Why the Fed Isn’t Tightening

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

On November 3, 2021, Jerome Powell made it clear the Fed will not raise interest rates until the labor market improves further:

We don’t think it’s time yet to raise interest rates. There is still ground to cover to reach maximum employment, both in terms of employment and in terms of participation.

While his concern for the labor situation seems legitimate, he might have an ulterior motive for not raising rates.

The motive lies in the following statement: “The Fed’s policy actions have been guided by our mandate to promote maximum employment and stable prices for the American people along with our responsibilities to promote the stability of the financial system.”

As I show in this article, the economy is pretty much at maximum employment. Inflation is running red hot and increasingly showing signs it is persistent. Having neglected one mandate and largely fulfilled the other, why is the Fed so slow to reduce asset purchases and unwilling to contemplate hiking interest rates?

Before I answer the question, I share data on the two congressionally chartered Fed mandates: price stability, and maximum employment. Examining the data shows there is something else accounting for recent Fed’s policy actions, or better said, lack of action.

Price stability

"The risk is skewed now, and it appears to be skewed toward higher inflation.”

“Overall inflation is running well above our 2% longer run goal.”

Powell was crystal clear at his November 3, 2021, press conference that inflation is running hot. No one in their right mind can say the Fed is meeting their mandate for “stable prices.”

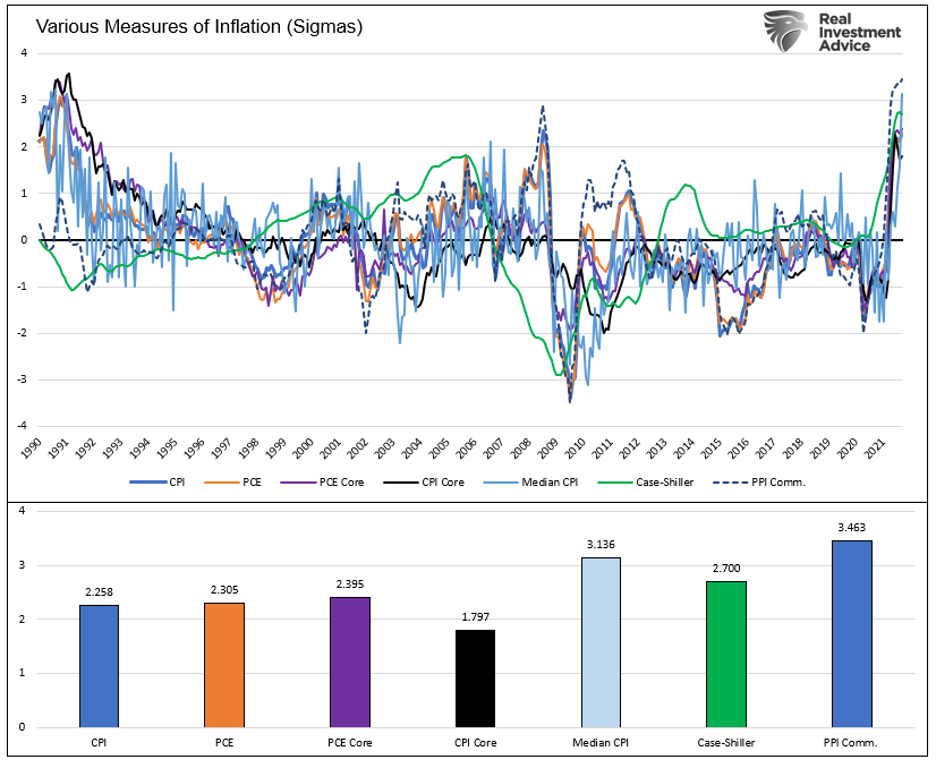

The graph below shows seven indicators of annual inflation rates. I use standard deviation, or sigma, to normalize the seven measures. They are all overextended significantly. In other words, there a very few instances of higher inflation than today in the last 30 years.

On the sole basis of prices, the Fed should be aggressively removing crisis-level monetary accommodations and raising rates to make prices “stable.”

