I take a lot of flak when I write about annuities. That criticism has come from the insurance industry, because I have been highly critical of products like fee-laden variable annuities with complex menus of riders. But recent discussions and a new analysis have led me to reconsider single-premium immediate annuities (SPIAs) as a source of longevity insurance at a reasonable cost.

Despite the simplicity and low cost of the SPIA, I have not recommended them. But the amount of push back I received from people I respect, such as Wade Pfau of the American College and Joe Tomlinson, actuary and former financial planner, has persuaded me to take another look. I discussed the subject with both of them.

A SPIA provides longevity insurance via mortality pooling – those who live short lives subsidize those who live longer ones. I also agree with Pfau and Tomlinson that it can dampen stock market sequence of returns risks. Reducing sequence risk, however, can also be accomplished with other fixed-income investments such as laddered bond portfolios.

I’ll look at the mortality-adjusted returns from a SPIA and compare them to corporate and Treasury bond ladders. I’ll then look at an important risk – inflation – and then step back to assess the pros and cons of SPIAs.

Calculations of expected returns

I went to ImmediateAnnuities.com and got a quote for a 65-year old male. I took the highest payout for a life-only option to be most fair to the product. Reducing payouts with options like life with a period certain or life with cash refund lowers the monthly payment and is counterproductive – insuring for both a very long and very short life. I’m assuming the actuaries would also price other ages and joint annuities based on life expectancy tables so this would be representative.

The best quote for a $100,000 SPIA was $570 a month. That translated to $6,840 or a 6.84% cashflow. I was impressed it was displayed as “cashflow” rather than “yield” or “income,” since some of that payment is return of principal. The SPIA was offered by Lincoln National Life with an AA- rating by S&P.

I then built a spreadsheet to calculate the annualized returns based on life expectancy tables from the Society of Actuaries and the American Academy of Actuaries, using a non-smoker in excellent health to be most beneficial to the annuity.

The results, shown in the table below, surprised me:

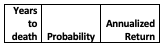

Excellent health – no smoking

Using the 23-year average life-expectancy, the SPIA produced a 4.36% annualized return. This return, as well as those for longer lives, reflects the benefit from mortality pooling that increases with age. Living 40 years to age 105 resulted in a 6.47% annualized return. Though I understand returns would be negative with a short life, the key purpose of retirement planning is to fund one’s lifestyle. I tell clients passing money on to the kids is only a secondary goal.

I built a high-level model to compare the above returns to bonds, which came out fairly close to results from a web tool, AACalc.com, recommended by Tomlinson. Comparing the above return of a SPIA at a 23-year life expectancy to corporate bonds, I would expect to get the equivalent cash flow if I had built a bond ladder of $92,400 in bonds providing a $570 a month cash flow. If I did the same with U.S. Treasury bonds, it would cost me $109,200 in bonds.

I argue the corporate bonds are a better comparison since they approximate the credit risk of the insurer issuing the SPIA. The benefit of a possible guarantee from a state guaranty fund is offset by both the lack of diversification and liquidity. The extra $7,600 cost ($100K less the $92,400 above to build a bond ladder of 23- years) is essentially a net premium for the longevity insurance. If compared to a roughly half corporate and half Treasury portfolio, the bond portfolio returns about the same as the SPIA, making the cost of insurance essentially zero.

How could Lincoln National take on the risks associated with this product with small margins? As of the end of 2017, its latest annual report, 86% of its investments were in fixed income, so it might be reasonable to expect Lincoln to earn a fixed-income-like return less commissions, costs and insurance company profits. However, Tomlinson points out that it’s possible that such large insurance companies can find fixed-income investment opportunities that earn a yield premium over the public corporate bond market. The other 14% of investments could perhaps also earn more.

The value of the longevity insurance

It’s nice to know what your check will be every month. Pfau writes:

A retirement income bond ladder can be structured so the cash flows provided through coupons and maturing face values will provide a steady and known stream of contractually guaranteed income for the ongoing expenditure needs in retirement.

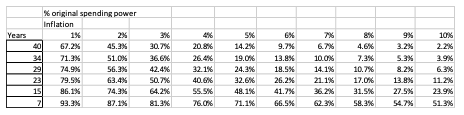

This SPIA payments accomplish the same thing, plus it provides longevity insurance for after the bond ladder has been spent down. Unfortunately, what matters is our spending power. For example, in 34 years (to age 99; a 10% chance of living that long), that payment only buys about 37% of current purchasing value at a 3% historical inflation rate. If, and I hope not, we have hyperinflation of 10% (possibly due to deficit spending), this buys less than 4% of current purchasing power. Thus, buying this SPIA reduces longevity risk but increases inflation risk.

However, a bond ladder suffers from the same problem if the actual inflation in retirement expenses exceeds inflation assumed in setting up the bond ladder. For that reason, I don’t recommend buying long-dated maturities given the relatively flat yield curve today:

The table above shows the reduction in purchasing power due to inflation based on the amount of time (vertical columns) and the inflation rate (horizontal rows). Each cell represents the percentage of purchasing power at the end of the time period, relative to the starting date.

An inflation-adjusted annuity

It is possible to insure against both longevity and inflation. ImmediateAnnuities.com shows that the Principal Financial Group has an unlimited inflation-protected SPIA (although its media-relations group declined to confirm this and I do not have a policy to confirm). Using the same 65-year-old male, it pays $404 per month, far less than the $570 fixed payment annuity. But that assures the payment will keep up with the overall inflation rate, based on the CPI-U.

I ran those cash flow through AACalc, and determined that one would need only $95,000 in a TIPS ladder for the same expected return. Thus, comparing the $109,200 in the nominal Treasury bonds to the $95,000 of the TIPS, tells me it costs roughly $14,200 to insure against inflation risk. Inflation risk is harder and more expensive for any insurance company to hedge than longevity risk, which it can do via risk pooling.

Conclusions

A SPIA provides some longevity insurance at a reasonable rate. Even using a corporate-bond comparison, the cost of longevity insurance isn’t terrible; if one assumes the proper comparison is half Treasury and half corporate bonds, the longevity insurance is free.

But, unless an inflation-adjusted SPIA is chosen, the longevity insurance does not provide steady spending power. One must consider whether inflation over dozens of years of compounding is riskier than a long life.

It’s very expensive to insure against high inflation and a long life.

Both Pfau and Tomlinson agree with me that the best inflation-adjusted government-backed annuity is delaying Social Security. Both also agree that it would be hard to imagine a situation where the client would take Social Security early and buy a SPIA, since delaying Social Security is the superior government-backed inflation adjusted annuity. While we can’t forecast future interest rates, with the relatively flat yield curve, going long is taking on a lot of duration (interest rate) risk for a relatively small additional reward. That is true if one builds the bond ladder or buys the SPIA.

Here’s my assessment of the pros and cons of buying the SPIA:

The older the client, the greater the value of the mortality pooling benefit and the more economic sense it could make to buy such a product but, even then, only after delaying Social Security.

It’s important that we examine the role of incentives in our recommendations. Annuities typically pay commissions, which fee-only advisors argue have greater conflicts. But those same fee-only advisors charging a percentage of assets have an incentive to recommend against a SPIA as it is typically outside of the AUM fee structure. Behavioral economist Meir Statman of Santa Clara University refers to the latter as committing “annuicide,” because that AUM fee-only advisor lost assets on which to charge ongoing fees.

Author’s note: I appreciate the help from Joe Tomlinson and Wade Pfau in working on this piece and acknowledge they do not agree with all of my points.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth