Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Because of its imprecision, The Fed chose the word "transitory" to describe rising prices. Transitory can mean hours, months, or decades. Using transitory versus a specific period provides the Fed freedom to be wrong but grammatically correct.

While the Fed uses ambiguous words, Mr. Market has more defined expectations. If investors grow impatient with the Fed's transitory, bond markets will react. In such a case, how will the Fed respond to "enduring" or "lasting" inflation coupled with higher yields? If they are already tapering, will such conditions push them to speed up their pace?

Conversely, recent data shows inflation may be stabilizing. Maybe the Fed is correct, and inflation rates will normalize in the coming months. If so, will they hold off on tapering or reduce the rate of tapering?

In July, I wrote Just How Transitory is Inflation? The article is a deep-dive analysis of the CPI. At the time, I sought a better understanding of what was causing inflation to rise. With two more months of inflationary data, an update is essential.

Understanding inflation beyond the headlines helps us answer the all-important question: How transitory is transitory? From there, we can assess potential Fed and market reactions.

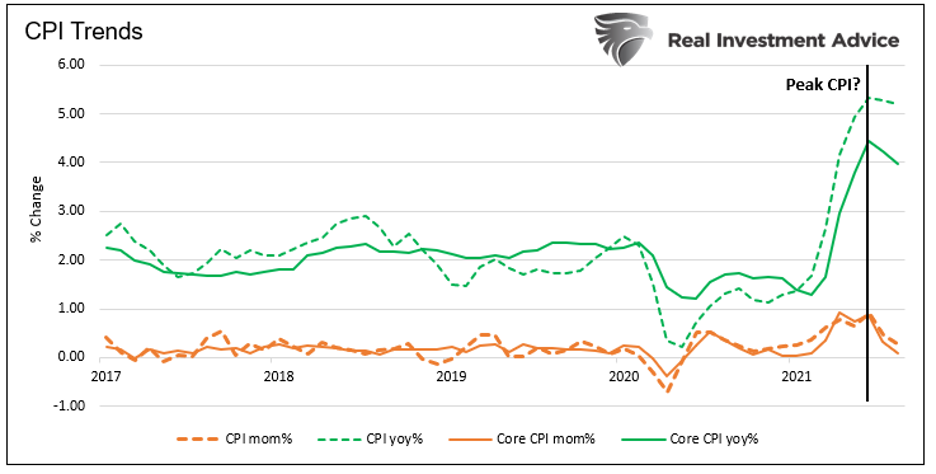

Headline CPI summary

In the latest CPI report, covering August, the monthly CPI figure rose by 0.3% or 3.6% annualized. The year-over-year rate is +5.30%. In comparison, June's monthly CPI rose by 0.90% or nearly 11% annualized. Despite the big difference in monthly rates, June's year-over-year change of +5.40% is only 0.10% higher than August.

As shown, the monthly CPI and core (excluding food and energy) are turning lower. While not as pronounced, the annual data is following suit. Two months does not make a trend, but it is fulfilling the transitory definition. Core CPI, at +0.10% last month, is 0.10% below the average for 2017-2019. Headline CPI is only 0.10% above the average.

The headline data is supportive of the transitory narrative; however, it does not tell the whole story.

The breadth of CPI

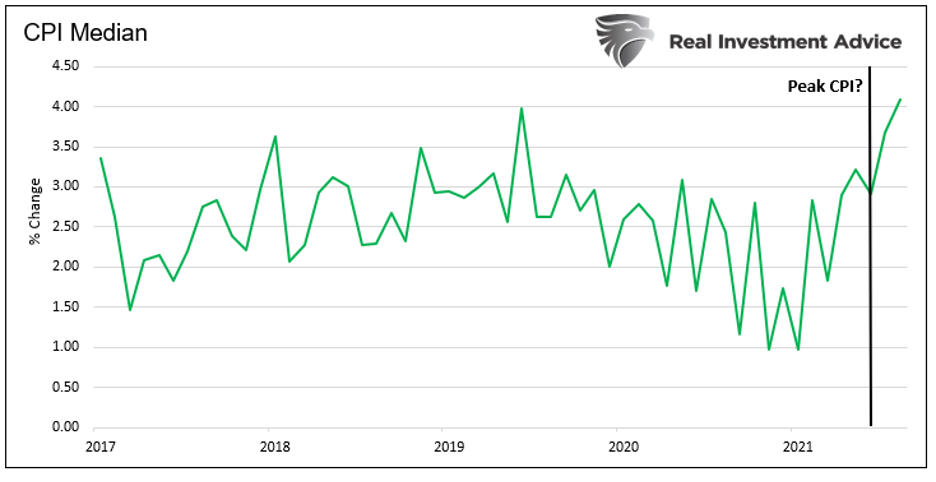

Digging deeper into CPI and looking beyond the headline averages shows inflation is not transitory. The graph below shows the CPI Index based on the median price of the goods and services in the index. Unlike the headline CPI Index, the median CPI is still rising and at the highest level since 2008.

