Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A week before the January 26th Fed policy meeting, I asked Instability or Inflation, Which Will The Fed Choose?

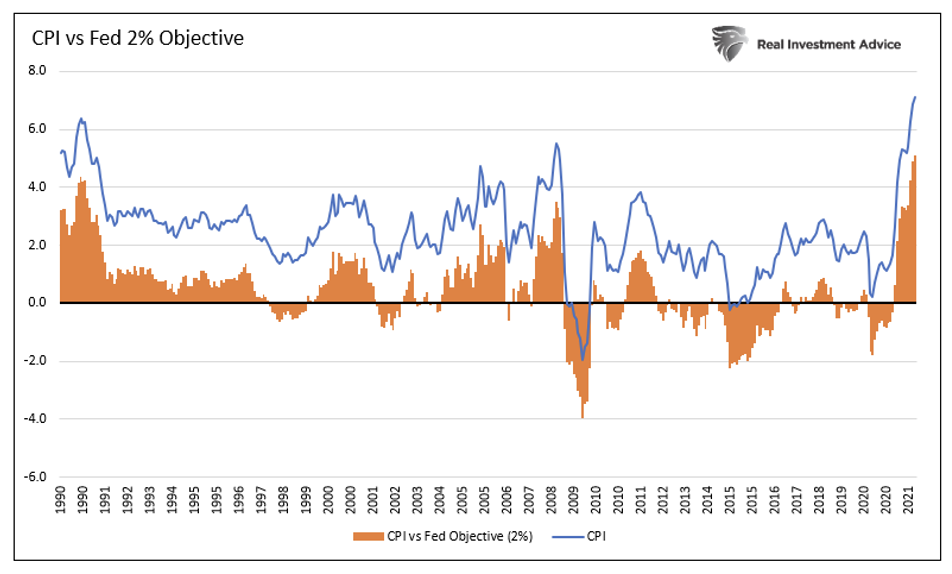

Liquidity is the lifeline of markets and the Fed, directly and indirectly, manages its flow via quantitative easing (QE) and zero rates. With inflation raging, the pandemic subsiding, and economic activity normalizing, the Fed is keen to start reducing liquidity via higher interest rates and reductions in its balance sheet. The purpose of normalizing monetary policy is to bring inflation down. However, the removal of said liquidity could prove problematic for stock prices, especially if done more aggressively than expected.

Per the article:

The Fed is making it clear it wants to reduce inflation. It is also telling us it will ensure financial stability. Sounds like a good plan, but walking the narrow tightrope successfully by achieving lower inflation without destabilizing markets is an incredibly tough task.

I think the odds of success are poor. As such, we must carefully consider which goal it will prioritize when push comes to shove.

Deciphering Fed speak is tedious but given the Fed's new fight on inflation and the considerable impact it can have on markets, it is worth getting a little wonky. Please stick with me as I dissect Powell's insightful press conference and what it may mean for monetary policy and inflation. Equally important is whether Powell is willing to sacrifice the Fed put and leave investors without the support they are accustomed to.

The following LINK provides access to the press conference I will discuss throughout this article.

Will Powell sacrifice the Fed put to quell inflation?

Until the last Fed meeting, I thought the answer was “yes,” but only until the stock market fell by 10% or a little more.

Following Powell's recent FOMC press conference, I may have underestimated his concern for inflation. As such, I now think he is willing to let stock prices fall more than I initially imagined. Might a 20% decline or even more be an acceptable price for Powell?

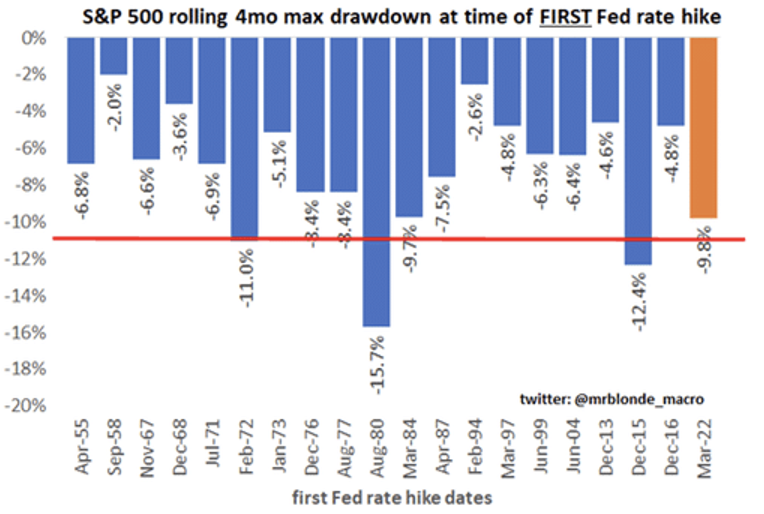

As a point of reference, the recent 10% drawdown is in line with other periods leading to the first rate hike of a tightening cycle.