Senator Rick Scott of Florida, in a letter to Chairman Powell, agreed: “Today, American families are faced with rising prices and inflation not seen in 30 years – this is surely not ‘price stability.’

Maximum employment

Inflation is relatively easy to measure with a single number. While we may question the veracity of any inflation figure, we can all agree prices are rising.

Employment is not so easy to measure. Here is what Jerome Powell said on November 3:

So maximum employment is, we say broad based and inclusive goal that’s not directly measurable and changes over time due to various factors. You can’t specify a specific goal. So it’s taking into account quite a broad range of things. And of course, levels of employment, participation are part of that.

The pandemic changed behaviors making some data even more challenging to assess. As such, let’s review traditional and alternative data and see if employment is back to normal.

The unemployment rate

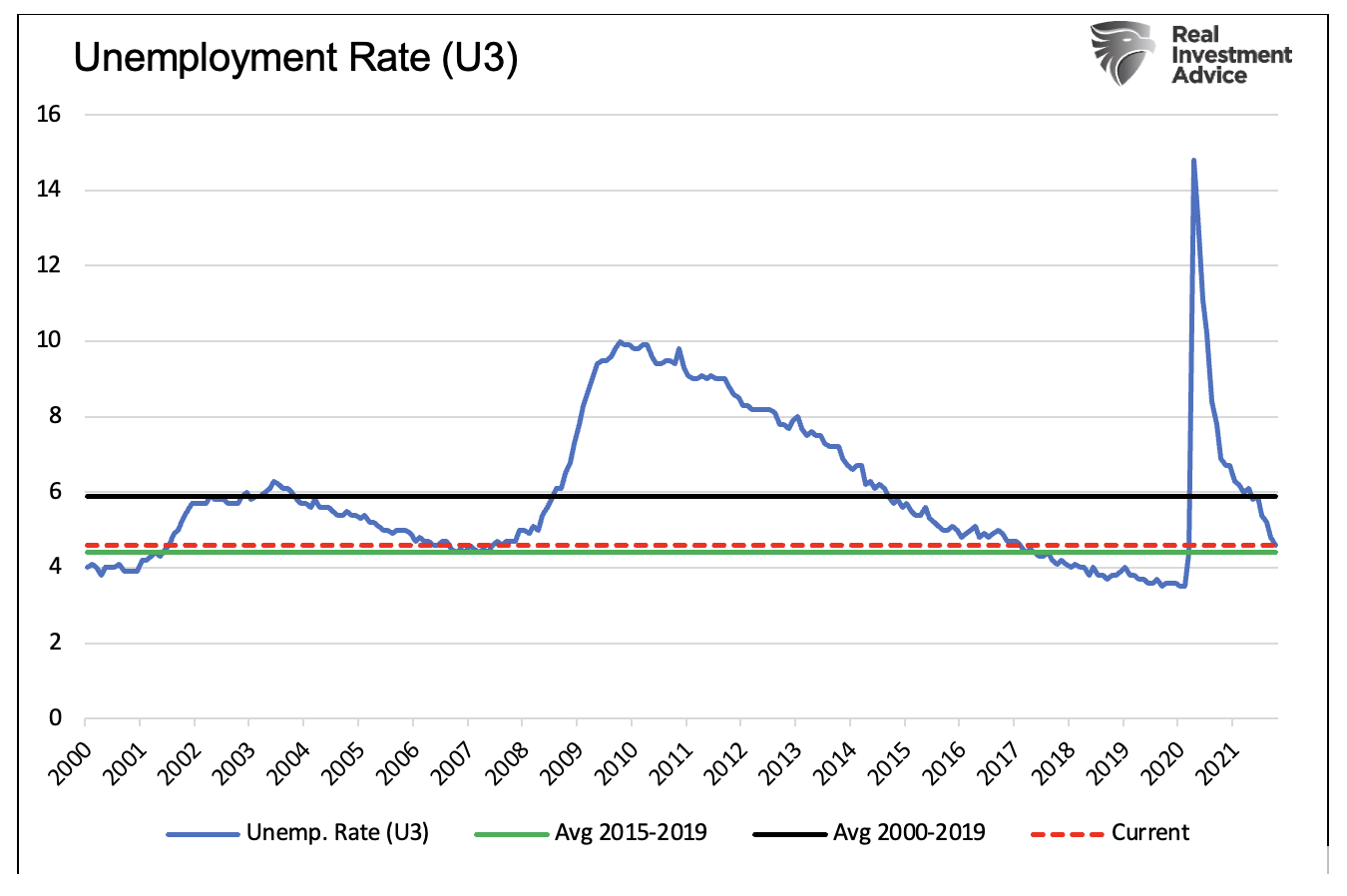

As shown below, the popular U3 unemployment rate, at 4.6%, is only 0.2% above the average of the five years preceding the pandemic. One can argue that period was abnormal as it posted the lowest level of unemployment since the 1960s.