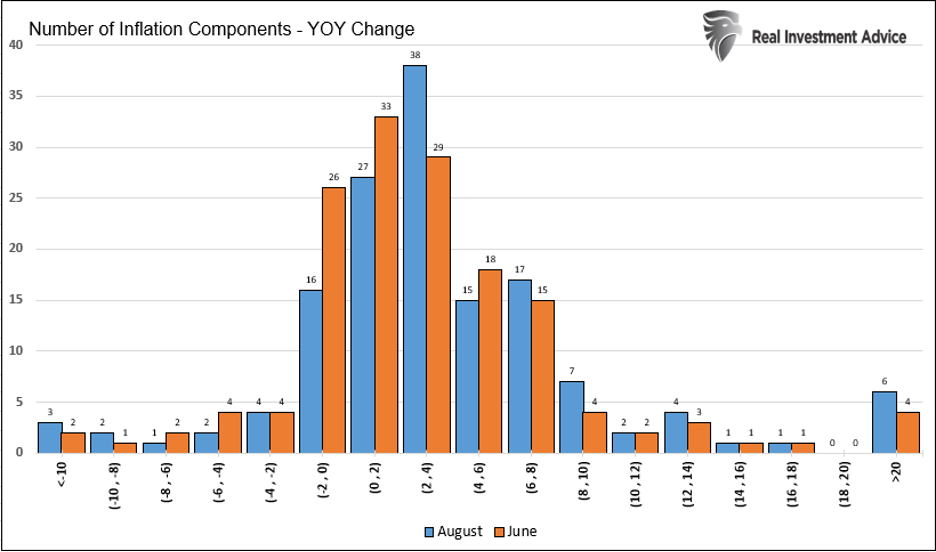

The distribution graph below compares June to August and shows how the prices of all the underlying goods and services within CPI are changing on an annual basis. I separate the data into 2% price buckets.

The blue (August) and orange (June) bars comparing the two months may look somewhat similar, but there are differences important.

In June, 75% of the CPI components were rising at a rate slower than the 5.4% inflation rate. In August, 71% were rising at a slower rate than the 5.3% rate of inflation.

The number of goods whose prices rose between 2% and 10% increased from 66 to 77. The number of goods whose prices rose by 2% or less fell from 72 to 55. While not obvious in the graph, the number of goods shifting to the right (more inflation) is noteworthy.

Among goods and services, 52 have had price declines from June to August. Six were unchanged, and 95 had price increases. Again, more goods are rising in price than falling.

The breadth of the market is not supportive of the transitory theme. A wide swath of prices are broadly rising, albeit not at an alarming pace.

Outliers

In the original article, four goods had year-over-year price changes of greater than 20%, as shown below:

- Used Cars 45.2%

- Gasoline 45.1%

- Fuel Oil 44.5%

- Other Motor Fuels 32.1%

In the August report, six goods had greater than 20% increases. The four goods from June maintain annual 20% rates of inflation. Added to the list are propane and utility services.

The inflationary outliers continue to be energy and auto-based. Both are rising in large part due to the reopening of the economy and supply disruptions. We expect both will moderate in the coming months. As this occurs, they will put less upward pressure on the CPI index.

Employee and school cafeteria food prices are down well below 20%. Over time, these should moderate as schools and offices come online. That will result in inflationary pressures.

