Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Affluent investors and retirees want a perfect solution: an added source of guaranteed (and inflation-indexed) income beside Social Security benefits. But they loath the idea of giving up control over their retirement nest egg. Well, there’s a solution at hand. Fiduciary advisers can help clients achieve these seemingly irreconcilable concepts with a back-to-the-future investment-only variable annuity – IOVA.

Annuities, in one form or another, have been around literally for several millennia. Classic defined-benefit plans are rarer today than dodo bird sightings and Americans are living longer and – with the great resignation – retiring earlier. As a fiduciary adviser, I believe that annuity products can help pre-retirees accumulate assets tax-deferred and provide secure retirement income for retired Americans.

Many retail variable annuities (VAs) are laden unnecessarily with high mortality and expense (M&E) fees, lengthy and hefty surrender charges and unneeded and costly riders.

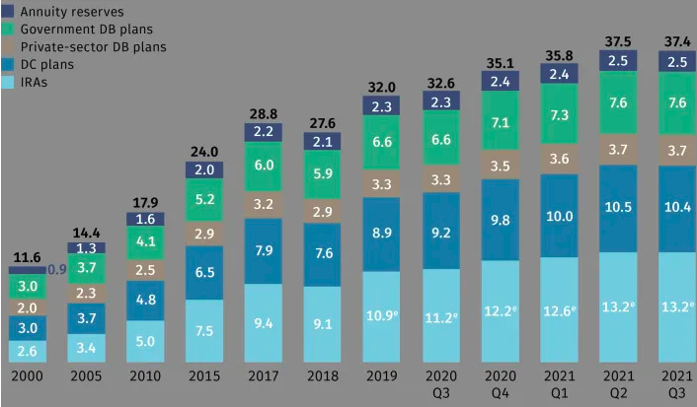

If a particular VA is too expensive, the potential benefits of tax-deferred savings will be undermined by cost drag. Yet in 2021, VA sales soared $125.6 billion and total U.S. VA assets topped $2.5 trillion at year-end.1 (See chart of 2021 Retirement Assets and Annuity Reserves.)

According to Morningstar Direct, the typical M&E charge in 2019 was 1.30%.2 From 2005 – 2019, the average commission charged on retail variable annuities was 6.09% and many VA contracts had all-in annual expenses of 300-350 basis points.3

IOVAs are a fairly recent innovation to VA chassis design. They were first launched circa 2005. The IOVA is a return to the VA inventor’s original idea – tax-deferred growth and purchasing power protection. This return to the future amounts to a simplification of the retail VA design that’s especially attractive for HNW households and UHNW investors. The IOVA has been stripped down to its most basic elements and its original purpose – the potential for capital growth on a tax-deferred basis. An IOVA’s lower cost reduces the risk of depleting wealth and increases the odds of accumulating more wealth, which may result in higher retirement income. An IOVA is a back-to-the-future, fee- and fiduciary-friendly annuity vehicle.

(Image source: “Retirement assets total $37.4 trillion in Q3 2021: ICI”, yahoo!money, 12/20/21)

One way to understand IOVAs is to illustrate what it isn’t! It’s not a retail VA with high costs, added riders ad infinitum, surrender fees and opaque language. It’s not a tax avoidance loophole. IOVAs are authorized under Internal Revenue Code Section 72. IOVAs don’t require medical exams or underwriting. Unlike the IRS limits on 401(k) accounts, IRAs and other executive benefit plan contributions, the only limits on the amount of annuity premiums are set by the carriers themselves.

