Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

It would appear that nothing can pop the stock market bubble, but there is one straightforward “pin” that will do the job – rising interest rates.

Central banks around the world have embraced zero interest rate policy (ZIRP). As long as interest rates remain low, investors are forced to take the risk in stocks, discounted future stock earnings remain high, and debt service remains low. But central banks can’t control long rates, like the yield on 10-year government bonds.

That reality is here.

Recent increases in 10-year government bond yields are trivial relative to what they will become with the inflationary pressures from the trillions of COVID relief money being helicoptered into the economy. COVID failed to pop the bubble last March, but the worst is yet to come. COVID relief will bring serious inflation, increasing interest rates and bursting the stock and bond market bubbles.

In this article, I begin by proving that a stock market bubble exists despite Wall Street gaslighting to the contrary, and I provide 15 reasons that it exists. Then I provide 10 possible pins that could burst the bubble and argue that increasing interest rates is the most probable. Then I conclude with an estimate of when the bubble will burst and how bad it could be. I suggest a few ways that investors can protect themselves. I also provide this video for your viewing and listening pleasure.

A big blow has super inflated the bubble in the past 11 months

It’s official. The rebound from the March 2020 crash is a V-shaped recovery and it only took four months, which is much faster than the typical recovery that takes four years.

It gets even better.

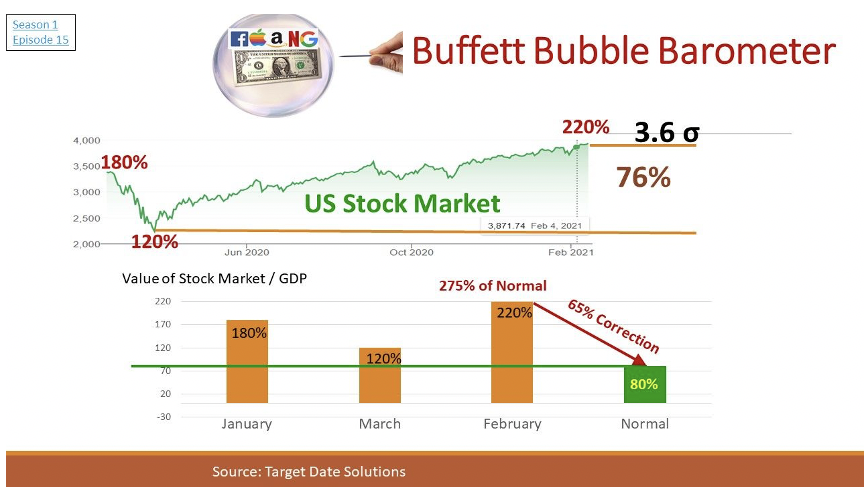

The return on the S&P 500 over the 11 months following the crash was an astonishing 76%! This is a 3.6 sigma event, very highly significant relative to the 9.6% average 11-month return.

This recent run-up brings the Buffett bubble barometer to its highest level ever at 220%, well above its 80% average. The value of the stock market is now 220% of gross domestic product (GDP).

The belief of many, including me, was that the March 2020 correction was just the beginning, and there was more to come. But now it will take a 45% correction to get the market back to those March levels, and it will take a 65% correction to get the Buffett barometer back to its 80% average.

The bubble just keeps inflating. But in case you still don’t believe there is a bubble, I discuss eight more indicators in the next section.

Eight more reasons to believe there’s a bubble

Wall Street is gaslighting us into believing that there is no bubble because they want investors to stay in the market. It’s true that most bubbles are confirmed after they pop, but this bubble is a whopper that baffles with its tenacity. A bubble exists when prices are far higher than fair value, like the price of some designer jeans today. To prove that there is a bubble, I need to establish a fair value and show that prices are way above it.

