Advocates of active management – particularly those who favor smart-beta strategies – claim that cap-weighting suffers from the irreparable flaw of overweighting a handful of supposedly overvalued high-tech stocks. But that reasoning is flawed.

Advocates of active management – particularly those who favor smart-beta strategies – claim that cap-weighting suffers from the irreparable flaw of overweighting a handful of supposedly overvalued high-tech stocks. But that reasoning is flawed.

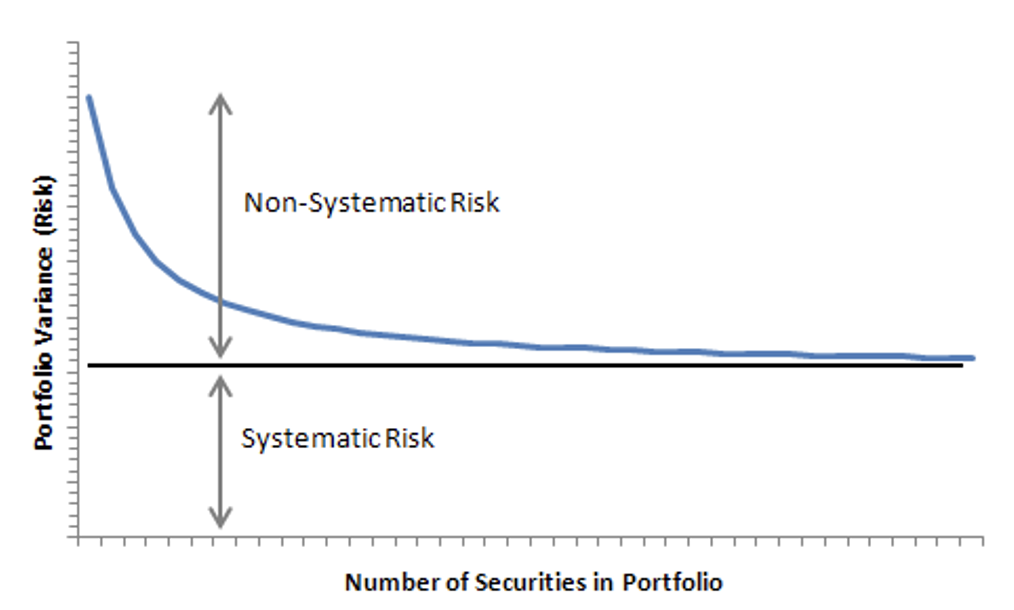

Diversification is the biggest “free lunch” in investing. Modern portfolio theory (MPT) proves a handful of stocks is riskier than the entire market. The risk of a single company is far greater than the risk of a handful of stocks. By owning more stocks, one decreases non-systematic risk, which is the risk the stock will perform worse (or better) than the market overall (also known as idiosyncratic risk). If we own the market, we have eliminated non-systematic risk and are left only with systematic risk. Systematic risk, of course, is the risk of the overall stock market, which cannot be diversified away. The market alone is very risky. MPT uses mean-variance analysis, a mathematical framework for assembling a portfolio of assets such that the expected return is maximized for a given level of risk.

Let’s examine diversification using the U.S. stock market as an example, though other asset classes such as international stock and bonds are also part of a diversified portfolio. The chart above illustrates how non-systematic risk is reduced by owning more stocks. The logical conclusion is that owning every stock eliminates non-systematic risk.

But what should the weighting be for each stock?

