Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

"Neither bull nor bear"

A deflationary hurricane is churning off the coast. At the same time, a massive warm front is surging toward us, threatening inflation like we have not seen in 40 years. As if forecasting future economic conditions was not tricky enough, both systems are being fueled in unpredictable ways by the convergence of historical amounts of monetary and fiscal stimulus.

The two ominous and encroaching weather systems make economic and market forecasting extremely difficult. The most recent evidence came from last week's BLS employment report. The consensus of economic forecasters missed the mark by 734,000 jobs. That is over three times the average monthly job growth pre-pandemic.

Forecasters must also untangle global supply line problems and resulting shortages of many commodities and finished goods. Further, robust pent-up demand from the lifting of economic restrictions and a global pandemic significantly influences the economic climate.

Despite such extraordinary circumstances, the level of confidence in economic and market forecasts is remarkably high. Many "experts" forecast beautiful days with a temporary bout of above-average inflation. There is nary a mention of debilitating inflation and no recognition of the troubling deflationary hurricane off at sea.

The confidence and hubris backing forecasts should be of great concern, not comfort.

The butterfly effect

In 1963, Edward Lorenz, a meteorology professor from MIT, wrote a white paper called Deterministic Nonperiodic Flow. Years later, his theories became a core foundation of chaos theory.

Per the MIT Technology Review, the essence of his work is that "small changes can have large consequences." His logic is better known as the butterfly effect.

Lorenz suggested that the flap of a butterfly's wings might ultimately cause a tornado. And the butterfly effect, also known as "sensitive dependence on initial conditions," has a profound corollary: forecasting the future can be nearly impossible.

Yet Lorenz's own deterministic equations demonstrated how easily the dream of perfect knowledge founders in reality. That the tiny change in his simulation mattered so much showed, by extension, that the imprecision inherent in any human measurement could become magnified into wildly incorrect forecasts.

Misplaced confidence

How a simple flap of a butterfly wing can change the environment attests to the difficulty in predicting the weather. Meteorologists are quick to describe their limitations and relatively poor level of confidence around longer-range forecasts. They understand the impossibility of calculating millions of variable factors affecting the weather.

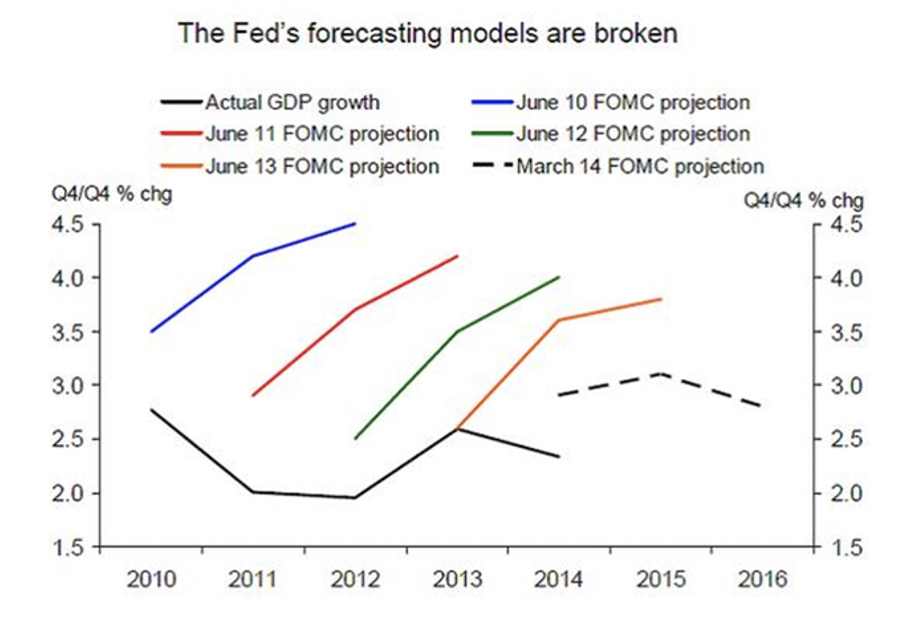

During more typical economic and market conditions, prognosticators struggle with forecasts. For example, the first graph below shows how the Fed consistently overestimated economic growth coming out of the last recession.

