Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Recently a highly respected financial publisher issued a research paper claiming that the “safe” withdrawal rate from tax-advantaged retirement portfolios could be as low as 3.3%, due to the high valuations of financial investments. As you may know, as an outcome of ongoing research, I recently increased my estimate of the “worst-case” withdrawal rate to 4.7% (for a 30-year time horizon).

How do we make sense of these two widely disparate results?

In the recent past, there have been other claims of low safe withdrawal rates, some less than 3%, made by researchers for whom I have a great deal of respect. What has been lacking in support of these claims are “scenarios”: illustrations of year-by-year assumptions of returns, CPI, and dollar withdrawals, so I could examine the prognostication in detail. These are the bread-and-butter elements of my “deterministic” historical approach but are apparently not so easy to produce using Monte Carlo methods, by which these much lower withdrawal rates have been generated.

Fortunately, in this instance, the author of the study very kindly responded to my request for further information and sent me the spreadsheets used in their simulations. I am very grateful for this, as it allows me to examine the details of their work and discover, finally, why my results differ so much from theirs.

To begin with, in an explanatory e-mail, the author of the report made two important revelations. First, the author announced the study used assumptions of very low returns for financial assets. The median arithmetic return used for their 50% stock/50% bond portfolios was 5.23%. This includes an 8.01% return for the stock portion of their portfolio. This means, consequently, they assumed a forecast for very low bond returns.

Let’s take a short break here and examine how those returns stack up against historical precedent. In the latest iteration of my research, I employed seven asset classes. Five of those are stocks: U.S. large cap, U.S. mid cap, U.S. small cap, U.S. micro cap, and international. The remaining two asset classes are fixed-income: U.S. Treasury bills, and U.S. Government intermediate-term bonds.

