more articles by David Blanchett