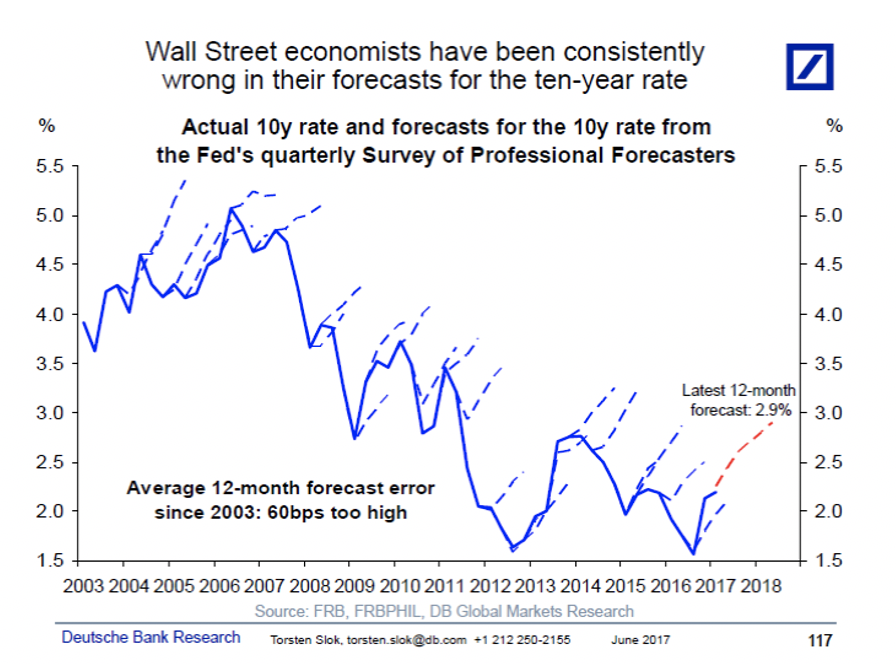

The following graph, courtesy of Deutsche Bank, highlights how Wall Street economists have consistently erred in their expectations for higher interest rates over the last 15 years.

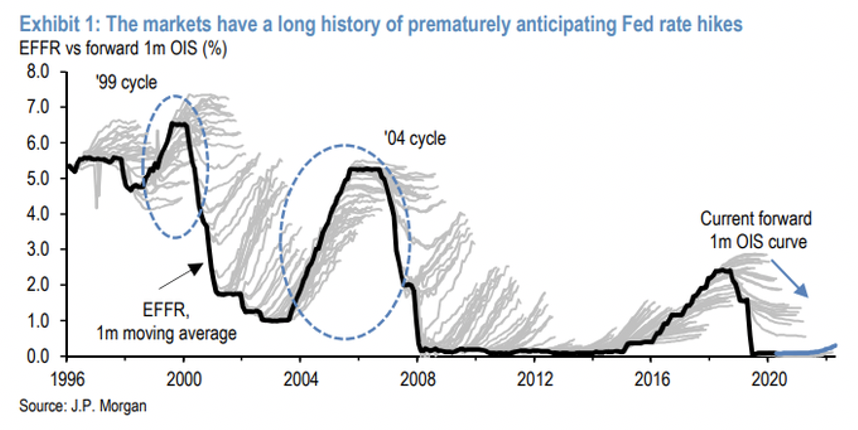

As the title of the next graph tells, markets have a long history of poor forecasts for the Fed funds rate.

Those at the Fed offer investors a good amount of confidence in predicting the pace of the economic recovery. They appear highly confident that any spurt of inflation will be transitory. If wrong, they offer complete confidence in their unproven tools to halt inflation. We know from historical experience that inflation it is difficult to arrest.

Wall Street analysts shrug off record equity and bond market valuations with forecasts of growth and normality. Investors buying at such valuations must trust that the Fed and Wall Street are correct. Despite the evidence that professional economic prognosticators are not good at their jobs, everyone seems assured of the future.

