Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Economic devastation will not heal itself in months or quarters and disappear, even if the virus does. The implications of bankruptcy and joblessness and a host of other financial, psychological, and societal issues dictate the path going forward.

On April 29, 2020, Fed Chairman Powell admitted this when he said, "both the depth and duration of the economic downturn are extraordinarily uncertain."

I am often critical of Federal Reserve policy and contradictory economic jargon coming from Fed presidents and governors. However, to my amazement, Powell surprised me with a moment of clarity.

No truer words have ever been spoken.

His statement is so obvious, it is profound. Yet, if you only follow the financial media or much of social media, you might think his statement hyperbolic. Apparently, the future, according to so many “experts,” is certain.

The economy will gradually re-open and, in time, everyone will go back to work and resume the same lives and consumption patterns they were leading in 2019.

This reassuring picture of economic resurgence and a return to normal is a matter of harnessing the virus. I too hope the confidence exuding from the experts being paraded around the clock on CNBC and Bloomberg turns out to be correct.

Think creatively

Wealth is not built, accumulated, or retained on hope. It is built on analytical rigor and a strong knowledge of data, facts, and history. It is built by avoiding debilitating losses, and by thinking for yourself.

History does not inform us of pandemics causing global economic shutdowns at times with extreme debt levels and eye-watering asset valuations. There is no relevant historical guidance for what may happen next.

However, we can evaluate various events throughout history, study their intricacies, and use them to arrive at a range of potential outcomes under current circumstances. What we learn by doing so, and what Powell reminds us, is that the future is far from certain.

Dare we say, extraordinarily uncertain?

Nth order effects

Monetary and fiscal stimulus will ease some of the pain, but at a cost. People have been scarred in ways that Wall Street and the media do not understand.

It is hard enough to forecast the first-order effects of the virus and its economic impact. Now consider the impossibility of understanding the myriad of second and third-order effects.

Anticipating these effects is like solving a Rubik’s Cube. If you twist a row to the left, what does that do to the other five sides? But that analogy is too simple. Make the cube an octagon and add 10 more rows and columns. Now add a series of rules, so each square is a chess piece and is limited in how it can be twisted.

To see a few shifts of the cube and think we can foretell the future is misleading at best and more akin to delusion.

Unforeseen effects

As I wrote this article, President Trump announced that the China Trade Deal is now secondary to what China did with the virus. Treasury Secretary Mnuchin followed that by warning that there would be “very significant consequences” if China does not make good on the trade agreement. The saber-rattling re-opens the following considerations:

- Trade war

- Tariffs

- De-globalization

We are witnessing a classic second-order effect, and but one example of what no one was planning for a few weeks ago.

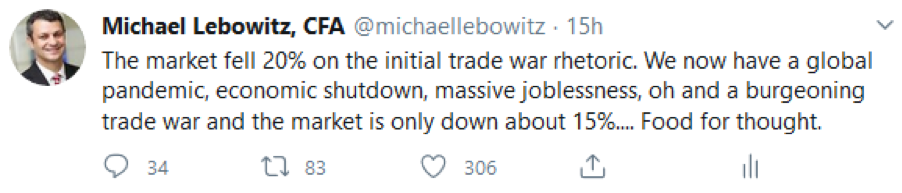

The previous trade war happened when the U.S. and global economy were healthy. Despite the economy, trade barbs between Chairman Xi and President Trump took the S&P down 20%.

The U.S. is engaged in a war on two fronts – one with another global power and one with a microscopic enemy. The list of possible second-order effects from these two issues is extremely complicated and unpredictable. Further, second-order effects often create third and fourth-order effects, and so on.

Buy and ignore

Stock prices and valuations are a function of the economy but are quite often trumped by confidence or lack thereof.

Despite depression-like GDP and unemployment data, which will undoubtedly be an anvil on corporate earnings, the S&P 500 has staged an eye-popping rally. April, in fact, witnessed the largest monthly percentage gain in over 30 years.

The S&P 500 is still down about 15% year-to-date, so some concern remains priced into asset prices.

However, despite the selloff, valuations remain near record levels and, in some cases, are even higher today than before the COVID crash. In other words, for all the uncertainty, the market has not corrected at all.

Investors are extremely confident that today’s problems will be fleeting and will not have significant lasting effects.

Summary

Extraordinary is defined as “very unusual or remarkable.”

Chairman Powell and the Fed, who tend to sugar-coat issues and take a cup-half-full approach, are warning us. What we are witnessing and experiencing is rare and without comparison.

No one knows how the future plays out geopolitically or economically, but we are experiencing a paradigm shift. Things have changed, and are changing, quickly. The “experts” are only experts at concocting compelling narratives. The ones who talk the most were cheerleaders during the dot-com bubble and never saw the onset of the great financial crisis. They are parrots repeating smart-sounding but empty phrases.

Many economists and investment strategists continue to use the lens of the past 10 year bull market in evaluating economies, markets, and investment ideas. They do not yet grasp that the next 10 years may not be recognizable from the last decade.

Do not assume that anyone, myself included, has the answers. Investment management is a dynamic process that should hinge first on sound risk management. As the Rubik cube turns and the chess pieces move, we learn more, allowing us to adjust and change our minds.

Today’s complexities will reward those who manage risk well.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.