Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“I’m a low interest rate person” - Donald Trump 2016

On Donald Trump’s hit TV show, The Apprentice, contestants competed to be Trump’s chief apprentice. Predictably, each show ended when the field of contestants was narrowed down by the firing of a would-be apprentice. While the show was pure entertainment, Trump’s management style was on full display. Trump has run private organizations his entire career. Within these organizations, he had a tremendous amount of unilateral control. Unlike what is required in the role of president or that of a corporate executive for a public company, Trump largely did what he wanted to do.

On numerous occasions, Trump has claimed the stock market is his “mark-to-market.” In other words, the market is the barometer of his job performance. This is a ludicrous comment and one that the president will likely regret. He has made this comment on repeated occasions. Whether he believes it or not, he has tethered himself to the market as a gauge of performance in the mind of the public. There is little doubt that the president will do everything in his power to ensure the market does not make him look bad.

Warning shots across the bow

On June 29, 2018, Trump’s Economic Advisor Lawrence Kudlow delivered a warning to Chairman Powell saying he hoped that the Federal Reserve (Fed) would raise interest rates “very slowly.”

Almost a month later we learned that Kudlow was not just speaking for himself but likely on behalf of his boss, Trump. During an interview with CNBC, on July 20, 2018, the president expanded on Kudlow’s comments voicing concern with the Fed hiking interest rates. Trump told CNBC’s Joe Kernen that he does not approve [of rate hikes], even though he put a “very good man in” at the Fed referring to Chairman Powell.

“I’m not thrilled,” Trump added. “Because we go up and every time you go up they want to raise rates again. I don't really — I am not happy about it. But at the same time I’m letting them do what they feel is best.”

“As of this moment, I would not see that this would be a big deal yet but on the other hand it is a danger sign,” he said.

Two months later in August of 2018, Bloomberg ran this article: Trump Said to Complain Powell Hasn’t Been Cheap-Money Fed Chair.

Quoting from that article: “President Donald Trump said he expected Jerome Powell to be a cheap-money Fed chairman and lamented to wealthy Republican donors at a Hamptons fundraiser on Friday that his nominee instead raised interest rates, according to three people present.”

On October 10, 2018, following a 3% sell-off in the equity markets, CNBC reported on Trump’s most harsh criticism of the Fed to date. Trump said, "I think the Fed is making a mistake. They’re so tight. I think the Fed has gone crazy."

Those comments and others come as the Fed is publically stating its preference for multiple rate hikes and further balance sheet reduction in the coming 12-24 months. The markets, as discussed in this article Everyone Hears the Fed but Few are Listening, are not priced for the same expectations. This is becoming evident with the pickup in volatility in the stock and bond markets. There is little doubt that a hawkish tone from Chairman Powell and other governors will increasingly wear on an equity market that is desperately dependent on ultra-low interest rates.

Who can stop the Fed?

There is an obstacle that might stand in the Fed’s way of further rate hikes and balance sheet reductions.

Consider a scenario where the stock market drops 20-25% or more, and the Fed continues raising rates and maintaining a hawkish tenor.

This scenario is well within the realm of possibilities. Powell does not appear to be like Yellen, Bernanke or Greenspan with a finger on the trigger ready to support the markets at early signs of disruption. In his most recent press conference on September 26, 2018, Powell mentioned that the Fed would react to the stock market but only if the correction was both “significant” and “lasting.”

The word “significant” suggests he would need to see evidence of such a move causing financial instability. “Lasting” implies Powell’s reaction time to such instability will be much slower than his predecessors. Taken along with his 2013 comments that low rates and large-scale asset purchases (QE) “might drive excessive risk-taking or cause bubbles in financial assets and housing” further supports the notion that he would be slow to react.

Implications

President Trump’s ire over Fed policy will likely boil over if the Fed sits on their hands while the president’s popularity “mark-to-market” is deteriorating.

This leads us to a question of utmost importance. Can the president of the United States fire the chairman of the Fed? If so, what might be the implications?

