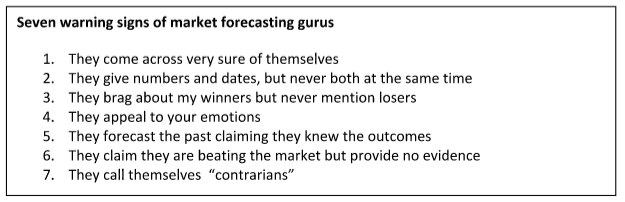

Much as I want to know the future, I’ve long since recognized the dangers of our addiction to predictions, which are usually heralded by so-called market gurus. I’ll give you seven surefire ways to spot those purveyors of bad advice, but first let’s look at a far more useful set of forecasts.

For a prediction to gain media exposure, two things are critical. First is precision. We want to know with a great degree of certainty what the stock market will return in 2018. Second is compelling logic. We want to feel confident that our nest egg and that of our client’s is invested on a firm footing.

Unfortunately, there is a mountain of evidence that market predictions aren’t just lousy; they are less accurate than random guesses. While not as emotionally appealing as a single-point prediction, probabilistic forecasts are more useful because they allow you to evaluate the consequences of possible scenarios.

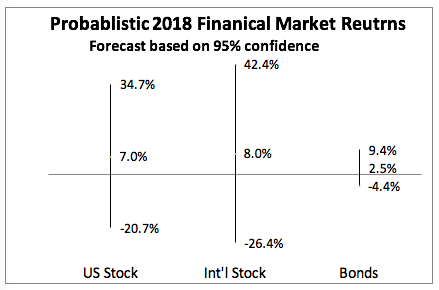

Here are my probabilistic market predictions and, even more importantly, the implications for your clients’ portfolios. Each prediction is made with a 95% confidence level, meaning I expect actual outcomes to be within this range 19 out of every 20 years.

1. The U.S. stock market will return between -21.7% and +34.7%

Stocks have historically earned approximately 7% after inflation. I just can’t resist the temptation to lower it a bit to 5% based on fairly rich valuations. So my midpoint is a 7% nominal return, or a 5% real return, if the Fed hits its 2% target inflation rate. Next, I take the 15-year historic standard deviation of 13.85% from Morningstar and apply two standard deviations to get a 95% confidence level. The Minneapolis Federal Reserve estimates the odds of a bear market being greater than my estimate at approximately 8%.

The implication is that stocks have a greater than 50% shot at beating inflation but are risky. We need only to look back to 2008 when U.S. stocks lost about 36%, which was a three-standard-deviation event, meaning once every 300 years.

A plunge could be caused by a natural disaster, a military conflict (such as with North Korea) or by a terrorist attack here at home. But let’s face it, if the plunge does happen, it’s likely that it will be caused by something we haven’t anticipated. The implication to your clients is, of course, that stocks are risky. The downside may be more important than the 34.7% upside since running out of money has a much greater impact on clients.

Are your clients taking any unnecessary risk?

2. There is a 95% probability international stocks will return between -26.4% and +42.4%

Valuations are a tad better overseas so I use an 8% nominal midpoint, though Morningstar shows a much greater volatility than domestic equities, with a 17.19% standard deviation. It also is logical to assume that a more volatile asset class would have a greater expected return.

The odds are that U.S. and international stock returns will have a strong positive correlation. Yet correlations and total returns are very different. For example, YTD as of December 13, the Vanguard Total Stock Index fund (VTSMX) is up 20.35% while the Vanguard Total International Stock Market (VGTSX) is up 24.95%. In 2007, the two funds plunged 37.04% and 44.10%, respectively.

Better valuations are no free lunch, but rather compensation for taking on more risk. While I believe in owning a global portfolio, understand that it increases risk and one should make sure clients understands this.

3. There is a 95% likelihood that high-quality bonds will return between -4.4% and +9.4%

I use a different methodology here than on stocks. Rather than starting from historic returns, I look at the current nominal yield of about 2.5%. That’s because past performance is driven in large part by a 35-year period of falling interest rates, causing bond returns to increase. However, this can’t continue forever. I’m also not using economists’ forecasts of rising rates, as their past predictions have been directionally correct far less than the 50% one would expect from a coin flip. The historic standard deviations are a good start point, which Morningstar shows as 3.45% for the Bloomberg Barclays Aggregate Bond Index (AGG).

A high-quality bond fund has far less risk than stocks. Clients who have “won the game,” as financial author William Bernstein puts it, should have the majority of their assets in high-quality fixed income.

I totally reject the notion that bonds have more risk than stocks. A broadly diversified stock fund has more risk in a day than a similarly diversified high-quality bond fund, such as iShares Aggregate Bond Fund (AGG), has in a year. Never forget that on Black Monday 1987, stocks lost over 20% in one day, which equates to six standard deviations (six sigma) of the AGG in one year, meaning it should happen no more often than once out of every 294,117 years.

Naturally, corporate investment-grade bond funds and junk-bond funds have greater yields than high-quality funds, along with much greater volatility. Even more importantly, they also have higher correlation with stocks, making them less valuable as a diversifier. That’s why I recommend taking risk with stocks and using fixed income as the portfolio’s “shock absorber.”

Why I may be understating the risk

As uncertain as the forecasts I’ve made are, actual risk may be greater and expected returns even lower. Stock and bond returns may not resemble a normal bell curve and may have fat tails. Beyond that, historic standard deviations may not be indicative of future volatility.

In addition to the above systemic risk factors, expected returns may be lower and volatility greater for most individual portfolios. That’s because these returns are before fees and the standard deviations are of the entire market. Fees lower returns. Next, a handful of stocks or picking sectors typically results in greater volatility and, often, lower returns. Research shows that the dollar-weighted returns of narrow funds are lower than broader funds.

Conclusion

You won’t see me on CNBC in the New Year touting my predictions. They are emotionally unappealing, which is exactly why they have value in planning portfolios for your clients.

My predictions fail all seven of the warning signs of a market forecasting guru.

Instead, help them understand the implications of the downside returns in the context of a range of possible outcomes. Risk is a combination of the probability of an outcome and the implications of the event becoming reality.

When your client wants more certainty, tell them they can’t have it. I’ve managed to build a financial-planning practice where telling clients that I don’t know the future is job one, and that it’s the single most important advice I have to give.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth