The Eight Great Misconceptions About Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits I’ve spent more time explaining bonds to clients than stocks, mostly overcoming eight great misconceptions about fixed income. I’ve found most advisors share those misconceptions. Here is how I explain bonds and correct those misconceptions.

I’ve spent more time explaining bonds to clients than stocks, mostly overcoming eight great misconceptions about fixed income. I’ve found most advisors share those misconceptions. Here is how I explain bonds and correct those misconceptions.

What is a bond and why are they inversely correlated with interest rates?

Bonds are far simpler than stocks, alternatives, hedge funds, and derivative investments. A bond is a loan to either a corporation or a government and a bond fund is a collection of those loans. Say you lend a corporation $100 for 10 years at a 4% interest rate. You will receive $40 in interest and your $100 back. If, however, rates rise to 6%, you are getting $40 in interest while the market says $60 is the going rate. The value of the bond will decline. If rates fall to 2%, you are getting an extra $20 in interest over the market rate and the value of the bond will increase.

Far worse than interest rate risk is the chance of a default. If the issuer goes into bankruptcy, you will likely get no further interest and lose a good part of your principal.

Given that background, let’s look at the eight great misconceptions about bonds.

1. Rates have to go up – right?

Intermediate term rates have gone up this year. Rates on the 10-year Treasury bond have risen from 0.93% at the end of 2020 to 1.69% as of April 1, 2021. But, will rates increase further for the rest of the year? Before you say “yes,” understand the dismal track record of the top economists in predicting the direction of rates (up or down) which is far less than 50%– that’s worse than a coin flip. Advisors also get rates wrong.

To understand why we can’t predict intermediate or long-term rates, remember that the Federal Reserve auctions off Treasury bonds regularly. If most of the buyers knew that rates were going to go up, they would bid less for these bonds to get that higher rate. Thus, bond rates would have already gone up.

Another misconception is that intermediate and longer-term rates follow the Fed funds rate. The Fed controls the Fed funds rate but that is the shortest of short-term rates – merely overnight. Markets control longer-term rates.

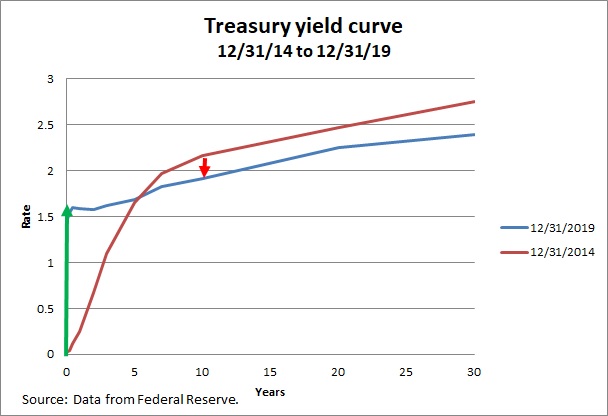

Beginning in 2014, the Fed did a double whammy. It stopped buying back bonds (the end of quantitative easing) and raised the Fed funds rate. Many financial planners cried “bond bubble” and predicted an increase in rates, causing bonds to plummet. The reverse happened. Intermediate and long-term rates declined, and bonds did quite well.

Just like in stocks, one must have knowledge the rest of the market doesn’t already have. Financial theorist and author William Bernstein once told me, “Trying to predict stock market returns is merely foolish; trying to predict interest rates is outright idiotic.”

2. Our huge debt and mushrooming deficits must result in high inflation leading to higher rates

Sure, the way I learned economics was that when you print more money chasing the same quantity of goods and services, that’s inflationary. And, of course, interest rates track inflation. But many things don’t follow what we learned in college. Japan has been running huge deficits for decades and its debt is now more than twice its GDP – almost twice that of the U.S. Since 1990, Japan has had virtually no inflation.

That’s not to say things will happen the same way in the U.S. Extrapolating based on one data point is always dangerous and I’m more than a little worried about our nation’s fiscal policies. Yet we can’t assume this means high or hyper-inflation will follow. It’s hard to predict rates; count me among the many who would have bet interest rates could never be negative as they still are in Germany.

3. Income from bonds is near an all-time low

Interest rates are very low, but get real. Consider taxes and inflation. The 10-year Treasury was yielding an average of 12.3% in the three-year period from 1979 to 1981. But tax rates were as high as 70% then, and even if only a third went to taxes, the after-tax yield averaged 8.2%. Unfortunately, inflation averaged 11.9%, so one lost about 3.7% of their spending power. Real rates – adjusted for inflation and taxes – were worse back then.

I tell clients that the purpose of fixed income has never been income. Rather, the purpose is to be the stable component of a portfolio and to have money to live on and to rebalance when stocks tank. Those high-quality bonds came in handy during the 33 days between February 19, 2020 and March 23, 2020 when stocks lost 35%.

