In constructing financial plans, I tell clients that the second most important decision they will make is to set the overall riskiness of their portfolio by deciding upon an asset allocation. I’ll disclose the most important decision at the end.

As a financial planner, I’ve been trained to administer what’s called a “risk profile questionnaire” to new clients to determine how much of their portfolio should be in more volatile asset classes like stocks. One of the best such questionnaires I’ve seen is this survey from Vanguard. It asks questions about how clients feel about risk and when they will need their money, with the answers supposedly determining how much risk to take.

Though I’m trained to use these questionnaires, I don’t and here’s why – as well as a better way.

I love the idea that risk tolerance is something that can be quantified by answering certain questions that magically reveal what your asset allocation should be. I’m opposed to using them, however, because reality indicates they don’t work. For example, the Vanguard survey said I should be 80% in stocks, while other surveys I’ve taken put me as high as 90% stocks. The lowest stock allocation I received from a questionnaire I took recently came from Riskalyze at 55% stocks.

According to these questionnaires, I should be between 55% to 90% stocks. Yet I won’t budge from my current target of only 45% stocks for three reasons:

1. Our inconsistent desire to take risk

After more than a 10-year bull market, most of us feel pretty confident. It’s easy to feel brave when everything is up. Not so much when stocks plunge. That’s the time when we tend to want to load up on cash. Had I taken these surveys on March 9, 2009 when stocks bottomed out, I would have had a much lower appetite for risk. In fact, data shows advisors fall into the trap of taking on risk after markets surge only to pull risk off the table after a plunge.

2. Past behavior in a vacuum

I love Vanguard’s question about how I behave in times of market declines. I agree that past behavior is a good predictor of how investors will behave during the next plunge. I truthfully answer questions knowing that I bought more stocks in late 2008 and early 2009. The problem is that my answer didn’t reveal that it was the hardest thing I’ve ever done in investing – and that was when I was only about 45% in equities. Had I actually been 80% in stocks before the plunge, I doubt I would have had the cash or the courage to rebalance.

3. Need to take risk is ignored

I’ve never seen a questionnaire measure one’s need to take risk, by which I mean where the investor stands in relation to financial independence. Though I’m not a big spender, I’m well aware that I can’t take it with me. I personally find that the good thing about being frugal is that I can be rich with less money. In fact, I define financial wealth in years as (net worth / annual spending). That makes relatively conservative assumption that the portfolio keeps up with inflation and taxes. I heed the words of financial theorist and author William Bernstein who says, “When you’ve won the game, stop playing.” I don’t take risks I don’t need to take and recommend the same for my clients. I try to explain both the probabilities of bad returns and the consequences.

I spoke to Michael McDaniel, co-founder and chief investment officer at Riskalyze, which says it builds “fearless investors.” First, he stated that its survey is only a starting point. He agreed it did not address the need to take risk, but said its risk score is used by the advisor to then help the client to adjust the portfolio based on need.

McDaniel disagreed with me, however, that the risk score isn’t stable over time, telling me scores only dipped slightly and briefly during down markets like the end of 2018. He did acknowledge that they have only been tracking the scores since 2011, so it hasn’t been tested during a bear market or when markets declined by more than 50%, as has happened twice since 2000.

Asset allocation – step one: Inflict pain

Though I start by asking the client a few questions that you might see in a risk-profile questionnaire, I’m not trying to quantify the results. As odd as it sounds, I’m actually trying my best to inflict pain on the client as a reality check. For example, when I ask what they would do if their stocks lost 50% and they respond that they would buy more stocks, I point out that while it would be the correct answer, they should try to imagine that half of their financial freedom, the ability to do what they want for the rest of their lives, has vanished. Embracing those painfully excruciating feelings might change the answer.

Daniel Kahneman won the Nobel Prize for his work on this pain in what is called “prospect theory.” It essentially says we get twice as much pain from losing a dollar as pleasure from gaining a dollar. I asked Dr. Kahneman about this and he recommended discussing the pain with clients. Still, imagining pain and actually experiencing it are not the same.

Asset allocation – step two: Assess need

If a client has a low need to take risk, I typically recommend they don’t take unnecessary risk. There are always exceptions like clients who have enough money to build a conservative portfolio for their lives but a riskier one for future generations. But, in general, if their need to take risk is low, I try very hard to help them imagine the consequences of a prolonged down market for decades, such as has happened in Japan.

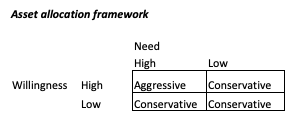

With steps one and two, I now have an imperfect understanding of the client’s willingness to take risk and a better understanding of their need. I then apply the simple framework below:

I will only recommend an aggressive allocation (more than 60% stocks) if the client has both a high need and willingness to take risk. That is to say, they must take risk in order to meet their goals and they are willing to do so. If a client has a high need but low willingness, I recommend a more conservative portfolio because the client is unlikely to stay the course and rebalance during a plunge. Thus, they will likely do better staying in a conservative portfolio rather than repeating the buy high and sell low that so many of us exhibit.

If, after talking through this, the client thinks they should be between 50% and 60% stocks, I’ll try to encourage the client to pick closer to the 50% recognizing that they will feel more pain in a bear than pleasure in a bull.

Asset allocation – step 3: Strike a deal if you have to

After more than a 10-year bull market, I sometimes have clients wanting to take on more risk than I think is prudent. Say, for example, I think the highest the client should go is 60% stocks but they want 70%.

My solution is to write into the plan that they will start with 60% but can increase it to 70% after stocks have declined by at least 20% from the date of the plan. I argue I’m not trying to time the market; I’m trying to test the client’s resolve to actually experience the pain (reality versus imagining) and react. As mentioned, we haven’t had a bear market in well over a decade but, even with a 10% correction, I’ve found most appetites for more aggressive allocations have fallen by the wayside.

Moving on to the most important portfolio decision

As mentioned in at the outset, I tell clients setting the asset allocation is only the second most important decision they will make. Committing to stick to the allocation for at least the next several years is the most important. I can’t predict financial markets, but predicting human behavior is much easier. Markets surge, we buy stocks only to sell after the plunge. As best said by behavioral economist Dan Ariely, we are predictably irrational.

I used to say, “If you can’t be right, at least be consistent.” I now think that consistency (the resolve to stick with the plan and rebalance) is even more important than setting it right in the first place.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

More Factor-Based Investing Topics >