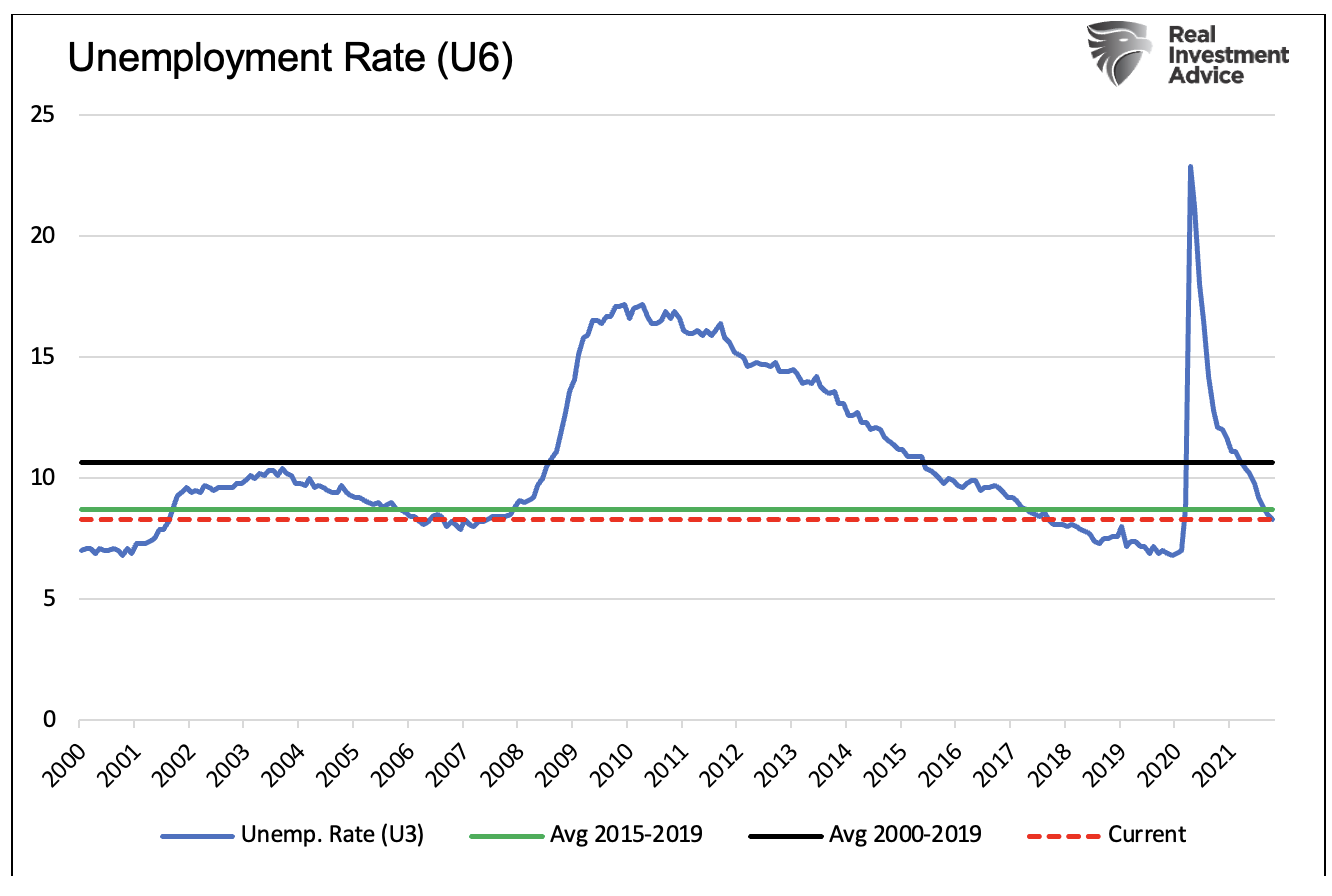

The U6 unemployment rate is not as well followed as the U3 shown above. U6 includes those unemployed in the U3 number but also those underemployed and discouraged from seeking jobs. Jerome Powell thinks the U6 figure is a more credible indicator given the pandemic-related dislocations. As shown below, the U6 rate is 0.4% below the average of the five years leading to the pandemic.

Both traditional measures show the Fed has met its employment mandate.