4. Bonds are better than bond funds as they eliminate interest rate risk

Many advisors and individual investors think building a laddered bond portfolio eliminates interest rate risk. That’s because you know you are going to get your money back upon maturity, assuming no default. But, remember the example above when rates rose from 4% to 6% and one collected $20 less than the market rate on that $100 10-year bond? The net present value of that $20 loss shows up in the market value of that bond and holding it until maturity does nothing since the opportunity cost shows up in collecting that lower rate.

A bond fund like Vanguard Total Bond Market ETF (BND) is a laddered portfolio of 18,401 individual bonds. How could that be riskier than a laddered bond portfolio of a few dozen bonds? To the contrary, you get far more diversification, not to mention the ability to reinvest automatically. With the individual bonds, the client must leave the cash earning 0.01% until they have enough to buy another bond.

5. If interest rates do shoot up, the bond bubble prediction will come true

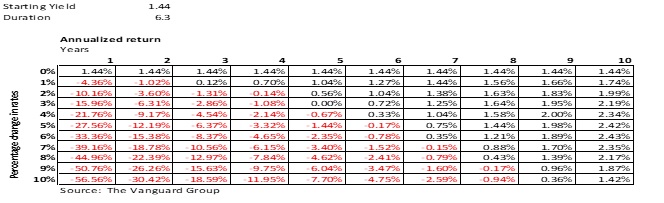

I’ve been hearing about a bond bubble for a long-time. Let’s frame what would happen to bonds if rates surged, as I’ve found it gives client’s some comfort. The illustration below is based on a fund like BND using a 6.3-year duration and a 1.44% starting yield. Taking a four-percentage point increase in rates over one year, this bond fund would lose an estimated 21.76% in one year. But that’s barely more than the stock market lost on black Monday in 1987. In fact, the stock market lost over 11% on March 16 of last year.

Back to the total bond fund example above; If rates then stabilized, the fund manager is now buying bonds yielding an average of four percentage points higher. By year six, the loss is wiped out and, by year eight, the gain is higher than it would be if rates had not risen in the first place.

6. Muni bonds are safe

Many think that munis have little risk, and that muni bond default rates were only about 0.5% during the Great Depression. I’m not against owning a low-cost muni bond fund but only in moderation. States and municipalities have about $4.5 trillion of unfunded pension and health care liabilities. That’s in spite of a surging stock market.

If stocks don’t do very well over the next decade, the shortfall will mushroom as baby boomers will have retired. As monthly benefits continue, there will be systemic risk to munis. This presents a different situation than what happened during the Depression or what Meredith Whitney said in her famously wrong call on CBS 60-minutes in 2010 – calling for hundreds of billions of dollars of defaults in the coming year. I’m worried about a long period of time and only if stocks don’t perform well.

7. Separately managed muni bond portfolios provide high income

I regularly look at portfolio statements showing tax-free income between three and five percent. This is a fallacy that the regulator, the MSRB, should deem illegal. The illusion works like this:

- Buy a bond with a $5 coupon for $112. Yield = 4.46% ($5/$112).

- Bond will mature or be called in three years at $100.

- Roughly $4 of that $5 yield is return of principal.

- Actual yield = 0.89% ($1/$112).

The bond manager is charging 0.4 to 0.5% to manage the bond portfolio; the actual return is roughly half that. By comparison, a bond fund is not allowed to report return of principal as income. As of April 1, 2021, the Vanguard Intermediate-Term Tax Exempt Bond Fund (VWIUX) yielded 0.93% after costs.

8. Interest from taxable bonds is always taxed as ordinary income

Though this is generally true, there are ways to turn future interest payments into long-term capital gains. Despite the recent uptick, interest rates have fallen and left many with unrealized gains. With interest payments higher than current yields, all things being equal, the prices of these bonds and bond funds will decline over time. Yet we will be taxed on those higher payments resulting in declining rates since we purchased them. If the client has a bond with a 5% unrealized long-term capital gain, they can sell it and buy a similar bond. This bond swap is typically done to harvest a loss, but can also convert future ordinary income into a long-term capital gain. If you tax-loss harvested in March 2020, your client may be able to absorb that gain in a tax-loss carryforward.

This can be done for a bond fund as well, but it’s more complex. You can’t just buy the bond fund back or buy a similar bond fund as the tax treatment is different for bond fund interest than the bond itself. You must buy an individual bond or tax-exempt bond fund. The latter has risk as previously discussed.

Conclusion

Bonds are the simplest but most misunderstood of the major asset classes. Many advisors harbor those costly misconceptions. Take risks with stocks and make your clients’ fixed income the most boring part of their portfolio with high-quality bonds. We can’t forecast rates. High-quality bond funds have as much risk in a year as stocks have in a day.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All