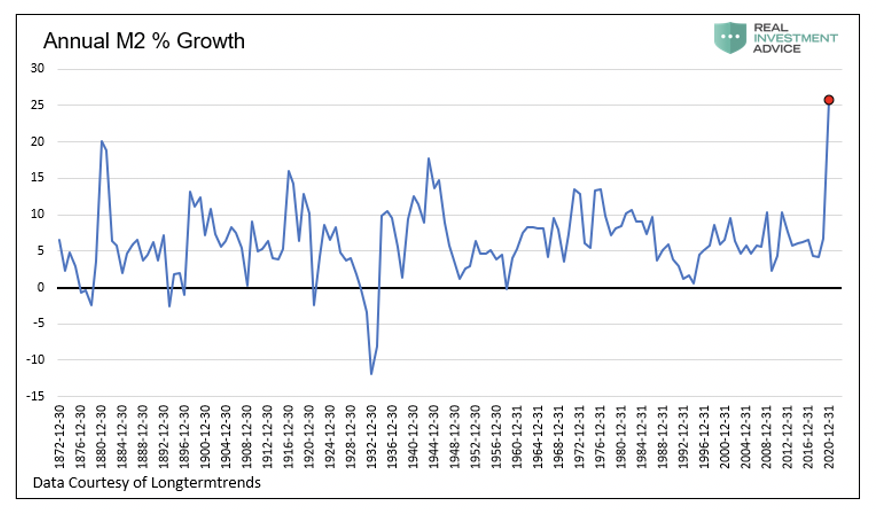

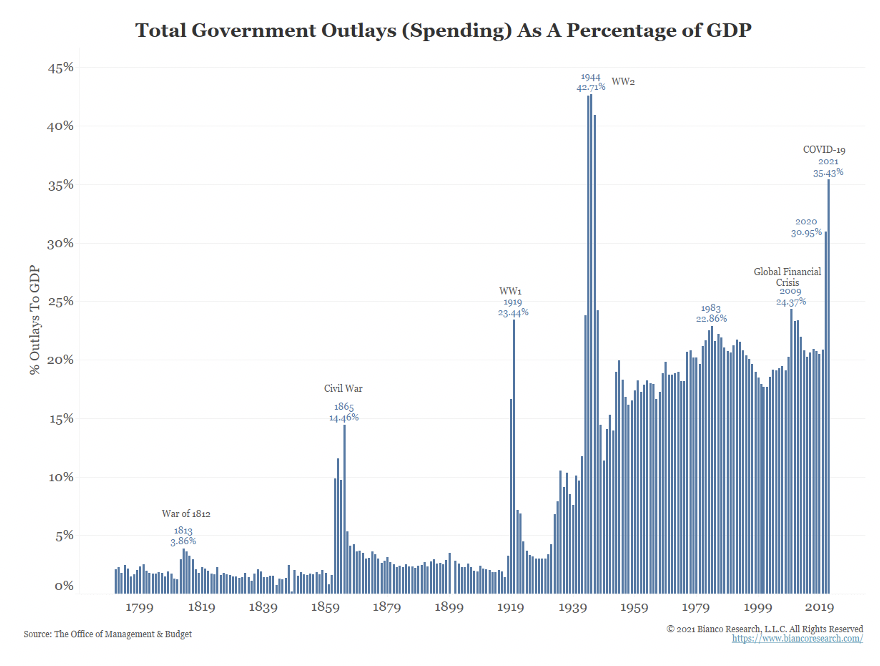

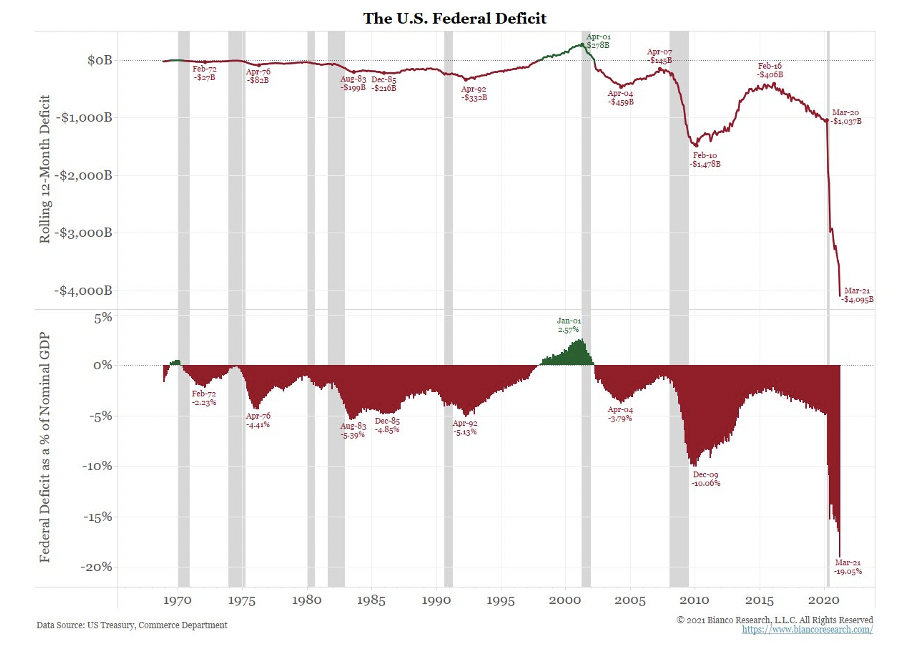

The graphs below show money supply growth, and the fiscal deficit are at levels that are anything but ordinary. Are we to believe the effects and consequences of such extreme monetary and fiscal policy, occurring concurrently, are easy to predict? Under such unique circumstances, what kind of professional would fail to recognize the peril of such a claim?

Confidence despite a poor track record

The cocksure attitudes of leadership, economic and political, and blind confidence put in them is perplexing given their poor track record. Consider a small sample of their dreadful forecasts:

- In June of 2017, Janet Yellen, Fed chair, stated: "Would I say there will never, ever be another financial crisis? ... Probably that would be going too far. But I do think we're much safer, and I hope that it will not be in our lifetimes, and I don't believe it will be." Less than three years later, GDP fell over 9% in a quarter, and the unemployment rate shot up from 3.5% to 14.8% in a month. The S&P 500 fell over 40% in four weeks.

- In May of 2007, a year before the subprime crisis would bankrupt many financial institutions and cripple others, Ben Bernanke stated: "we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system."

-

"I believe that the general growth in large [financial] institutions have occurred in the context of an underlying structure of markets in which many of the larger risks are dramatically – I should say, fully – hedged." Alan Greenspan 2000

- "We will not have any more crashes in our time." Famed economist John Maynard Keynes 1927

-

"There is no cause to worry. The high tide of prosperity will continue." - Andrew W. Mellon, Secretary of the Treasury. September 1929

Flip a coin

The point in highlighting blunders is not to shame the forecasters. Instead, it is to help readers understand that despite decades of experience, reams of data and information, and well sought-after educations, economists and market forecasters are human. They, like everyone else, have little ability to forecast the future accurately.

