Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

"Currently, the December 2019 Fed Funds futures contract implies that the Fed will reduce the Fed Funds rate by nearly 75 basis points (0.75%) by the end of the year. While 75 basis points may seem aggressive, if the Fed does embark on a rate-cutting policy and history proves reliable, we should prepare ourselves for much more."- Investors Are Grossly Underestimating the Fed

My advice to plan for the unexpected was prescient. When I wrote the article in July 2019, Fed funds were between 2.25% and 2.50%. The Fed funds futures contracts were implying the Fed would reduce rates by .75% in the forthcoming months.

By April 2020, Fed funds were trading near zero, 1.50% below where the market thought they would be in mid-2019. The article quantified the history showing that the Fed always raises or cuts rates much more than expected.

Today, the market is pricing in steady increases for the Fed funds rate, starting in 2022. Yet, despite high inflation and low unemployment, the Fed refuses to think about thinking about raising rates.

Given the Fed's posture, traders are overestimating how much the Fed will raise rates. However, I caution once again; traders always underestimate the Fed.

Evidence

Whether higher Fed funds is logical is irrelevant. As investors, we need to strategize in case history proves clairvoyant. Given the Fed is starting to normalize monetary policy, it's worth revisiting the above referenced article from 2019.

I recommend reading the article's first section for more background on Fed funds and their futures contracts.