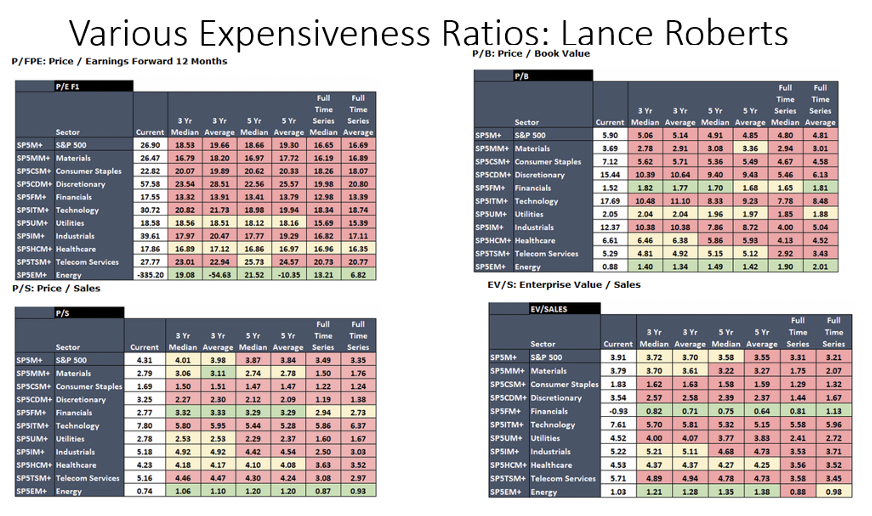

Price/earnings ratio (P/E) is among the most popular bubble metrics, with a “fair” historical average value of 15. It is currently above 30 and in the territory that has preceded previous market collapses. There are other ratios in bubble territory like those shown by Lance Roberts in the following, where red indicates the economic sectors that are overpriced.

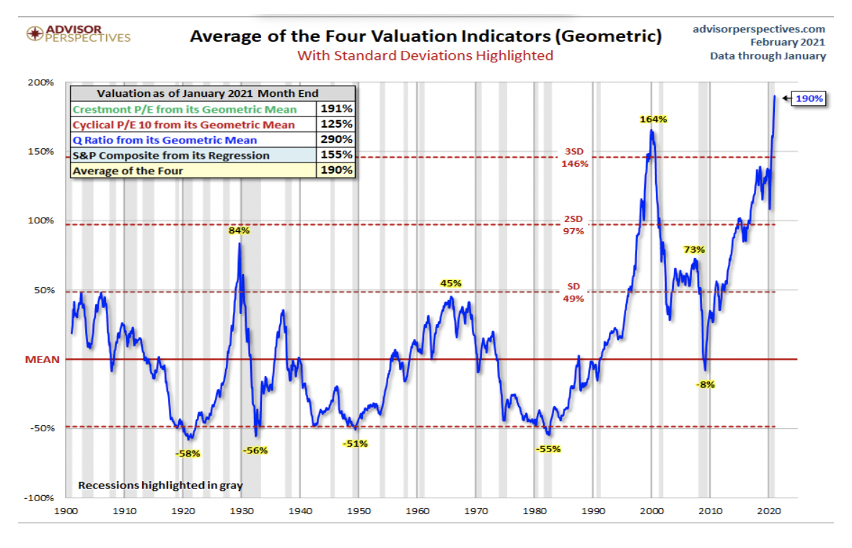

Similarly, the following picture is an example that uses a family of four expensiveness measures, from Advisor Perspectives:

There is also a bubble is in the bond market. Our government, as well as others, are implementing ZIRP, manipulating interest rates to artificially low levels in order to keep borrowing costs under control on our mounting debt. We have a debt crisis. As discussed below, this crisis is one of the pins that could burst the stock market bubble. The bond market bubble exists because our government wants it to exist. The reasons for the stock market bubble are more complex and varied.

15 explanations for the stock market bubble

I can think of 15 reasons for the current stock market bubble, most of which are wishful thinking. That article also lists 10 pins capable of bursting bubbles.