An IOVA is a very different breed. Most IOVA policies have zero commissions, no surrender charges and low annual M&E and admin fees plus various subaccounts that span traditional and alternative investment strategies. An IOVA is an annuity chassis that returns to the original purpose of a variable annuity vehicle – tax-sheltered growth of equity to protect against inflation effects. Here’s a quick snapshot of generic product features and potential benefits of a fiduciary-friendly, investment-only variable annuity:

- Low M&E charge

- Commission-free variable annuity

- No surrender/no contingent deferred sales charge – CDSC

- No costly/non-essential riders (e.g., GMDB, GMIB or GMWB)

- No annual policy fee

- Open architecture – wide opportunity set of investment choices

- Tax-free exchanges/transfers among investment sub-accounts

- 1035 tax-free policy exchange

- Fixed period or period-certain annuity option

- Inherited non-qualified annuity stretch option

- Standard death benefit (contract value) or optional death benefit (for additional fee)

- No policy underwriting.

“In 2021, fee-based (annuity) products experienced the largest gains as registered investment advisors and broker-dealers sought out tax-deferral solutions for their clients,” according to Todd Giesing of the Secure Retirement Institute.4 In 2021, fee-based advisers sold a record amount of VAs, totaling $4.8 billion. Fee-based annuities sales represented 3.8% of 2021’s annuity sales. But it was and still is one of the fastest growing categories of annuity-linked products.5 It’s past due for fiduciary advisers to take a fresh look at these investment-only annuity vehicles.

When considering an IOVA, a fiduciary adviser can accomplish two goals when recommending investment-only VAs to clients who’ve maxed out their tax-qualified 401(k) and IRA accounts. A fiduciary adviser embraces her/his duty of care by considering alternative investment strategies (which may be tax-inefficient) and practice asset location by recommending that this allocation be made in a tax-advantaged vehicle like a variable annuity.

The ability to own high turnover, actively managed (read, tax-inefficient) funds in a low-cost vehicle is a major advantage of an IOVA chassis. To the extent that a particular IOVA offers alternative investments and managed volatility funds, they provide an implicit form of risk protection. IOVA subaccounts that feature managed volatility strategies can be quite useful for policyholders who use systematic withdrawals (and no surrender fees) to fund retirement spending needs. Although a managed-risk fund might not guarantee an income for life (unless the VA policy is annuitized), it may increase the odds that an investor’s portfolio is more durable in market downturns.

A final reason to consider back-to-the-future IOVAs? The IOVA allows charitable donors to control ownership and distribution of assets earmarked for future bequeaths to non-profit charities and foundations. A philanthropist can name her/his favorite charity as the primary beneficiary of the IOVA while still controlling ultimate disposition of the assets. Conversely, an individual can name a charity or foundation as the contingent beneficiary of the IOVA. That way, the IOVA policyholder maintains the option of the VA’s primary beneficiary to change the terms and disallow any part of the IOVA account value to be disbursed to the designated charity. The IOVA is by and large an undiscovered gem, particularly as it relates to fiduciary advisers seeking solutions for their HNW and Ultra HNW clients.

The author, Rick Roche, is a managing director at Little Harbor Advisors, LLC and 41-year industry veteran. Little Harbor Advisors is the majority-owner of a Chicagoland-based investment and derivatives trading firm, Thompson Capital Management. Little Harbor Advisors (LHA) sponsors “Risk-Responsive Investing” and volatility-influenced strategies. Rick is a frequent industry speaker and has been published in numerous financial trade publications.

1 Secure Retirement Institute, LIMRA, “Total Annuity Sales Jump 16% in 2021 – Marking Highest Sales Since 2008”, January 27, 2022.

2 Morningstar Direct, The average annuity expense charge is 1.30% for all nongroup variable annuity subaccounts in Morningstar as of April 23, 2019.

3 Mark L. Egan, Shan Ge, and Johnny Tang, “Conflicting Interests and the Effect of Fiduciary Duty – Evidence from Variable Annuities”, NBER Working Paper, July 2020, Revised in August 2020, page 12.

4 John Iekel, “Annuity Sales Came on Strong in ’21”, ASPPA, January 28, 2022.

5 Tuohy, C., “Fee-Charging Advisors Sold Record $4.8B of Variable Annuities in 2021”, Life Annuity Specialist, January 31, 2022.

Read more articles by Rick Roche

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.