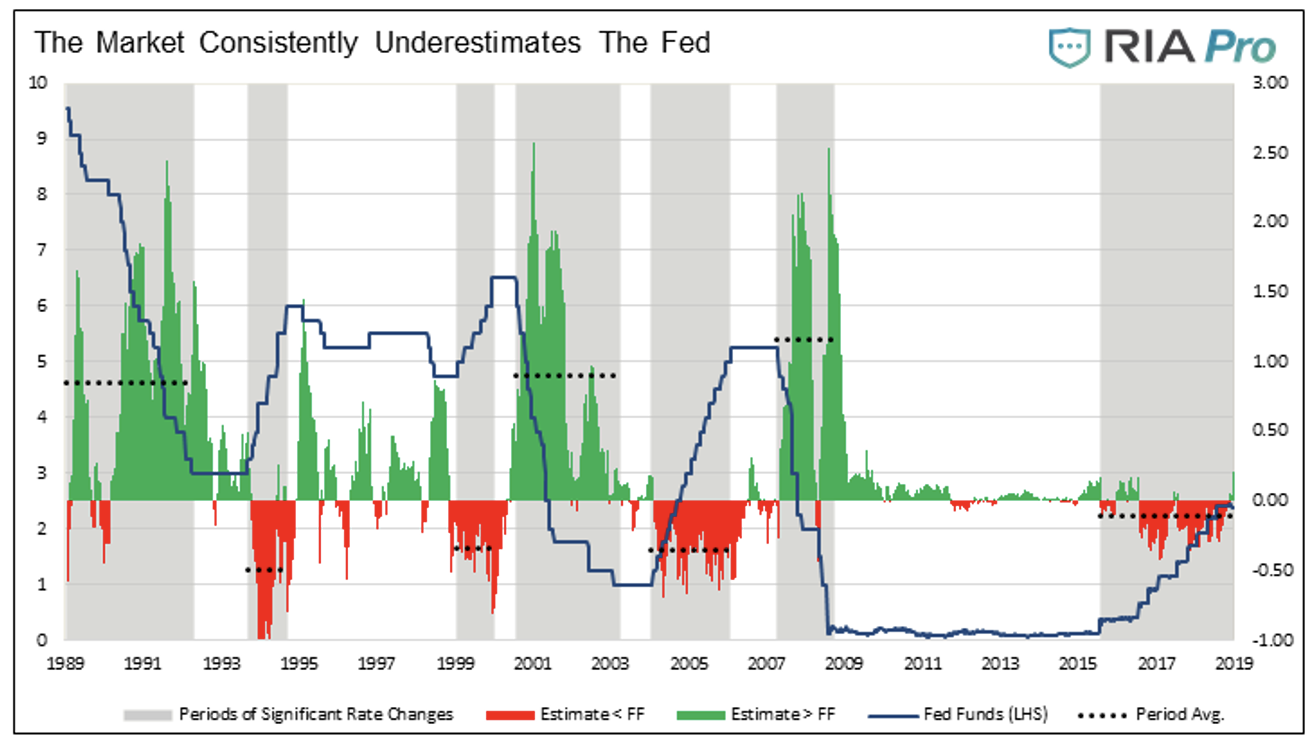

The graph below shows how much the Fed funds futures market consistently over or underestimates what the Fed does. The green areas and dotted lines quantify how much the market underestimates how much the Fed ultimately reduces rates. The red shaded areas and dotted lines are akin to today's potential rising rate situation. They show estimates for rate cuts fall short of the Fed's actual actions.

Per the article:

As shown in the graphs above, the market has underestimated the Fed's intent to raise and lower rates every single time they changed the course of monetary policy meaningfully. The dotted lines highlight that the market has underestimated rate cuts by 1% on average, but at times during the last three rate-cutting cycles, market expectations were short by over 2%. The market has underestimated rate increases by about 35 basis points on average.

The good news, with rate increases on the horizon, is the market's margin of error for rate increases is much less than for rate decreases.