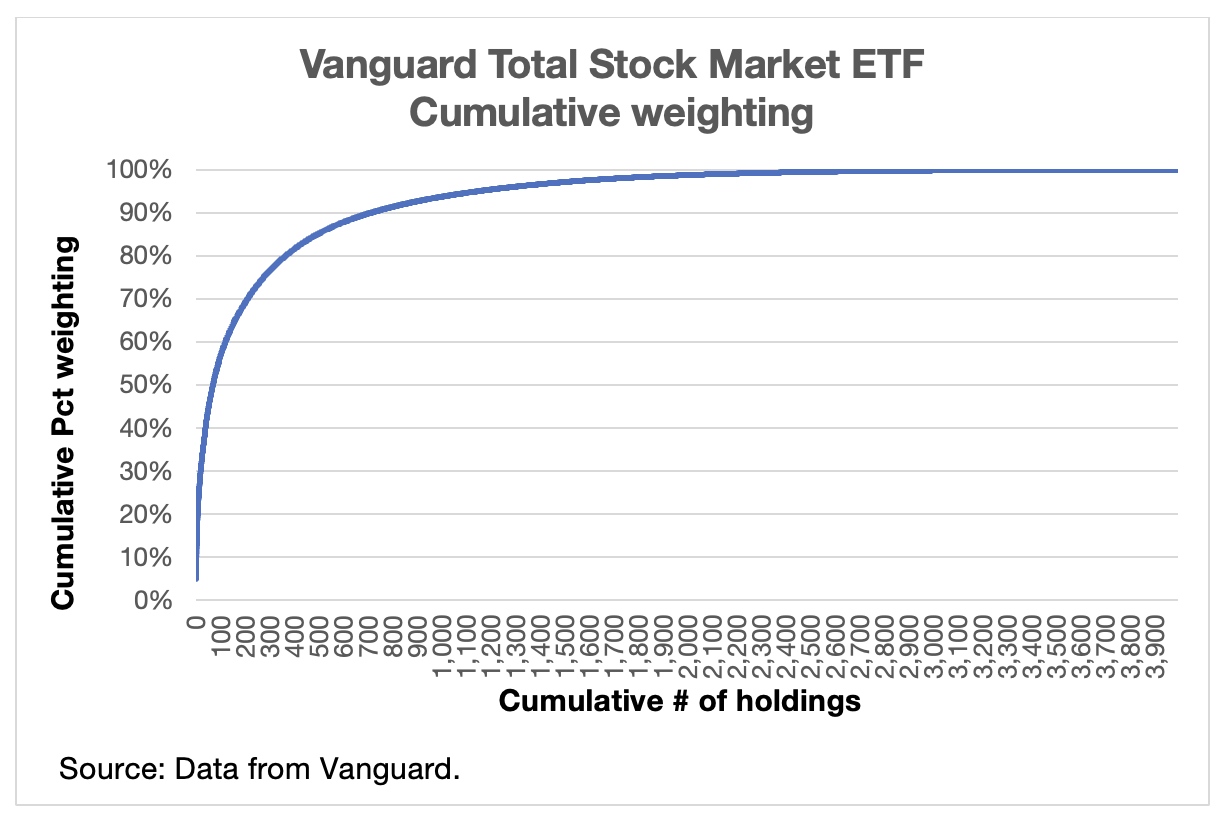

The Vanguard Total Stock Market ETF (VTI) has more assets than any other fund (if we include all share classes). It owns 3,994 stocks though slightly fewer companies, as some companies have more than one share class. On the surface, that is diversified. But critics claim that the cap-weighting methodology, buying very large amounts of a few companies, is flawed.

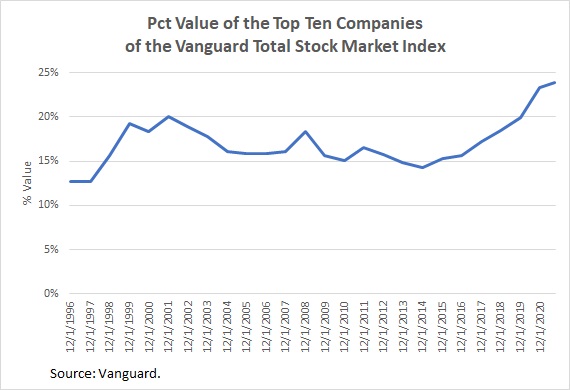

As of September 30, 2021, the top 10 companies (11 stocks as Alphabet has two share classes) comprise nearly 24% of the holdings.

