Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Inspiration for article ideas come from a wide variety of sources. This article's motivation is from "Compared to What," a classic jazz tune written in 1966. It was made famous in 1969 by Les McCann and Eddie Harris at the Montreux Jazz Festival and has been covered by over 200 artists. The song is a protest about Vietnam, crime, and economic and social inequality.

Fifty years later, there is no Vietnam war to protest, but social and economic inequality are again front-page news.

After casually listening to the song, one line in it, "Unreal values, Crass distortion," hit me over the head. The quote would have been perfect for several articles I have written to describe the economy and markets.

Alas, those words also accurately describe the Fed's role in redefining "capitalism," the topic of this article.

Don't blame capitalism

It has become popular to blame capitalism for today's economic inequality issues. I wholeheartedly disagree. The fault lies in Washington, D.C. for redefining capitalism.

Corporations own Capitol Hill and the Oval Office. Their ability to fund elections ultimately allows them to pick our leaders. Candidates unwilling to take corporate money have little chance of winning elections. Once a politician is bought, the laws are written to benefit mainly corporations.

The nation is stumbling into an odd mixture of corporate socialism as a result. Companies flourish to the detriment of the people.

Just as corporations increasingly define the government's fiscal role, the Federal Reserve increasingly dictates investment and speculative behaviors via monetary policy.

This article leaves political problems for another day and focuses on the Fed's machinations and their harmful effects.

Wicksell recap

The cost of money lies at the heart of free markets, and free markets are a core foundation of capitalism. The cost of money, or the level of interest rates, is a primary factor in helping savers and borrowers determine the best uses of money. When interest rates appropriately reflect the economic growth rate, capital gravitates toward its most productive uses. The more productive the economy, the more economic growth, and the better wealth is distributed to the entire population.

When the Fed interferes in the rates markets by setting interest rates and buying bonds, interest rates do not reflect the economy's actual supply and demand for money.

In my article, Wicksell's Elegant Model, I wrote:

Per Wicksell, optimal policy should aim at keeping the natural rate and the market rate as closely aligned as possible to prevent misallocation. But when short-term market rates are below the natural rate, intelligent investors respond appropriately. They borrow heavily at the low rate and buy existing assets with somewhat predictable returns and shorter time horizons. Financial assets skyrocket in value while long-term, cash-flow driven investments with riskier prospects languish.

Money flows to non-productive uses when rates are too low.

Bernanke wholeheartedly ggrees with Wicksell

If you think Wicksell's message is lost on the Fed, it's not. They choose to ignore it.

Consider the following quote from Ben Bernanke:

Paul Samuelson taught me in graduate school at MIT, if the real interest rate were expected to be negative indefinitely, almost any investment is profitable. For example, at a negative (or even zero) interest rate, it would pay to level the Rocky Mountains to save even the small amount of fuel expended by trains and cars that currently must climb steep grades.

Said differently, non-productive, or even poor investments, have increasing value as rates decline, especially as they fall below zero.

I have shown on numerous occasions how the real rate, or yield, on U.S. Treasury securities has been negative for the better part of the last decade. Over the last few months, the real rate for a wide assortment of risky loans turned negative. The incentive for corporations to level the Rocky Mountains has never been higher.

Fed-induced distortion on display

Over the last year and a half, the Fed has purchased nearly four trillion Treasury, mortgage, and corporate bonds. The reduction in the stock of investible bonds along with the Fed's zero-rate interest rate policy has further warped interest rates for all types of lending. As Wicksell postulates, lower-than-normal interest rates are driving a highly speculative environment. Productivity is languishing as a result.

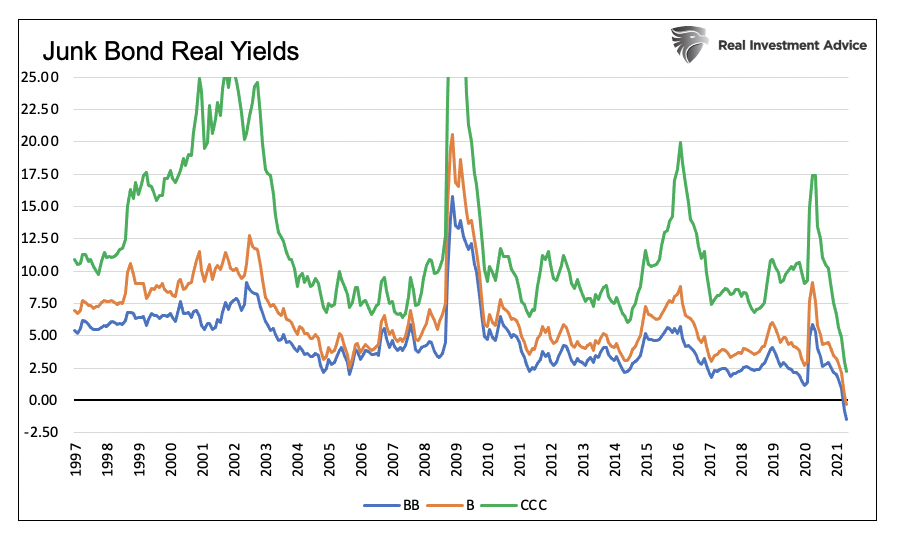

The graph below highlights how Fed policy distorts corporate bond yields. Corporate junk bonds offer investors a means to earn an above-average yield, albeit by taking on inflation and default risk. As shown below, yields on BB and B-rated junk bonds are now below the inflation rate, and CCC-rated bonds are not far from it.

Even if we assume zero defaults, which is impossible for an index of junk-rated bonds, investors will still lose money on an inflation-adjusted (real) basis.

Over the last 25 years, on average, junk bond investors were paid a premium over inflation of 4.7%, 6.5%, and 12.3% for holding B-, BB-, and C-rated bonds, respectively. Such yields offset inflation and the risk of default.

Interest rates are well below their natural rate.

Summary

Society is paying a dear price for policies that most citizens don’t understand. Forcing the price of money to absurdly low or even negative rates is slowly but constantly detracting from economic progress and ripping the social fabric of our nation. While there are many to blame, the Fed and their warped ideas around interest rates and economic growth should be among the first.

If only a famous musician today could stoke the public into action with a catchy song about the Fed's role in dismantling capitalism.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected]

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.