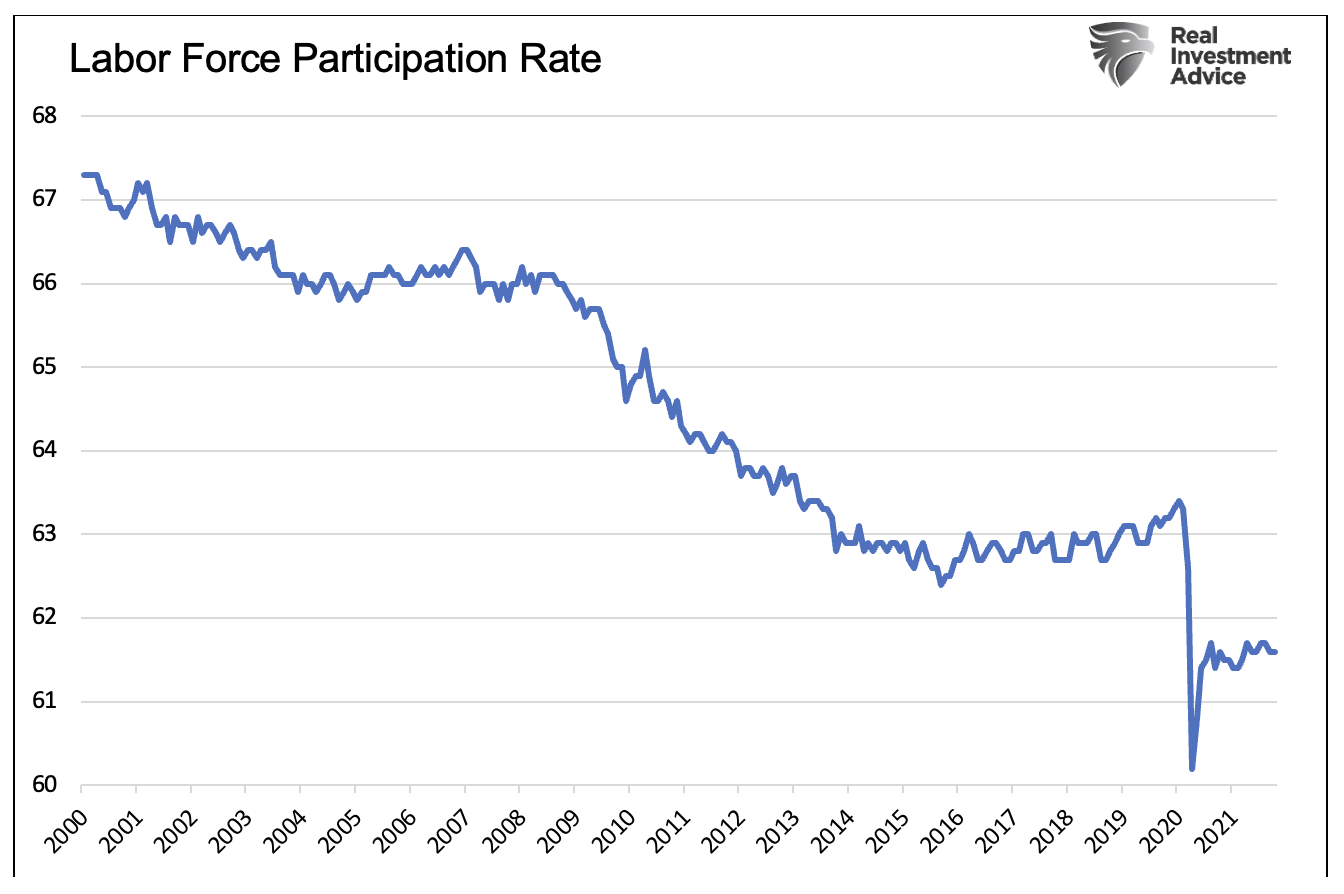

Labor participation rate

Jerome Powell used the word “participation” seven times in his most recent press conference. The paragraph below has three of them:

The unemployment rate was 4.8% in September. This figure understates the shortfall in employment, particularly as participation in the labor market remains subdued. Some of the softness in participation likely reflects the aging of the population and retirements, but participation for prime aged individuals also remains well below pre-pandemic levels.

In his mind, weak labor participation rate is a sign of labor weakness. Labor participation is calculated by dividing the labor force by the total working-age population.

The graph below shows the labor participation rate is about 1.5% below pre-pandemic levels.

Why?

Why are some measures of employment back to normal yet the participation rate slow to recover?

People have left jobs for several reasons. In many instances, people are voluntarily leaving their jobs. For example, some parents are now staying at home with their kids. In other cases, those on the cusp of retiring retired from their jobs. More recently, the number of people quitting jobs is increasing, as workers look for a better or higher-paying job.

- The female labor force participation rates show that women aged 35-44 is still down about 3% from pre-pandemic levels. The participation rate for women aged 25-34 is down about half a percent. Women aged 35-44 are much more likely to have school-aged children than the younger cohort.