Current expectations

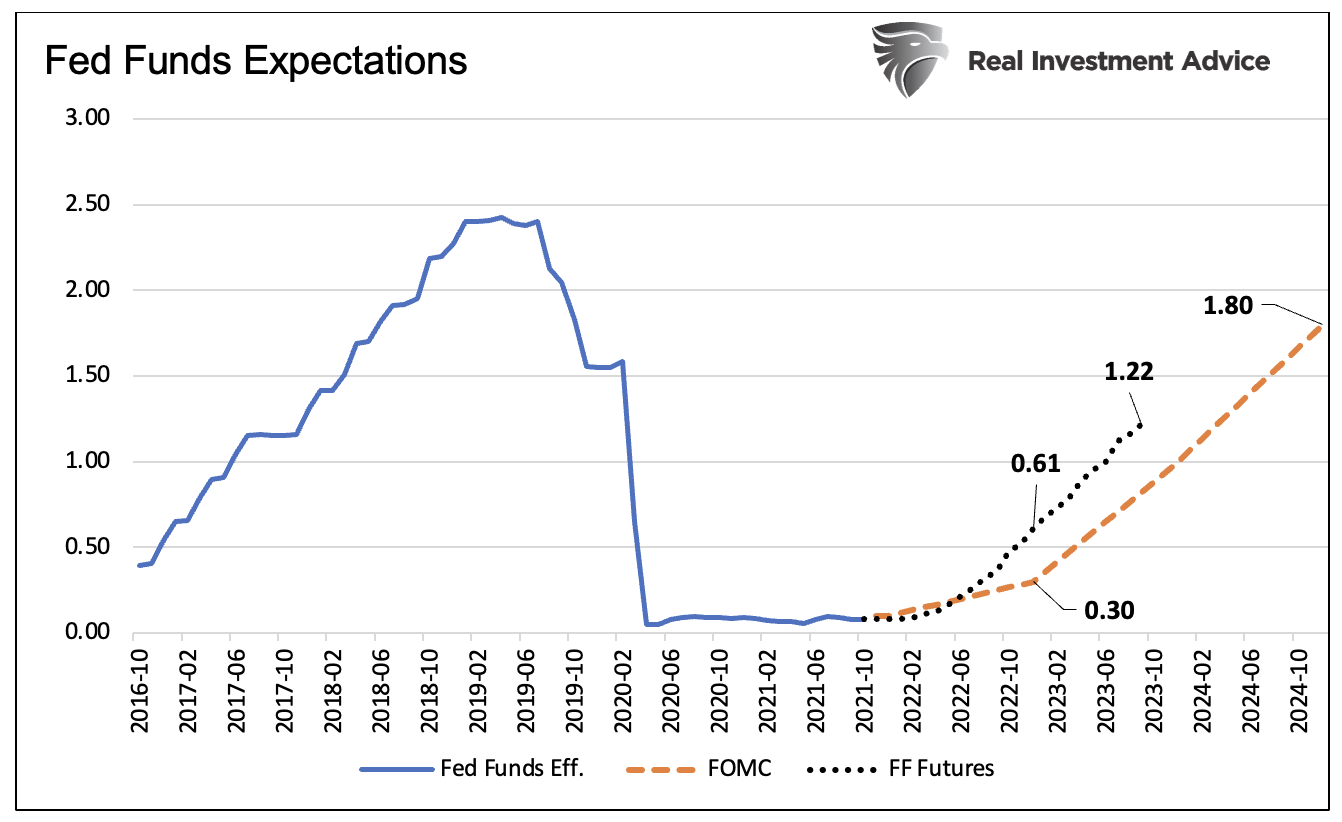

The Fed funds futures markets are now pricing in a 100% chance of a 25 basis point rate hike by August 2022 and a second hike by year end. They also project two more hikes in 2023.

The graph below highlights the history of Fed funds as well as the futures implied forecast. I also show the Federal Reserve's median forecast.

The Fed is coy about tapering QE, let alone raising interest rates. While the forecasts shown above may seem aggressive, odds are they are conservative. Based on the last four significant rate-hiking experiences, we should expect an additional 35 basis points, above market expectations, of rate increases by the end of December 2022. 1% Fed funds here we come!

Why the market may be underestimating the Fed

The current environment is unique, making my quantitative forecast questionable. The unique ways in which the pandemic crippled economic activity along with the massive amounts of fiscal and monetary stimulus are beyond compare.

Inflation at 5.4% is running more than twice the rate of the prior 10 years. Of more significant concern, it is showing signs it may be persistent. Chairman Powell recently noted as much: "The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation."

The Fed has not faced such an inflationary environment since the late 1970s and early 1980s. Fractured supply lines, shortages, transportation problems, and rising wages threaten to keep upward pressure on prices. If elevated prices remain persistent, the Fed will need to act with aggression to reduce it.

If such a scenario plays out, the market may be grossly underestimating the Fed's resolve and political pressure on them to quell inflation.

Why the market may be overestimating the Fed

Economic growth is slowing rapidly. Third-quarter GDP was just 2%, well off the 6.7% pace of the second quarter. Forecasts for the fourth quarter range widely from 3% to 6%. However, estimates for the third quarter were also north of 5% only a month ago.

If some of the supply problems abate and economic activity remains weak, the Fed could slow its taper schedule and leave Fed funds alone. One could argue it might taper QE only to increase monthly purchase amounts in the first quarter of 2022. In this case, Fed funds would stay near zero.

Summary

As I wrote in Investors Are Grossly Underestimating the Fed, "the market has a long history of grossly underestimating, in both directions, what the Fed will do. The implications to stocks and bonds can be meaningful. To the extent one is inclined and so moved to exercise prudence, now seems to be a unique opportunity to have a plan and take action when necessary."

Two years after having written those words, they remain equally important today. The equity markets and most financial assets, for that matter, are trading at extreme valuations. It is not future economic prospects driving the enthusiasm. Instead, it is the Fed's radical monetary policy. In What is the Federal Reserve Hiding From Us? I offered investors caution: "The most inappropriate monetary policy" is the sole bedrock supporting the most egregious asset valuations in well over 100 years."

If easy money is the bedrock of valuations and the Fed is getting ready to shift the bedrock, investors best pay attention to market forecasts and how the Fed ultimately acts.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Fed is coy about tapering QE, let alone raising interest rates. While the forecasts shown above may seem aggressive, odds are they are conservative. Based on the last four significant rate-hiking experiences, we should expect an additional 35 basis points, above market expectations, of rate increases by the end of December 2022. 1% Fed funds here we come!

The Fed is coy about tapering QE, let alone raising interest rates. While the forecasts shown above may seem aggressive, odds are they are conservative. Based on the last four significant rate-hiking experiences, we should expect an additional 35 basis points, above market expectations, of rate increases by the end of December 2022. 1% Fed funds here we come!