Since 1996, the concentration is at a record high and nearly twice what it was then.

Further these companies are concentrated in technology or tech-related companies. A further drill down reveals:

- The top 70 stocks (1.75% of the holdings) comprise more than half of the market value.

- The bottom 50% (1,997 stocks) comprise only about 1.3% of the market value.

The chart below illustrates the weighting of the VTI fund.

The argument is that cap-weighing the market makes investors dependent on a relatively small number of companies (that some claim are overvalued) and own thousands of companies that have very little impact on return (that some claim are undervalued). For example, if the top 10 companies (11 stocks) declined by 50%, those stocks would cause a nearly 12% loss in VTI. Yet if the bottom 1,997 stocks lost 50%, that would result in only a 0.65% loss.

Are other weighting methodologies more diversified?

The simplest methodology would be equal weighting. But is it feasible? Look to one of the smallest holdings, Allied Healthcare Products (AHPI), to understand why it’s not. An equal weighting would mean this fund would need to own $313.35 million worth of shares, but the total market cap of AHPI is $21.19 million. This methodology would cause this stock to surge, along with many other small-cap stocks. This methodology won’t work.

But other methodologies such as smart beta could. I looked at the FTSE RAFI US 3000 index. It holds 3,174 stocks and is almost as broad as the Vanguard Total Stock Index. Its top 10 holdings comprise about 15.62% of the value. While that’s lower than the 23.9% in the cap-weighted fund, it’s still fairly concentrated. Only Apple, Microsoft, and Berkshire Hathaway are in the same top 10 list as the cap-weighted methodology.

Is it superior? Rob Arnott, chair and founder of Research Affiliates argues it is, because cap weighting is flawed. He states a capitalization-weighted index explicitly links the weight of a holding to its price, so the more expensive a stock gets, the bigger its weight in your portfolio. He states smart-beta strategies break the link between the price of an asset and its weight in the portfolio. Smart-beta weights the holdings based on factors such as volatility, liquidity, quality, value, size and momentum.

Is it more diversified than cap weighting? Clearly the top 10 holdings are less concentrated. But remember the MPT framework of systematic and non-systematic risk. The CRSP US Total Market Index earned 20.99% in 2020, including dividends. That means eliminating all the non-systematic risk earned 20.99% less costs. The Vanguard Total Stock Market ETF (VTI) actually slightly bested the return earning 21.05%. (With securities lending and trading efficiencies, it more than covered the 0.03% annual expense ratio.) But the FTSE RAFI US 3000 index clocked in a return of less than half, at 9.3%, a shortfall of 11.7 percentage points, which is non-systematic risk that this methodology did not diversify away.

Over the next year, the FTSE RAFI US 3000 index could trounce the total market, which would be favorable non-systematic risk. Cathie Wood, whose ARKK fund earned 152% in 2020, had positive non-systematic risk. (The ARKK fund did have small holdings in international stocks, but it clearly bested the market). So far in 2021, ARKK has negative non-systematic risk. Last September, Arnott told me he thought there was a 60% to 70% probability of value outperforming growth in the next year and a 90% probability over the next decade. He may be right but, whether it outperforms or underperforms, that variance to the market is the measurement of non-systematic risk.

Jim Rowley, CFA, head of active/passive portfolio research in Vanguard Investment Strategy Group pointed out that the Vanguard Total Stock Market ETF holds about 4,000 individual stocks as of September 30, 2021. Rowley stated:

Alternative weighting methodologies that deviate from the market-cap weight by underweighting the largest stocks in the index do so by overweighting some other stocks— transferring the risk from the underweighted holdings to the overweighted ones. This leads to at least three forms of active risk: One is at the individual stock level because each of the “other stocks” is overweighted. Two is at the style level because the “other stocks” collectively are mid- and/or small-cap stocks, which means those styles become overweighted relative to large-cap. And three is at the sector level because the “other stocks” are members of various sectors, leading to various overweight and underweight positions across various sectors.