Big contributors

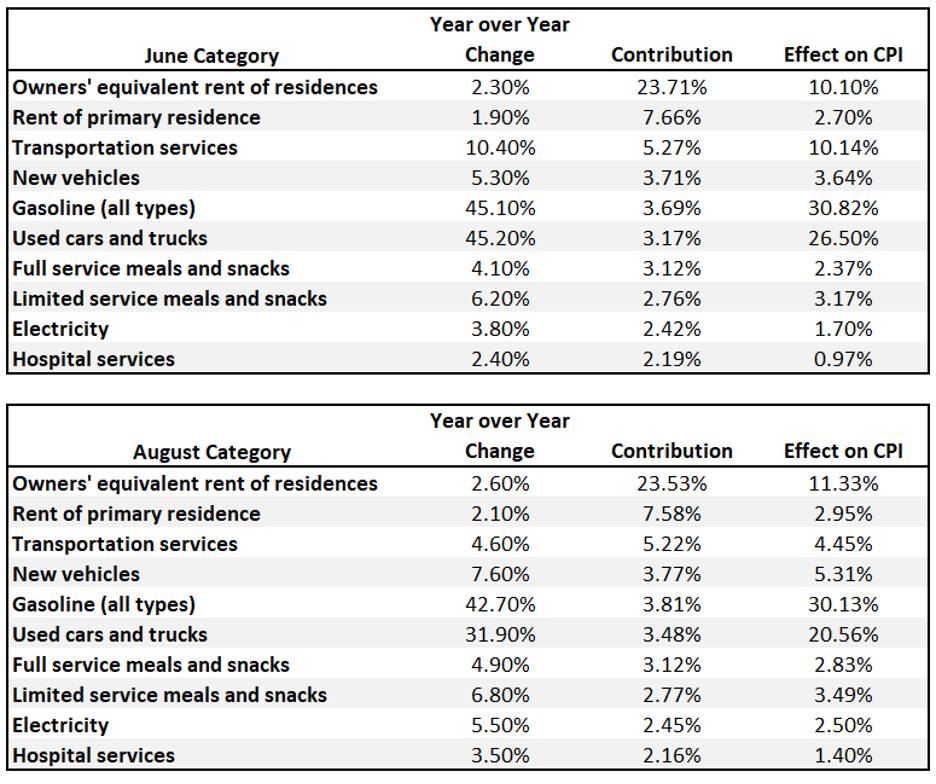

In June, 92% of the change in the CPI was due to the price changes of the 10 largest index weightings, as shown below. Those 10 goods played slightly less of a role in August, contributing 82% to the change in the index. Below is a comparison of the same ten contributors for June versus August.

The prices of used cars and transportations rose at a slower rate than June, but every other category was little changed.

In the original article, I warned that shelter prices are the most considerable risk to more inflation. Driving my concern is shelter's 30%+ contribution to CPI and rapidly rising home and rent prices. As I show above, higher home and rental prices are barely making their way into CPI.

What gives?

In my article, BLS' Housing Inflation Measure is Hypothetical Bull****, I stated: "It appears impossible to calculate the BLS version of OER or rent."

I remain concerned that a double-digit increase in rent and home prices (OER) will push shelter prices higher in the months ahead. However, history proves reality and the BLS Shelter measure have a near-zero correlation.