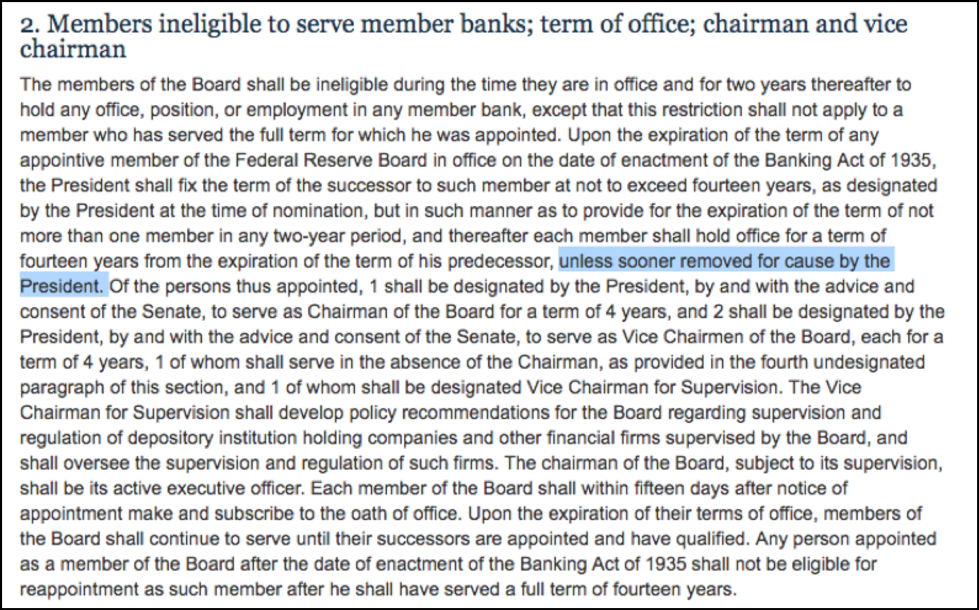

The answer to the first question is “yes.” Pedro da Costa of Business Insider wrote on this topic. In his article (link) he shared the following from the Federal Reserve Act (link):

Given that the president can fire the Fed chairman for “cause” raises the question of implications were such an event to occur. The Fed was organized as a politically independent entity. Congress designed it this way so that monetary policy would be based on what is best for the economy in the long run and not predicated on the short-term desires of the ruling political party and/or president.

Although a president has never fired a Fed chairperson since its inception in 1913, the Fed’s independence has been called into question numerous times. In the 1960s, Lyndon Johnson is known to have physically pushed Fed Chairman William McChesney Martin around the Oval Office demanding that he ease policy. Martin acquiesced. In the months leading up to the 1972 election, Richard Nixon used a variety of methods including verbal threats and false leaks to the press to influence Arthur Burns toward a more dovish policy stance.

If hawkish Fed policy actions, as proposed above, result in a large market correction and Trump were to fire Fed Chairman Powell, it is plausible that the all-important veil of Fed independence would be pierced. Although pure conjecture, it does not seem unreasonable to consider what Trump might do in the event of a large and persistent market drawdown. Were he to replace the Fed chair with a more loyal “team player” willing to introduce even more drastic monetary actions than seen over the last 10 years, it would certainly add complexity and risk to the economic outlook. The precedent for this was established when President Trump recently nominated former Richmond Fed advisor and economics professor Marvin Goodfriend to fill an open position on the Fed’s Board of Governors. Although Goodfriend has been critical of bond buying programs, “he (Goodfriend) has a radical willingness to embrace deeply negative rates.” – The Financial Times

Such a turn of events might initially be very favorable for equity markets, but would likely raise doubts about market values for many investors and raise serious questions about the integrity of the U.S. dollar. Lowering rates even further leaves the U.S. debt problem unchecked and potentially unleashes inflation, a highly toxic combination. A continuation of overly dovish policy would likely bolster further expansion of debt well beyond the nation’s ability to service it. Additionally, if inflation did move higher in response, bond markets would no doubt eventually respond by driving interest rates higher. The can may be kicked further but the consequences, both current and future, will become ever harsher.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics.

Read more articles by Michael Lebowitz