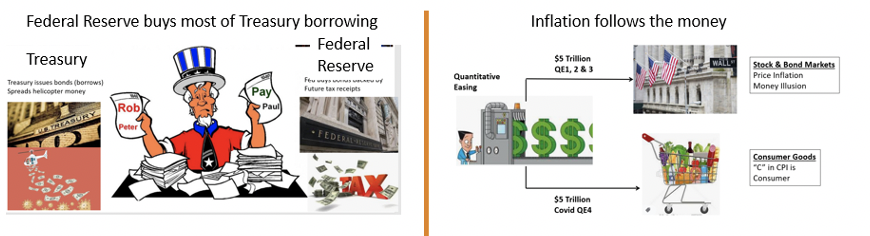

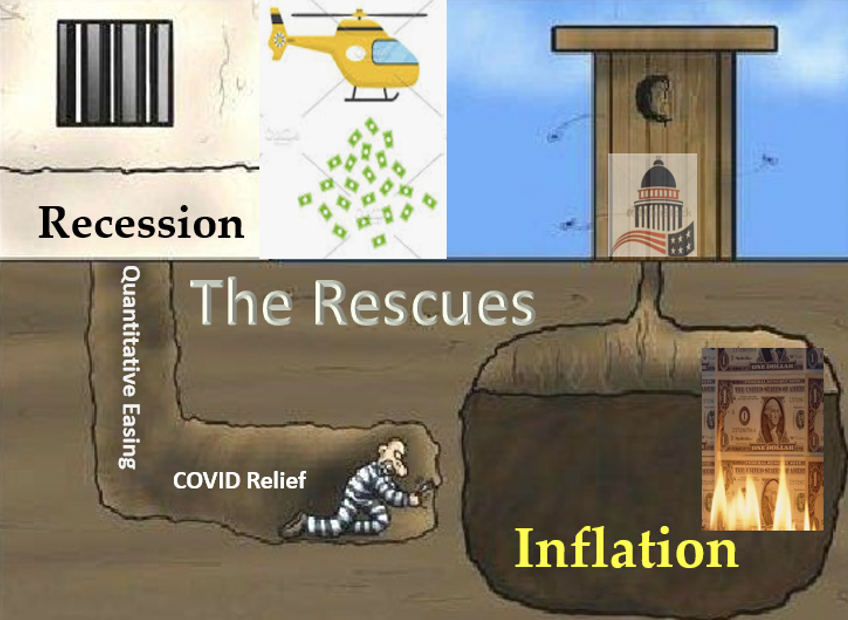

Money printing gone amuck

It all started in 2008 when the U.S. economic gears locked, and recession threatened. Quantitative easing (QE) came to the rescue. The US followed Japan’s lead and printed money to solve the problem, as recommended by modern monetary theory (MMT). MMT advises governments to print money if they own the printing press, but to guard against inflation by raising taxes as needed. The experiment worked, at least so far. Recession was avoided and the stock market enjoyed its longest recovery ever, although the Global Debt Crisis worsened. Even better, there was no inflation, at least as measured by the consumer price index (CPI).

The fact is that there has been inflation caused by QE, but not in consumer goods. QE money has mainly gone into the stock and bond markets, inflating the bubbles with money illusion. By contrast, the new money being printed for COVID relief will move the CPI needle because it will be spent on food and rent.

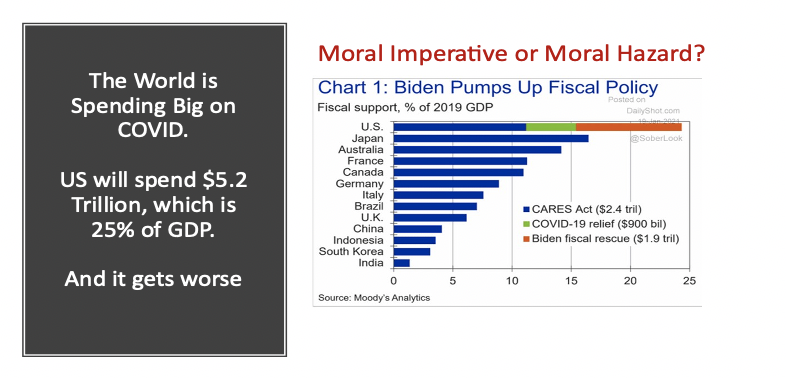

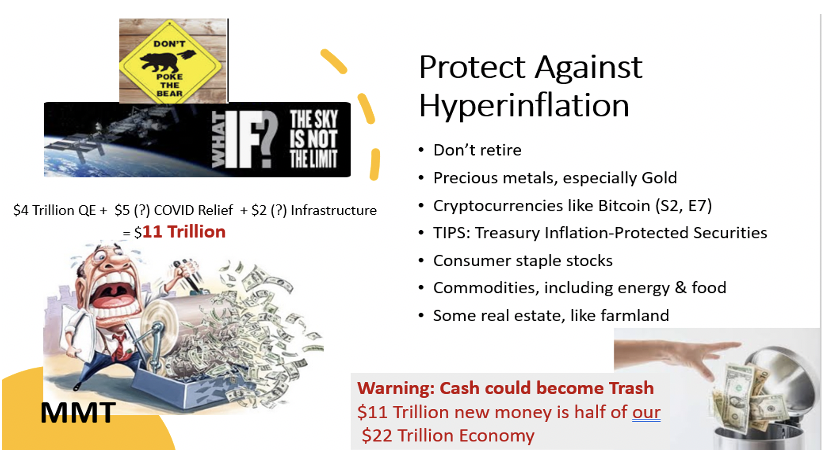

Another $5 trillion in COVID relief, in addition to $4 trillion in QE will load the U.S. economy with a mountain of paper money, plus another $2 trillion has been earmarked for infrastructure improvements. That $11 trillion is more than half of GDP.