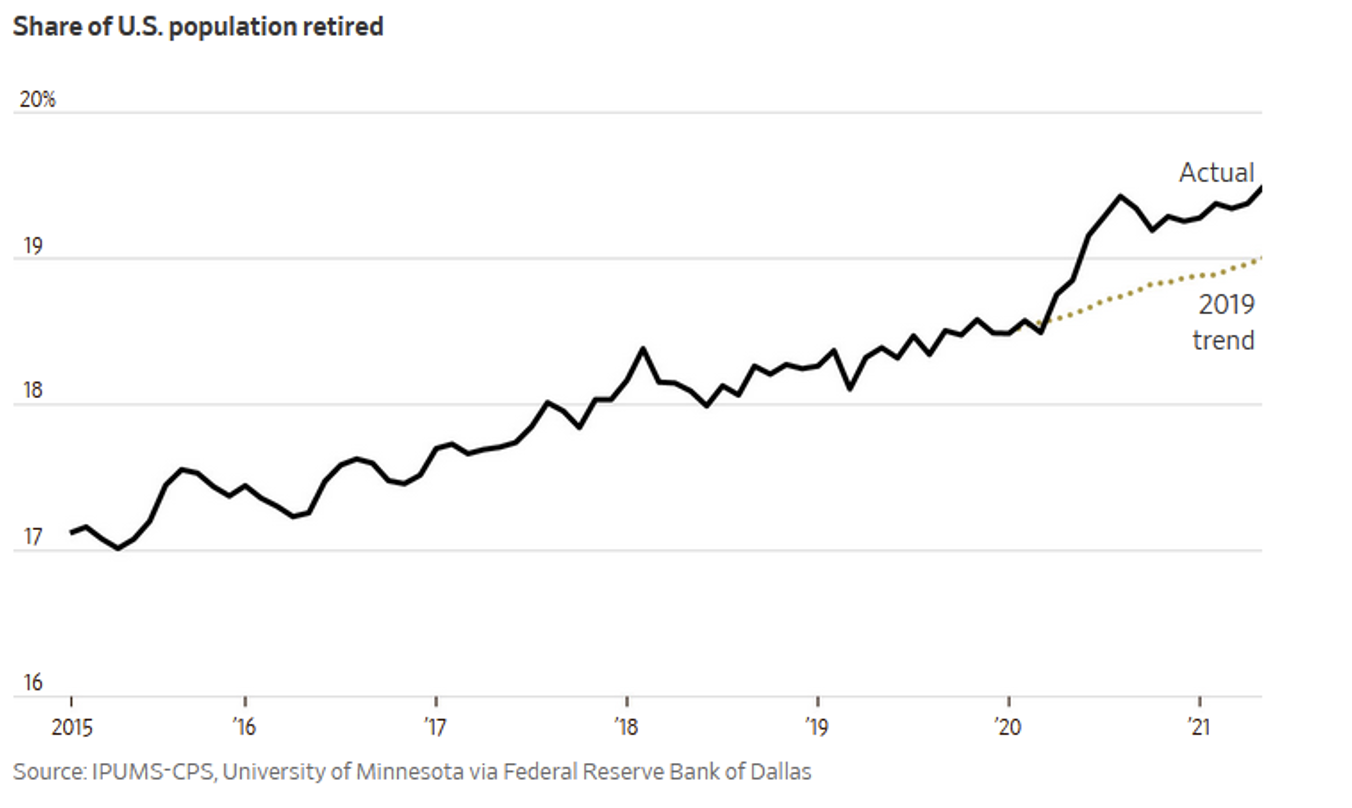

- The Wall Street Journal graph below shows the share of the population that retired since the pandemic rose by about half a percent above its trend.