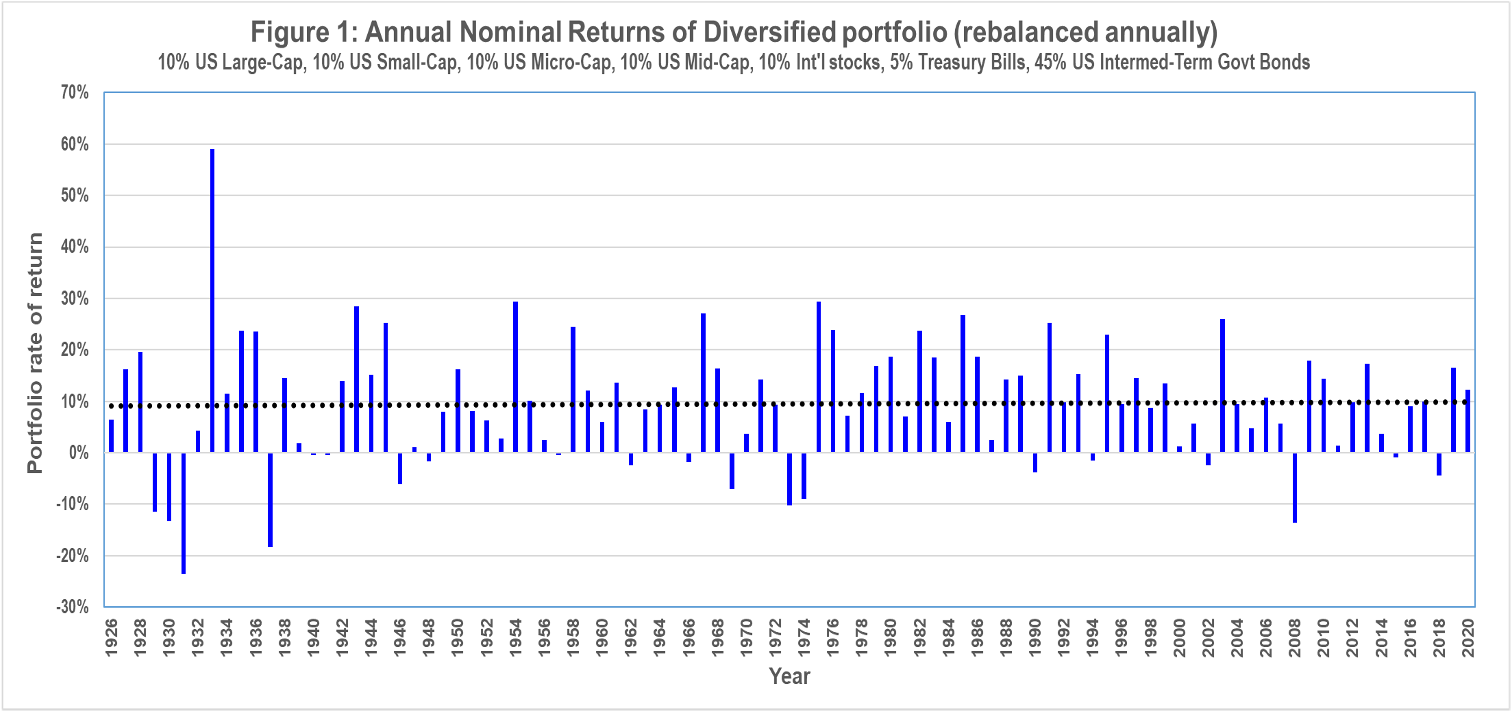

My historical portfolios, consisting of 10% in each of the stock classes, 5% in U.S. Treasury bills, and 45% in U.S. intermediate-term government bonds, have averaged a 9.55% arithmetic return over the years 1926 through 2020 (Figure 1). As you might expect, the geometric (compounded) return is somewhat lower at about 8.9%. Nevertheless, these returns are both much higher than the 5.23% return assumed in the study.

Do my returns seem high to you? We may be tempted to think along these lines: Stocks returned about 10% over the long term, and bonds returned about 5%. For a 50-50 allocation, wouldn’t that suggest a portfolio return of only about 7.5%? Where did that extra two percentage points or so in arithmetic return come from?

Two factors explain why actual portfolio returns were much higher than that: low asset class correlation and portfolio rebalancing (rebalancing at the end of each year is assumed). These two elements exert a powerful effect on portfolio returns. The effects of low correlation between asset classes is well known, as a tenet of Modern Portfolio Theory. Less well understood are the beneficial effects of rebalancing. Through rebalancing, we periodically move funds from asset classes which have just outperformed, to asset classes which have just underperformed. Since there is a cyclicality in the performance of most asset classes, this maintains significant portions of the portfolio in asset classes which have better short-term prospects.

The second point made by the author is that the study assumed that the low expectations for returns would last for the entire 50 years of the study’s time horizon (including, of course, the standard 30-year time horizon). In other words, “mean reversion” is not in play in their analysis.

Is it any wonder, given these two assertions, that a very low withdrawal rate is generated by their computations? Actually, their 3.3% withdrawal rate produced only about a 90% success rate, while mine had a 100% historical success rate, so the difference is even greater than first appears.

I can’t quibble with the forecast of lower returns in the near-term, perhaps out to a decade or more. Today’s asset valuations are at record levels. Therefore, below-average returns might last longer than they have in the past. But 50 years of below-average returns? There is no precedent for such in the historical record. Historically, periods of below-average returns have been followed by above-average returns, and vice versa, generally on the scale of several years, at most. Figure 1 makes this clear.

Who’s correct? The whole issue comes down to whether you accept their forecasts of low returns “forever,” or whether you prefer an approach like mine, which has “mean reversion” built into it. I wouldn’t presume to make that choice for you. But there is an awful lot riding on this for retirees!

As a final comment, the aforementioned study assumed a constant 2.2% inflation rate. As I have stated in the past, elevated and sustained inflation is a greater threat to retirees than low investment returns, as it forces the retiree to “lock in” high withdrawal rates forever. Therein lies the greater threat to the undermining of my 4.7% “safe” rate. Will today’s higher inflation prove to be transitory, as some claim? I don’t know, but as a retiree, I fervently hope so!

William P. Bengen is a retired financial adviser who first articulated the 4% withdrawal rate as a rule of thumb for withdrawal rates from retirement savings. The rule was later further popularized by the Trinity study (1998), based on the same data and similar analysis.

Read more articles by William P. Bengen

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.