The Fed’s Naïve Mindset is Driving Societal Rift

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“It was assumed, even only a decade ago, that the Fed could not just print money with abandon. It was assumed that the government could not rack up huge debt without spurring inflation and crippling debt payment costs. Both of these concerns have been thrown out the window by large numbers of thinkers. We’ve seen years of high debt and loose monetary policy, but inflation has not come.

So the restraints have been cast aside.”

– David Brooks, New York Times, Joe Biden Is A Transformational President (my emphasis)

Regardless of whether you agree with Brooks’ politics, he makes an incredibly bold statement. Massive amounts of monetary and fiscal stimulus can be employed with no consequences or restraints.

This naïve mindset is not just Brooks’ but represents a rapidly growing school of thought among economists, politicians, and central bankers. They all want unicorn-like solutions to what ails us, but the truth, grounded in history, is no such thing exists.

Since Brooks shrugs off any consequences of aggressive monetary and fiscal policy, I bring them to the forefront.

Who Is funding the stimulus?

Someone must pay for rampant federal spending.

Ask your spouse, neighbor, or friend who that might be, and they are likely to tell you the taxpayer is on the hook. To some degree they are correct but increasingly less so.

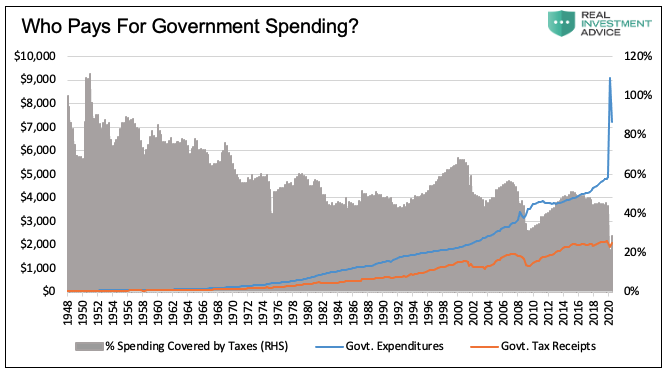

Since 1980 there have only been two years with federal surpluses. The government spent more than it received in tax receipts in 38 of the last 40 years. In other words, the government must borrow to supplement taxes to pay the bills.

Since 2017, taxpayers have paid for less than half of government expenditures. Over the last six months, as shown below, that percentage has fallen to less than a third.

Treasury bond investors are increasingly on the hook for the growing funding deficits. This scheme is possible because the Federal Reserve progressively employs easier monetary policy to assure interest rates stay abnormally low. The intention is not only to minimize the government’s interest expense but generate inflation. Inflation shrinks the real cost of the debt. An added benefit is to boost financial asset prices.

The government’s interest expense is less than 8% of its total expenditures. That is the lowest percentage since at least 1947. Contemplate the following:

- Total federal debt has risen 8320% since 1966.

- Federal debt-to-GDP is 127%, up from 40% in 1966.

- Interest expense declined by $46 billion as Treasury debt rose by over $7 trillion in the last year.

Manipulating interest rates to allow the proliferation of debt comes at a steep cost.

The consequence: Wealth inequality

Monetary policy has been a primary driver of wealth inequality. It employs low interest rates and spurs price inflation to drive temporary economic activity and goose asset prices.

The wealthy consume a relatively small percentage of their wealth. As such, inflation is not a big concern for them. On the other hand, low interest rates and rising asset prices benefit the large percentage of wealth they don’t spend. Per the Federal Reserve, the top 1% of Americans own 52.75% of corporate equities and mutual funds.

The poor frequently spend their entire paychecks and, at times, any sparse savings. Inflation, even when it’s low, reduces the purchasing power of their earnings. Other than small retirement-plan savings, in some cases, the poor receive little to no benefit from rising asset prices. But they pay for inflation.

I explained in detail the Fed’s role in widening the wealth gap in my article, Two Percent for the One Percent. The article’s summary started as follows:

The central banking scheme of supporting economic growth through increasing levels of debt only makes sense if “growth at all cost” uniformly benefits all citizens, but it does not. There is a big difference between growth and prosperity. Furthermore, an inflationary policy that aims to minimize the burden of debt while at the same time aggravating the growth of those burdens is taking a serious toll on global economic and social stability.