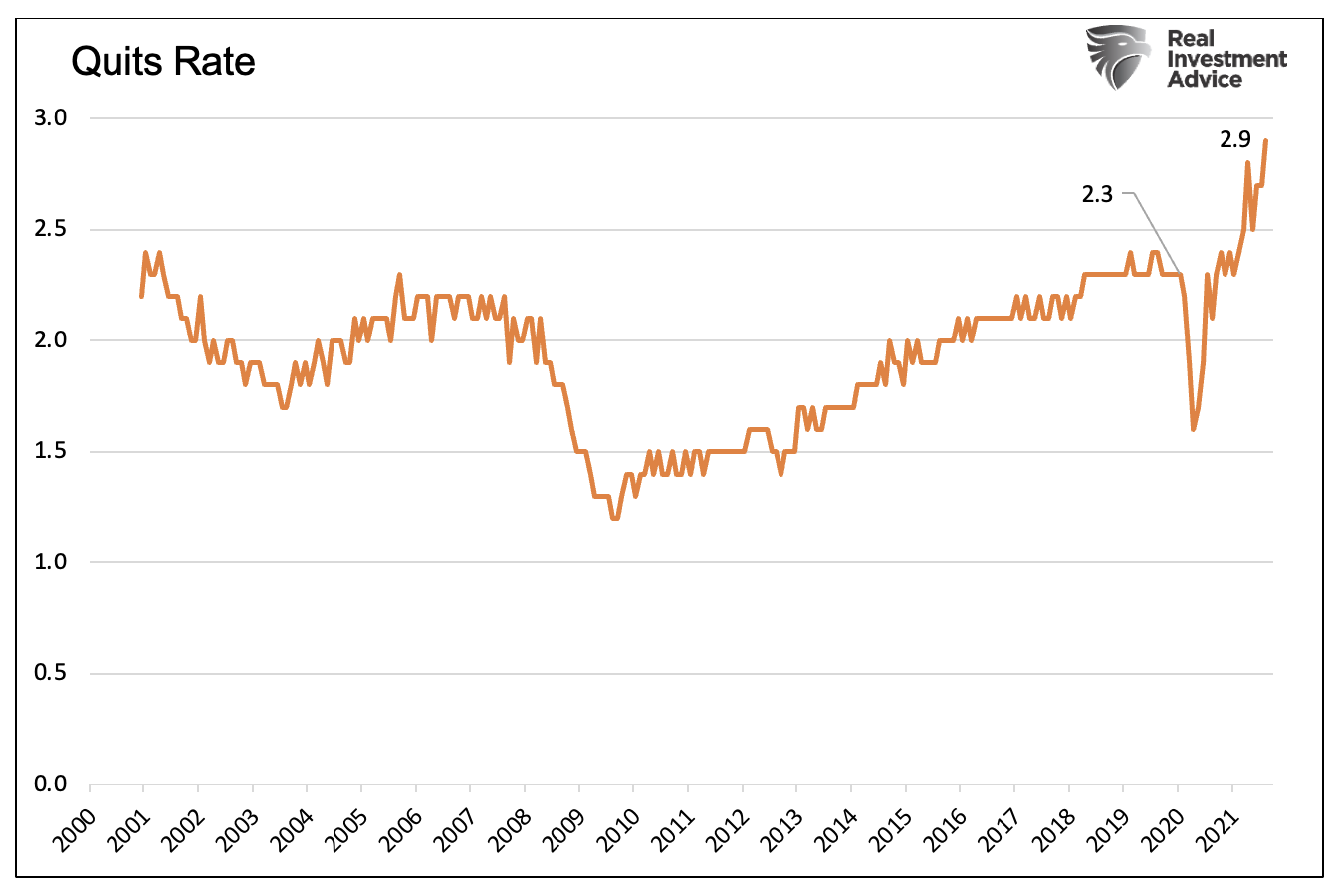

- The graph below shows, the labor quits rate is up .6% since the pandemic started.

While difficult to quantify, when adjusted for voluntary actions, like those above, the participation rate is likely back to where it was before the pandemic.

