Want to build a diversified, tax-efficient, and low-cost income fund for your clients? Here’s a surprising way to do that with a broad-based index fund like the S&P 500.

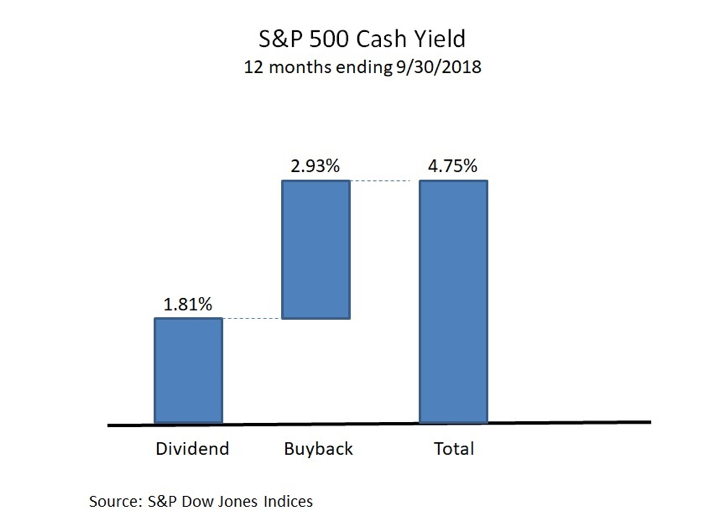

According to S&P Dow Jones Indices, the S&P 500 had a 4.75% yield for the 12 months ending September 30, 2018. That yield came from a 1.81% dividend yield and 2.93% stock buyback yield1. You or your clients may say you can’t spend the buyback yield. I beg to differ. Consider the following example.

Say you bought 100 shares of Fiduciary Consulting Co. (FCC) for $10 each a year and a day ago. Since FCC has 10,000 shares outstanding, you own 1% of the company (100/1,000). FCC made $6,000 over the past year, or 60 cents per share, and wants to return it to shareholders. Let’s also say that FCC stock went up by $2 and is now trading at $12 a share.

FCC could pay a 5% dividend and you’d receive $60 and be taxed at 15% (unless your income is very high) on your federal tax. You’d pay $9 in taxes and be left with $51.

FCC could also decide to buy back some stock with this $6,000 cash. At $12 a share, it can buy back 500 shares, leaving 9,500 shares outstanding. If you then sold five shares for a total of $60, your gain would be $10 and you would have a $1.50 tax from the long-term capital gain. You’d have $58.50 in your pocket and still own 1% of the company (95/9,500). Buybacks are superior to dividends because less goes to taxes.

Though the above example is simplified, the principle holds true regardless of how many shares are outstanding and how many shares you own. And you don’t have to sell your shares back to the company. You can sell them to anyone. So, if you sell 2.93% of your S&P 500 index fund, you’ve received a more tax-efficient distribution than if the companies had returned this same amount of cash via a dividend.

Granted, it may take a little time to explain this to clients. But once they see their increased after-tax cash flow, they will thank you.

Buybacks are under attack

Senators Chuck Schumer (D-NY) and Bernie Sanders (I-VT) recently wrote an op-ed in the New York Times announcing proposed legislation to limit buybacks. They wrote:

When a company purchases its own stock back, it reduces the number of publicly traded shares, boosting the value of the stock to the benefit of shareholders and corporate leadership.

For this to be true, markets would need to be very inefficient, meaning corporations would be buying back their own shares at below market value. Tamara C. Belinfanti, co-director of the Center for Business and Financial Law at NYU Law School, says it’s more complicated. In a phone interview, she told me, “although share price might increase in response to a buyback announcement it is not a given.” Belinfanti is co-author of a new book, Citizen Capitalism, which discusses buybacks going to a universal fund for social benefit.

The performance of the Invesco Buyback Achievers ETF (PKW) provides some illustrative data. It tracks an index comprised of stocks that have reduced their shares outstanding by 5% or more in the trailing 12 months. It had a total annual return of 8.17% annually over the past five years ending February 7, 2019. This lagged the overall S&P 500 by 2.62 percentage points annually. But over the 10-year period, it did slightly best the S&P 500.

Politics aside, from a shareholder-value perspective, management has a fiduciary responsibility to return cash to shareholders if it can’t earn more than its cost of equity (the returns expected by shareholders) through its own, internal capital investments within the company’s core competencies. Individuals can then allocate this capital as they see fit. There are two ways to return the capital – dividends and stock buybacks. As previously shown, buybacks are more tax-efficient.

Barry Ritholtz wrote an interesting piece for Bloomberg on why stock buybacks do so little for Americans, but he concluded that expanding the pool of Americans owning stocks is a better solution than restricting share repurchases.

Legitimate criticisms of buybacks

While I may not agree with government dictating what companies can do with the shareholder’s capital, there are some valid criticisms of buybacks, as they are more aligned with managements’ (versus shareholders’) interests in two ways. They are more beneficial to management stock options. In the FCC example, the 60-cent dividend would have caused the share price to decline by the same amount, thus making their stock options less valuable. The share buyback, however, keeps the price the same.

Second, dividends are more permanent than stock buybacks. Company share prices are typically punished badly when a dividend is cut. Not much happens when buybacks are reduced or stopped.

Conclusion

Even though management buy back shares for the wrong reasons, our clients benefit from a more tax-efficient return of capital. That is not to say you should buy companies that buy back large amounts of stock, or even funds or ETFs that buy companies buying back their own stock. Nor am I saying that a 4.75% cash yield is the same as a safe withdrawal rate.

But I’m suggesting the best equity income strategy may be buying a broad low-cost stock index fund, such a total U.S. stock fund, and letting clients know they can sell the same amount that was repurchased via stock buybacks. When compared to popular income-generating strategies, it will take a little time to educate the client that this builds a lower-cost, more diversified, and more tax-efficient income fund.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

1 The actual yields add to 4.75%, not 4.74%, because of rounding.

More Mutual Funds Topics >