Why owning the entire cap-weighted market virtually guarantees you will beat most investors

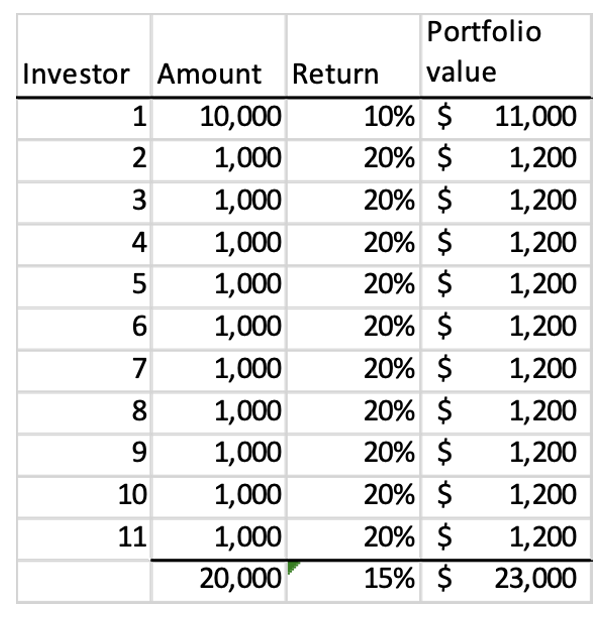

The fewer the number of holdings and the further the variance in weightings, the greater the amount of non-systematic risk (either to the positive or negative). William Sharpe’s paper, The Arithmetic of Active Management, showed the average dollar invested equals the market return less costs. That means the low-cost total stock index fund must beat the average dollar invested.

Does this translate to beating most investors? In theory, no, as I’ll show in this example. If there were 11 market participants with one very large player owning half the market and 10 smaller ones owning the other half, most investors could beat the market. In the example below, the market earns 15% with the giant investor being the underperforming sucker earning only 10%, while the 10 others earn 20%. Thus 10 of 11 (91%) beat the market. The average dollar invested earned 15%, while the vast majority earned 20%.

But let’s leave theory and enter the real world with millions of market participants who are ruled by the law of large numbers. The market participants vary in size from portfolios with billions of dollars to those with very little in their 401(k). But there is evidence that large institutional investors beat smaller investors (including some who use advisors). Large institutions generally pay less in fees.

The brilliance of a total-cap-weighted total-stock index fund is also behavioral. There is a comfort in knowing, irrespective of market performance, the low-cost cap-weighted total-stock index fund will nearly certainly beat investors in that same asset class. We hate to lose money (prospect theory) and especially hate it if we lose more than other people. When a cap-weighted index fund plunges, there is at least a little comfort in knowing others in that asset class lost more.

The same logic for a total U.S. stock index fund is true for international stocks.

Conclusion

Whether a cap-weighted total-stock index fund is the most diversified stock portfolio one can have is debatable, though I think it is. It is undeniably superior in that it has the lowest cost and greatest tax-efficiency and the only way to get the return of the market. It is the optimal stock portfolio. Author and co-founder of Efficient Frontier Advisors, William Bernstein, has it right. As he put it, “A suboptimal portfolio you can stick with is better than an optimal one you can't.”

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

Advocates of active management – particularly those who favor smart-beta strategies – claim that cap-weighting suffers from the irreparable flaw of overweighting a handful of supposedly overvalued high-tech stocks. But that reasoning is flawed.

Advocates of active management – particularly those who favor smart-beta strategies – claim that cap-weighting suffers from the irreparable flaw of overweighting a handful of supposedly overvalued high-tech stocks. But that reasoning is flawed.

Since 1996, the concentration is at a record high and nearly twice what it was then.

Since 1996, the concentration is at a record high and nearly twice what it was then.

Are other weighting methodologies more diversified?

Are other weighting methodologies more diversified?