Job openings

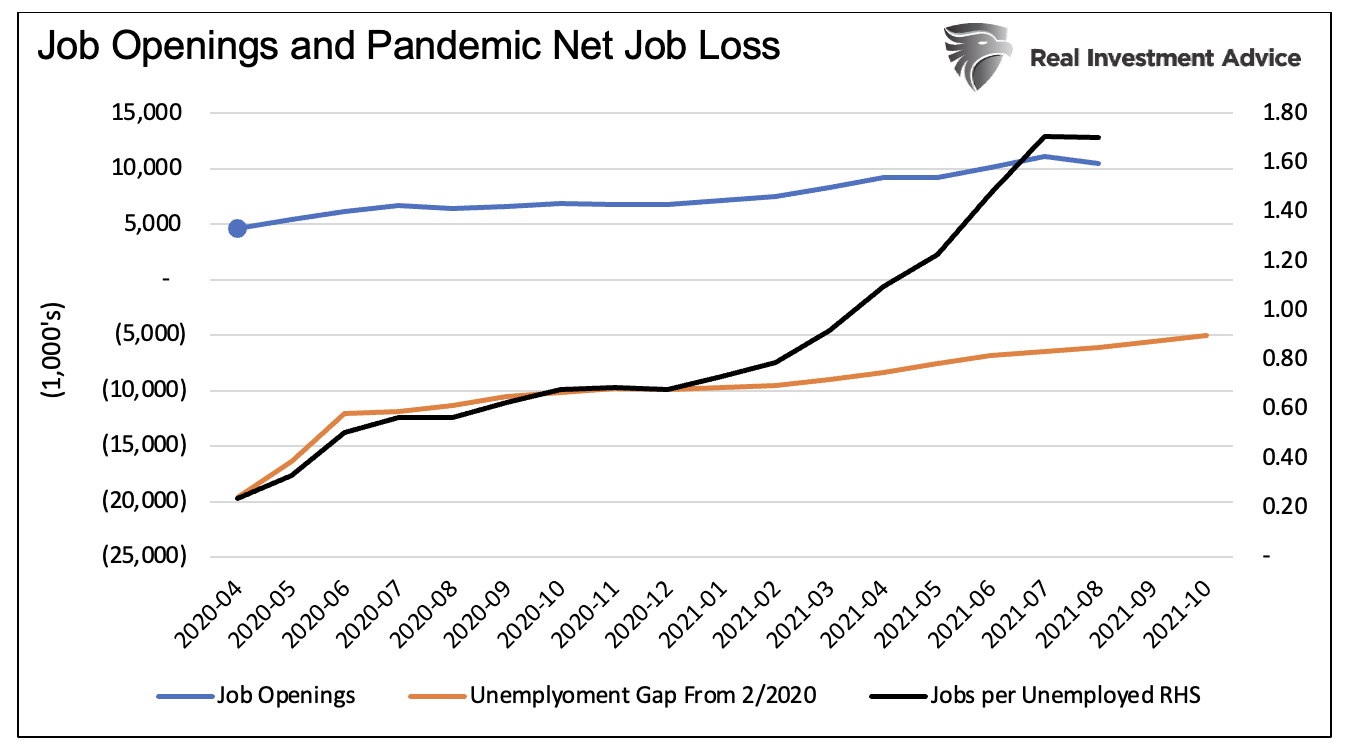

Other alternative indicators are telling us the labor market is robust as well. For instance, the graph below shows there are 1.7 jobs available for every person that lost a job during the pandemic. The data lags BLS data but will likely show further improvement in the months ahead.

The labor market is fully recovered for those willing and able to work. The Fed has met its mandate.

It’s all about “stonks”

Stonks is a meme that purposely misspells stocks. The term is used on social media to imply that many stock traders have a vague understanding of the stock market. The preponderance of amateur “stonk” investors help explain why valuations are extreme and disconnected from reality.

The Fed, through its operations, fosters such a speculative and dare I say reckless environment. For more on this, please read The Fed is Juicing Stocks.

Regardless of whether it is direct or indirect, the “Fed put” encourages risk-taking. Why not take on more risk? The Fed has your back in the event of a downdraft. This was true once again in March of 2020.

Let’s revisit a Powell quote: “The Fed’s policy actions have been guided by our mandate to promote maximum employment and stable prices for the American people along with our responsibilities to promote the stability of the financial system.”

More specifically, he stated: “Our asset purchases have been a critical tool. They helped preserve financial stability early in the pandemic. And since then, have helped foster smooth market functioning and accommodate financial conditions to support the economy.”

