U.S. stocks slumped the most in 17 months on Monday, but the “buy the dip” mentality isn’t dead in the U.S. — and stock analysts are part of the reason it’s likely to stick around awhile. Research on individual stocks is as bullish as it has been in two decades by some measures.

It’s no wonder investors can’t kick their equities habit despite the largest ground war in Europe since World War II and energy prices that threaten to exacerbate the worst inflation in 40 years. Even as the S&P 500 Index fell 12% from its recent peak, investors are being told repeatedly that the majority of individual stocks have a bright future. From that vantage point, of course, every selloff will look like a buying opportunity.

Of 10,814 analyst ratings on S&P 500 stocks, 58.4% are “buys,” up from 58.2% at the end of the year, before the market had begun to reflect the risk from Russia. While the stock market has pulled back, analysts have been seemingly slow to assimilate the geopolitical threats and have remained generally committed to the price targets their models spit out. Relative to falling prices, those price targets make the upside look rather attractive. But is it, or are these recommendations just changing way too slowly?

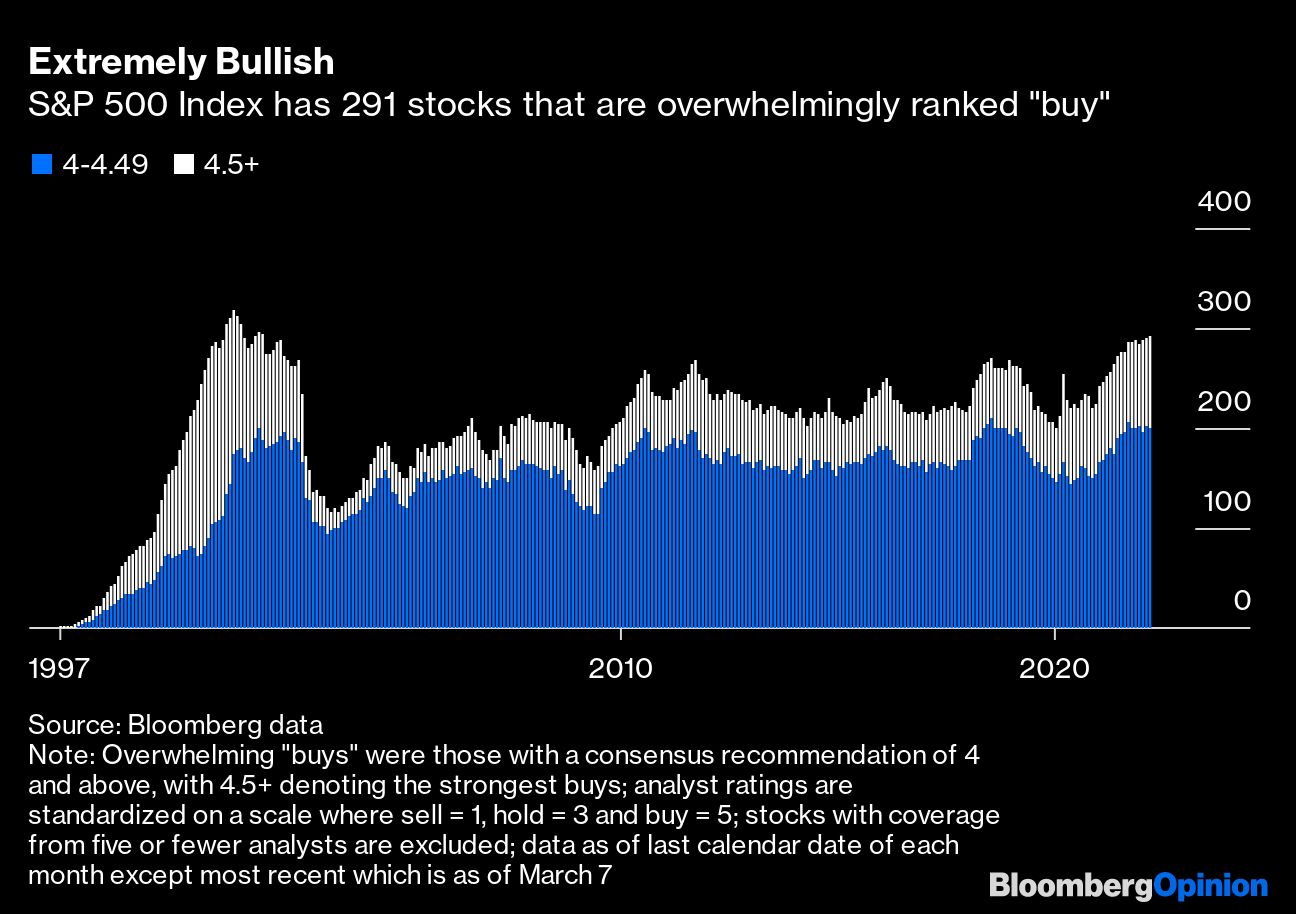

On a company by company basis, 291 stocks look like solid buys, meaning they have a recommendation consensus from analysts of 4 or above (each sell is a 1, each hold a 3 and each buy a 5). That’s the highest in two decades. Of that group, 90 are rated 4.5 or above, also near the most in 20 years.

Specifically, analysts are bullish on the index’s four heaviest-weighted companies. Apple Inc., Microsoft Corp., Google parent Alphabet Inc. and Amazon.com Inc. have consensus recommendations of 4.5, 4.85, 4.92 and 4.96, respectively. (No. 5 Tesla Inc. is in the bottom quintile of the index at 3.4, but the Elon Musk cult of personality more than makes up for the enthusiasm gap.)

When analysts exhibit this much unchecked optimism, it’s not necessarily a good thing. “Buy” recommendations were ubiquitous in 1999 and the early 2000s, before the dot-com bubble fully deflated, and there are some obvious parallels in today’s market. Then, as now, years of juicy returns have conditioned investors to believe that staying bullish pays off. Any analyst who entered the workforce after 2010 (essentially anyone 34 or younger) will understandably have a rosy perspective on markets.

Those who owned or recommended risky stocks in February 2020 weren’t all necessarily chastened by the experience. Instead of humility, what they internalized was the notion that all stock losses would be recovered in a matter of months — and that the market would only surge higher from there.

The current situation is another test for the optimists. Inflation is running so rampant at 7.5% that the Federal Reserve will have to embark on a rate-increase cycle that could risk tipping the economy into recession. Even in a best-case scenario, rising interest rates will mean higher funding costs for companies, threatening the durability of some of the highest equity valuations in recent history.

Certainly, investors can’t be blamed for trying to pick some winners, and that’s an area that stock analysts specialize in. Even if you think stock indexes are about to get crushed, what are you going to do? Park your money in cash and let inflation eat away purchasing power?

With most companies having reported for the latest quarter, some 76% have delivered a positive earnings surprise. Some will withstand whatever the next year brings with Ukraine and the Fed — and inevitably, a handful will make for epic investments.

Dip-buying is ultimately a part of healthy markets, and it will happen no matter what stock analysts say. But in this turbulent market, I worry about the false sense of assurance people get when they consult a report and decide that the war in Europe and other risks aren’t material because the company happens to be doing well.

The incentives in sell-side analysis are well known: Brokerages profit from trades, and firms gets more trades when they recommend buying. Analysts also need access to company executives, and CEOs can stop answering the phone if they don’t like an analyst’s research. The current bullish calls add another layer of sanguineness. The past few weeks notwithstanding, the incredible bull market of the past decade has lulled investors into a sense of complacency, and analysts aren’t doing them any favors by blithely going along for the ride.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.