The U.S. is outdoing all other countries in providing COVID relief.

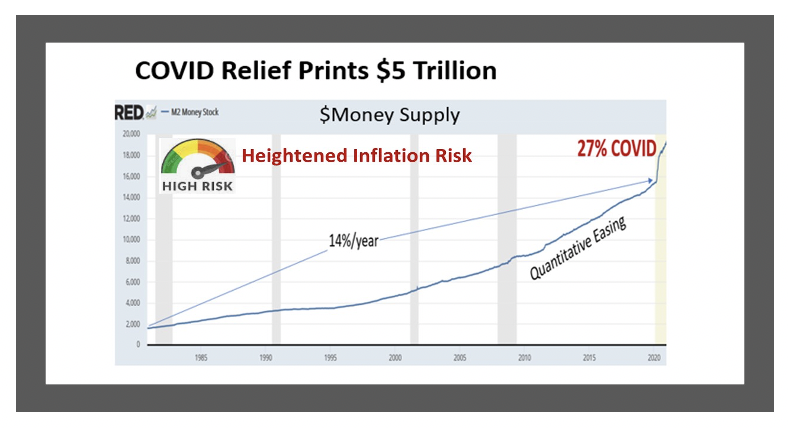

As a result, the U.S. money supply will increase by 27% overnight, as shown in the next picture.

Paper money is called “fiat currency” because it works by fiat – the government says it works and adds “In God We Trust” to its paper currency. But pieces of paper only work as long as we all agree and trust. The definition of money is that it is (1) a store of value and (2) a means of exchange. When currencies are devalued by excessive printing, they cease being a store of value. And in the case of extreme devaluation (hyperinflation), billionaires become penniless and paper money can’t be exchanged for anything.

Protect yourself

No one knows how much money the U.S. can print without creating rampant inflation, and no one wants to find out, but that is the path we are on. It’s a path that will be extremely painful and devastating to our baby boomers. Most of our 78 million baby boomers are now in the risk zone spanning the 10 years before and after retirement. There’s a high probability of a market crash during this period that will simultaneously an irreparably harm baby boomers due to sequence of return risk.

The number one investment objective of baby boomers at this stage in their lives should be to protect their lifetime savings. The first level of protection is to not invest in overpriced and risky stocks and bonds. The average investor, regardless of age, is 60/40 stocks/bonds, a mix that lost 35% in 2008 and that could lose much more when the current bubbles burst. This mix might be alright for younger investors who are likely to recover from a market crash, but recovery could take more than a decade, a decade that many boomers will not see. Ordinarily, cash would be a safe haven, but there is a risk of rampant inflation that argues for protection in precious metals and other real assets like cryptocurrencies and commodities, as shown in the following.

Conclusion

COVID relief will attack the U.S. stock market. Humanitarian relief comes with a moral hazard. Trillions of dollars in new money will cause inflation and drive interest rates up, which will tumble the whole façade built on ZIRP and MMT. QE dug the hole, but stayed clear of CPI inflation. But COVID relief turns the corner heading straight on into the inflation pit.

It would be surprising if inflation were controlled below 10% and the stock market declined less than 20%. Many, including me, believe the stock market will decline by at least 50% and inflation will be at least high double digits. Harry Dent forecasts a 40%+ market crash this April (pretty brave, right?).

Please see How to Minimize the Impact of Inflation, Recessions, and Stock Market Crashes for some thoughts on protecting yourself. Also, Peak Prosperity is a good source of economic analysis that says it like it is.

Ron Surz is CEO of Target Date Solutions, Age Sage, GlidePath Wealth Management, and co-host of the Baby Boomer Investing Show that you can binge watch on Patreon.

Please watch and support our Baby Boomer Investing Show on Patreon and visit our Baby Boomer Libraries, our Target Date Fund blog, and our GlidePath blog

Read more articles by Ron Surz