The consequence: Fear of dollars

As if rising wealth inequality and social rift are not a cost worthy of economists’ considerations, there is another problem with reckless monetary policy. People are increasingly looking for ways to protect their wealth. They are looking to divest from the dollar.

The day after Brooks’ editorial, the New York Times published the following: Investment Mania: From Crypto Art to Trading Cards.

Author Erin Griffith stated:

These seemingly singular events were all connected, part of a series of manias that have gripped the financial world. For months, professional and everyday investors have pushed up the prices of stocks and real estate. Now the frenzy has spilled over into the riskiest – and in some cases, wackiest – assets, including digital ephemera and media, cryptocurrencies, collectibles like trading cards and even sneakers.

She specifically mentioned a piece of digital art by Beeple, which sold as a non-fungible token (NFT) for $69.3 million:

With NFTs, the hysteria escalated quickly. Last month, an NFT GIF of Nyan Cat, which shows an animated flying cat with a Pop-Tart body, sold for roughly $580,000. Other artists, including Grimes and Steve Aoki, began reaping millions of dollars from their digital artwork. Then on Thursday, Beeple, whose real name is Mike Winkelmann, sold his “Everydays – The First 5000 Days” NFT for a stunning $69.3 million.

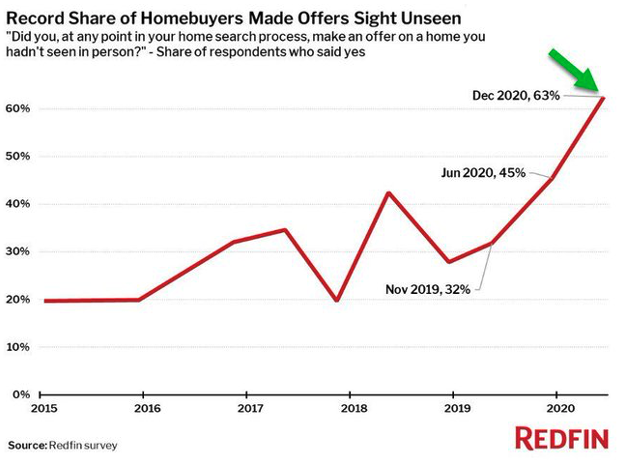

Her article highlighted the exorbitant prices being paid in fringe asset classes. It’s not just GIFs of flying cats and other “wacky” assets sucking in money; it’s hard assets like land and real-estate. The graph below shows the urgency of some home buyers. In December, over 60% of home buyers bid for a house without seeing it in person.

Fiat money, such as U.S. dollars, are worthless pieces of paper. Their value comes from individuals' trust in the ability for the dollar to retain value over time. Recent trends in digital assets, real estate, and other assets are clear signs that some people believe the dollar's value is eroding. They would rather own something else, anything else.

Summary

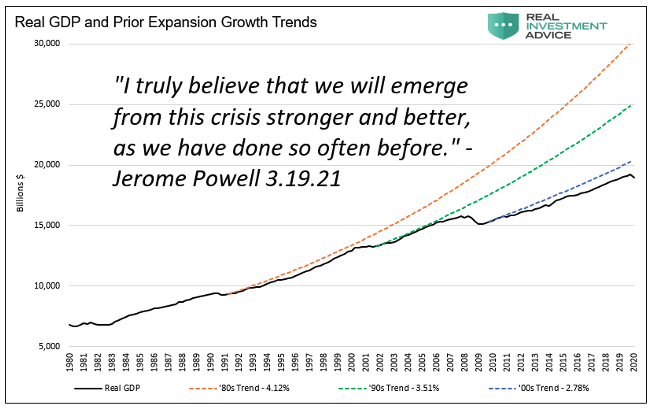

Thoughtless monetary policy is sold to the public in the name of the greater good. What these purveyors of deceit fail to identify is whose greater good. The graph below shares a recent quote from Jerome Powell in which he indirectly claims each successive economic recovery has been stronger than the prior one. He implies that monetary and fiscal actions to arrest recessions result in stronger future economic growth.

As shown in the graph, his statement is patently false.

Aggressive monetary policies funding immense fiscal spending will only widen the wealth gap and further slow economic growth, as it has done in the past. At the same time, said policies drive more people to seek shelter from the rapidly devaluing dollar. Speculative investments will further dominate, leaving less capital for productive investment. Productive investments build economic growth and help everyone prosper.

Ignoring history and logic may be expedient but it only aggravates our societal and economic problems.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All