Financial stability and smooth market functioning translate to higher asset prices. Paradoxically, at current extreme valuations, financial markets are now more unstable than at just about any other time in history.

This is not news to the Fed. In their most recent Financial Stability Report, it noted: “Asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate.”

Investor risk sentiment is very sensitive to Fed’s actions. You do the math.

From the horse’s mouth

If you do not believe me listen to them.

The following editorial is from the guy that ran QE operations for the Fed:

I can only say: I'm sorry, America. As a former Federal Reserve official, I was responsible for executing the centerpiece program of the Fed's first plunge into the bond-buying experiment known as quantitative easing. The central bank continues to spin QE as a tool for helping Main Street. But I've come to recognize the program for what it really is: the greatest backdoor Wall Street bailout of all time. - Andrew Huszar 2013 -LINK

Summary

Powell’s rationale for not reducing QE quicker or raising rates is either a lie or poor analysis. Either way, the labor market is nearly as strong as any time in the last 30 years.

Prices are far from stable. Inflation is running hot and the odds of supply-related shortages putting pressure on prices grows by the day.

While markets seem calm and healthy, valuations portend they are incredibly risky.

Based solely on the two Fed mandates and its “responsibility” to “foster smooth market functioning” they should halt QE immediately and raise rates tomorrow.

They won’t because doing so would harm the financial markets, and that trumps everything at the Fed.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All