From an economic and market perspective, we are not in the lazy days of summer. Instead, we are in a highly charged, volatile environment. As a result, there are many unknowns, well beyond anything these brave forecasters ever witnessed or studied.

Their rosy forecasts may be correct. The economy might continue to recover gradually. The recent spike in inflation may be transitory, and economic data will assume prior trends. Unicorns may spew rainbows.

However, there are excellent odds they will once again be wrong. Lorenz stated: "small changes can have large effects." Now consider the potential range of effects from the plethora of economic and policy factors exerting significant influence over economic activity and human behaviors.

The reality is like meteorologists predicting next week's weather; no one knows what the economy holds in store. Of course, they can extrapolate current trends and make educated guesses on how consumers and corporations react to future events. Still, no one has ever experienced anything like what we face today.

Summary and advice

At my firm, RIA Advisors, we have a marketing tag line as follows:

Bulls win in Bull Markets; Bears win in Bear Markets. Eagles soar above and take advantage of opportunity. Let us help you soar as you reach your financial goals with R-I-A Advisors. Neither Bull nor Bear.

Given the economic climate and extreme market risks and rewards, we take an agnostic view of markets. We are not wed to opinions of economic activity or inflation and how they may steer markets. We are not self-proclaimed bulls or bears.

Paying top dollar for assets requires independent thinking and careful attention to market activity. To grow and preserve wealth in what may be a coming melt-up or meltdown, we must soar well above the nonsense and confidence spewed by so-called experts.

From the brightest traders on Wall Street to the halls of the Federal Reserve and the studios of the self-anointed media economic experts, there is zero appreciation for the potential of massive forecasting errors.

Quite often, investors are rewarded for going against the crowd, especially when the masses are in agreement on what the future holds.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

More Global Markets Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.