Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“The process by which money is created is so simple that the mind is repelled.” – JK Galbraith

By formally announcing quantitative easing (QE) “infinity” on March 23, 2020, the Federal Reserve (Fed) is using its entire arsenal of monetary stimulus. Unlimited purchases of Treasury securities and mortgage-backed securities for an indefinite period is far more dramatic than anything they did in 2008. They also revived other financial-crisis programs like the Term Asset-Backed Securities Loan Facility (TALF) and created a new special purpose vehicle (SPV), allowing them to buy investment-grade corporate bonds and related ETFs.

The purpose of these unprecedented actions is to unfreeze the credit markets, stem financial market losses, and provide some ballast to the economy.

Most investors are unable to grasp why the Fed’s actions have been, thus far, ineffective. In this article, I explain why today is different from the past. The Fed’s current predicament is unique as they have never been totally faced with zero-bound interest rates heading into a crisis. Their remaining tools become more controversial and more limited with the Fed funds rate at zero. My objective is to assess when the monetary medicine might begin to work and share my thoughts about what is currently impeding it.

All money is lent in existence

That sentence may be the most crucial concept to understand if you are to make sense of the Fed’s actions and assess their effectiveness.

Under the traditional fractional reserve banking system run by the U.S. and most other countries, money is “created” via loans. Here is a simple example:

- John deposits a thousand dollars into his bank

- The bank is allowed to lend 90% of their deposits (keeping 10% in “reserves”)

- Anne borrows $900 from the same bank and buys a widget from Tommy

- Tommy then deposits $900 into his checking account at the same bank

- The bank then lends to someone who needs $810 and they spend that money, etc…

After Tommy’s deposit, there is still only $1,000 of reserves in the banking system, but the two depositors they have a total of $1,900 in their bank accounts. The bank’s accountants would confirm that. To make the bank’s accounting balance, Anne owes the bank $900. The money supply, in this case, is $1,900 despite the amount of real money only being $1,000.

That process continually feeds off the original $1,000 deposit with more loans and more deposits. Taken to its logical conclusion, it eventually creates $9,000 in “new” money through the process from the original $1,000 deposit.

To summarize, we have $1,000 in deposited funds, $10,000 in various bank accounts and $9,000 in new debt. While it may seem “repulsive” and risky, this system is the standard operating procedure for banks and a very effective and powerful tool for generating profits and supporting economic growth. However, if everyone wanted to take their money out at the same time, the bank would not have it to give. They only have the original $1,000 of reserves.

What the Fed does

Manipulating the money supply through QE and Fed funds targeting are the primary tools the Fed uses to conduct monetary policy. (As an aside, QE is arguably a controversial blend of monetary and fiscal policy.)

When the Fed provides banks with reserves, their intent is to increase the amount of debt and therefore the money supply. As such, more money should result in lower interest rates. Conversely, when they take away reserves, the money supply should decline and interest rates rise. The Fed does not set the Fed funds rate by decree, but rather by the aforementioned monetary actions to incentivize banks to increase or reduce the money supply.

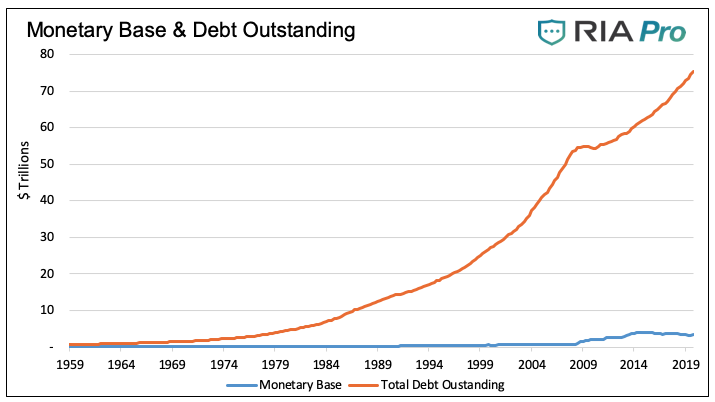

The following graph compares the amount of domestic debt outstanding versus the monetary base.

Data Courtesy: St. Louis Federal Reserve

Why is QE not working?

With an understanding of how money is created through fractional reserve banking and the role the Fed plays in manipulating the money supply, let’s explore why QE helped boost asset prices in the past but has not been similarly potent this time around.

In our simple banking example, if Anne defaults on her loan, the money supply would decline from $1,900 to $1,000. With a reduced money supply, interest rates would rise as the supply of money is more limited today than yesterday. In this isolated example, the Fed might purchase bonds and, in doing so, conjure reserves onto bank balance sheets through the magic of the digital printing press. Typically the banks would then create money and offset the amount of Anne’s default. The problem the Fed has today is that Anne is defaulting on some of her debt and, at the same time, John and Tommy need and want to withdraw some of their money.

The money supply is declining due to defaults and falling asset prices, and at the same time, there is a greater demand for cash. This is not just a domestic issue, but a global one, as the U.S. dollar is the world’s reserve currency.

For the Fed to effectively stimulate financial markets and the economy, they first have to replace the money which has been destroyed due to defaults and lower asset prices. Think of this as a hole the Fed is trying to fill. Until the hole is filled, the new money will not be effective in stimulating the broad economy, but instead will only help limit the erosion of the financial system and yes, it is a stealth form of bailout. Again, from our example, if the banks created new money, it would only replace Anne’s default and would not be stimulative.

During the latter part of QE 1, when mortgage defaults slowed, and for all of the QE 2 and QE 3 periods, the Fed was not “filling a hole.” Think of their actions as piling dirt on top of a filled hole.

Those monetary operations enabled banks to create more money, of which a good amount went towards speculative means and resulted in inflated financial asset prices. It certainly could have been lent toward productive endeavors, but banks have been conservative and much more heavily regulated since the crisis and prefer the liquid collateral supplied with market-oriented loans.

QE 4 (Treasury bills) and the new repo facilities introduced in the fall of 2019 also stimulated speculative investing, as the Fed once again piled up dirt on top of a filled hold. The situation changed drastically on February 19, 2020, as the virus started impacting supply chains, economic growth, and unemployment in the global economy. Now QE 4, Fed-sponsored repo, QE infinity, and a smorgasbord of other Fed programs are required measures to fill the hole.

But, there is one critical caveat to the situation.

As I stated earlier, the Fed conducts policy by incentivizing the banking system to alter the supply of money. If the banks are concerned with their financial situation or that of others, they will be reluctant to lend and therefore impede the Fed’s efforts. This is clearly occurring, making the hole progressively more challenging to fill. The same thing happened in 2008 as banks became increasingly suspect in terms of potential losses due to their exorbitant leverage. That problem was solved by changing the rules around how banks were required to report mark-to-market losses by the Federal Accounting Standards Board (FASB). Despite the multitude of monetary and fiscal policy stimulus failures over the previous 18 months, that simple re-writing of an accounting rule caused the market to turn on a dime in March 2009. The hole was suddenly over-filled by what amounted to an accounting gimmick.

Summary

Are Fed actions making headway on filling the hole, or is the hole growing faster than the Fed can shovel as a result of a tsunami of liquidity problems? A declining dollar and stability in the short-term credit markets are essential gauges to assess the Fed’s progress.

The Fed will eventually fill the hole, and if the past is repeated, they will heap a lot of extra dirt on top of the hole and leave it there for a long time. The problem with that excess dirt is the consequences of excessive monetary policy. Those same excesses that were created after the financial crisis led to an unstable financial situation with which we are now dealing.

While we must stay heavily focused on the here and now, we must also consider the future consequences of Fed actions. I will share more on this in upcoming articles.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.