Powell on inflation

Powell's tone throughout the question-and-answer session was different than prior sessions. Broadly speaking, his confidence level in managing inflation has fallen sharply. At times he appeared shaken by the high and persistent level of inflation. In prior meetings, he brushed off inflation as transitory and purely a function of COVID and related supply-line problems. The arrogance in the Fed's ability to manage inflation has vanished.

Powell's inflation forecast since the mid-December meeting, just six weeks ago, is higher "by a few tenths." More telling, he seems disturbed by the trend higher in prices. He fears the trend is more potent than expected thus will not be as easy to reverse.

That said, he thinks supply line-related price pressures will abate in the latter half of 2022. However, he stressed on numerous occasions that the red-hot labor market will keep upward pressure on inflation. Further, his attention to labor shortages was more acute than before.

He used the word "inflation" 71 times in the one-hour session. While inflation is the most important economic data to watch, those factors that feed inflation, such as the tight labor market, bear close attention.

Political pressure on the Fed

Rachel Siegel asked Chair Powell, "how inflation affects different groups of Americans, especially lower-income earners."

For the first time, Powell reflected on how damaging inflation is and its detrimental impact on lower-income classes. Political pressure from the president and members of Congress are influencing his view on inflation and its harmful effects.

- I think the problem that we're talking about here is really that people are on fixed incomes who are living paycheck to paycheck, they're spending most or all of their – of what they're earning on food, gasoline, rent, heating their heating, things like that, basic necessities. And so inflation right away, right away forces people like that to make very difficult decisions.

- The point is some people are just really in – prone to suffer more. I mean, for people who are economically well off, inflation isn't good. It's bad. High inflation is bad, but they're going to be able to continue to eat and keep their homes and drive their cars and things like that.

- But part of the – part of it is just that it's particularly hard on people with fixed incomes and low incomes who spent most of their income on necessities, which are experiencing high inflation now."

The Fed's shift toward fighting inflation occurred right after Powell met President Biden and secured his renomination bid. We don't know what happened in that meeting but based on the abrupt change in tone around fighting inflation, the president is likely pressuring the Fed to stop high inflation. With a mid-term election around the corner, such is in Biden's best interest. Powell took the bait or, at a minimum, is talking the talk.

Inflation or financial stability

Having established that the Fed is much more serious about fighting inflation, let’s move to financial stability. Investors believe the Fed will do everything in its power to keep higher stock prices and lower bond yields. Many market participants believe the term “financial stability” is Fed code for strong asset markets.

In the conference's last question, a reporter asked about prior hiking cycles and how they were problematic for asset bubbles that resulted from easy monetary policy. Powell's response:

So asset prices are somewhat elevated, and they reflect a high-risk appetite and that sort of thing. I don't really think asset prices themselves represent a significant threat to financial stability, and that's because households are in good shape financially than they have been. Businesses are in good shape financially. Defaults on business loans are low and that kind of thing. The banks are highly capitalized with high liquidity and quite resilient and strong.

He is saying asset prices are not a threat to financial stability. Powell also distinguished asset prices from more valid measures of financial stability. His response was a clear signal that the recent downdraft in prices is not a concern.

Background quantitative tightening (QT)

Curiously Powell used the term "background QT." The phrasing makes it appear QT is not an important issue and should not be followed by the public. Specifically, he claimed QT is in the background to interest rate hikes. His quote reminded me of when Janet Yellen in 2017 declared the QT process would be "like watching paint dry." It turns out the market did not think it was so dull.

"So, again, we think of the balance sheet as moving in a predictable manner, sort of in the background, and that the active tool meeting to meeting is not – both of them, it's the federal funds rate."

Minimizing QT will not get investors to forget about QT. The problem is higher rates and less liquidity are not supportive of record valuations. Investors will link QT with liquidity, just as they link QE with liquidity. As they say, you can't have your cake and eat it too.

Fisher votes inflation

Former Dallas Fed President Richard Fisher provided insight on whether Powell will follow through on his fight against inflation at the expense of the stock market.

Let's face it Joe, I want to come back to the alcohol metaphor we started with, the market has been wearing beer goggles for the longest possible time...and they just assume the Fed's going to bail them out. I think the strike price on the Fed put has moved significantly...and unless we have a dramatic turn in the markets that indicates it can infect the real economy, I don't believe - under this chair in particular who has a credit market background – that they will be weak in following through on what they pronounced.

Summary

The Fed's sensitivity to stock prices is not as acute as some investors believe. In the words of Richard Fisher, the strike price on the Fed put has moved significantly. If this take is correct, the Fed may sit idly by if markets voice displeasure with abrupt changes in monetary policy.

I caveat that statement by reminding you the Fed will relent if stocks fall enough. For the last 30 years, it has been increasingly aggressive in defending markets. While protecting asset prices is not in their Congressional mandate, I have little doubt this time will be different. The only thing that might be different is the losses the Fed will tolerate before it exercises its put.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected]

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Political pressure on the Fed

Political pressure on the Fed