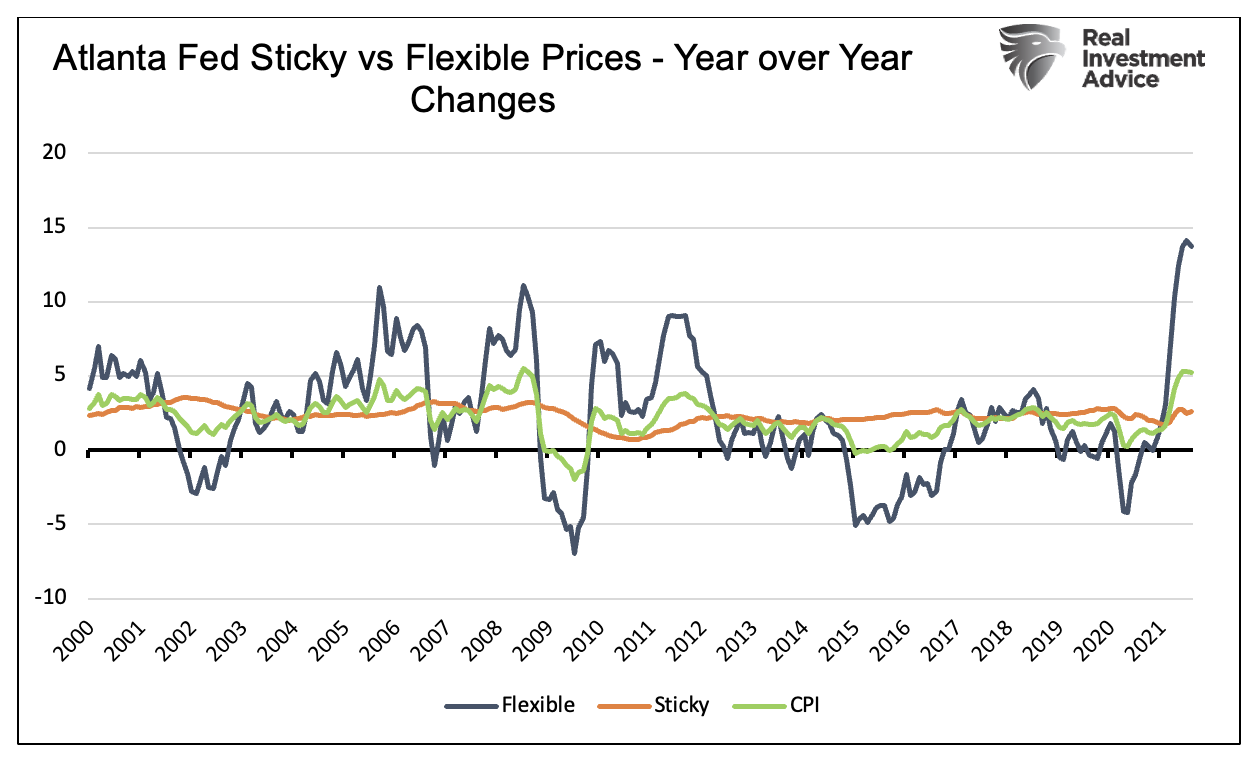

Flexible prices

As I wrote in June, CPI tends to be heavily correlated with goods and services that have flexible prices. These are goods like gasoline, whose prices tend to fluctuate both up and down. The Atlanta Fed publishes data on flexible and sticky prices, as shown below.

The graph shows sharp increases in both flexible- and sticky-priced goods are leveling off over the last two months. Given the Atlanta Fed measure of flexible prices has a 96% correlation with CPI, I am hopeful the upsurge is halting.

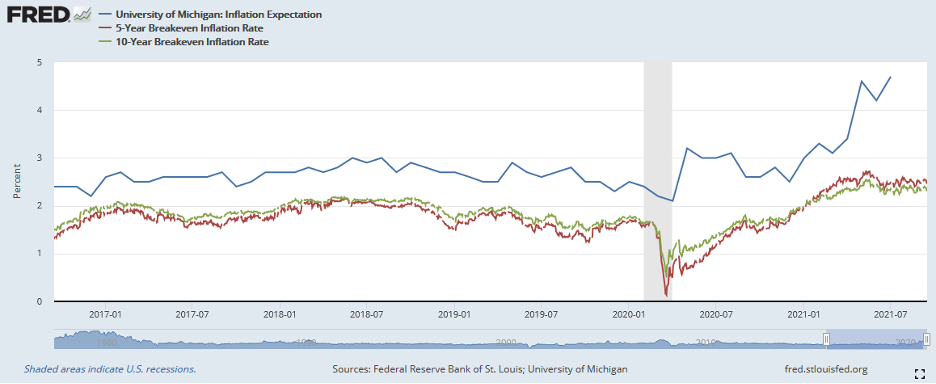

Expectations

The graph below shows a glaring divergence between Wall Street inflation expectations and those of Mom and Pop. Five and 10-year market-implied inflation expectations have been stable since January. All the while, the University of Michigan survey of consumers sees steadily rising inflation expectations.

While Wall Street buys into the transitory theme, consumers are not. This divergence matters as personal consumption drives about two-thirds of economic activity.

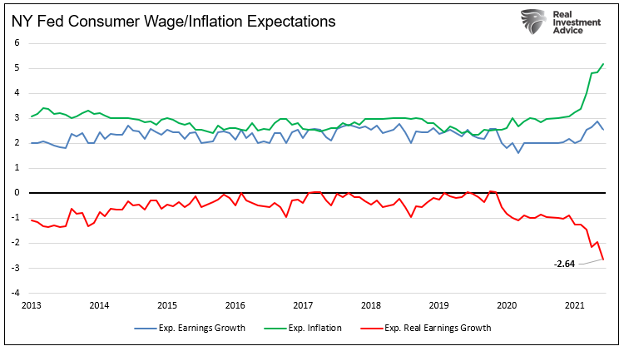

The New York Fed, via its latest consumer expectations survey, highlights why confidence is weak. Per its survey, expected inflation is now over 5% and rising. At the same time, expected wage growth is 2.5% and stable/falling. As a result, consumers expect to lose 2.64% (red line) in purchasing power over the next year. Would you be confident taking a 2.64% pay cut?

Summary

We are witnessing unprecedented pressures on the supply and demand side of pricing equations. Forecasting, with such uncertainty, is challenging. As such, I maintain a humble approach to inflation forecasting.

The latest round of data provides some evidence inflationary pressures are abating. However, the breadth of the data tells us there are still many goods and services still rising in price. This difference may help explain why consumer inflation expectations are higher than the market's, and confidence is falling.

Just how transitory is transitory? The market will have its answer in the next few months. Prolonged rising or high inflation beyond December will get many to question if inflation is truly transitory. Until then, pay attention to headline inflation, the breadth of the data, and especially any effects from rising shelter prices on CPI.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected]

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.