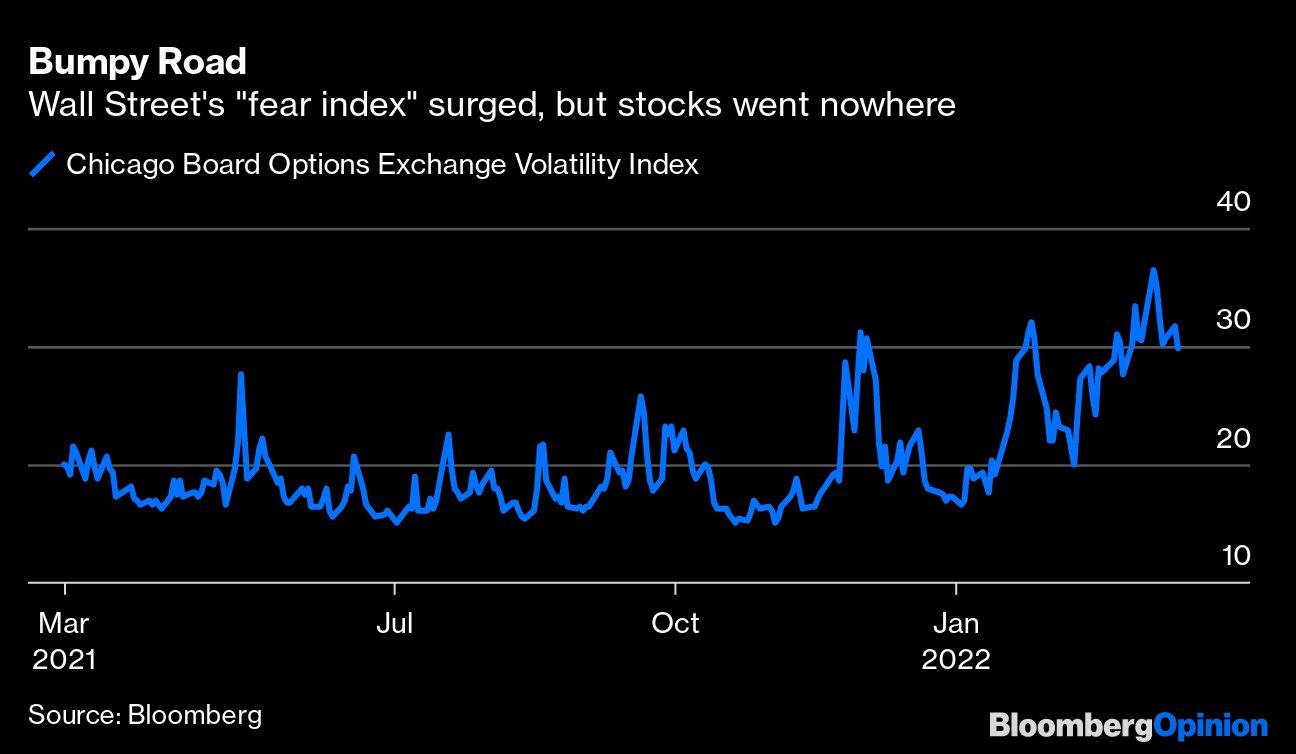

For all their daily volatility, U.S. stocks have been on a bumpy round trip to nowhere since Russia’s bloody invasion of Ukraine began three weeks ago. The S&P 500 Index, Dow Jones Industrial Average and Nasdaq Composite Index have all been basically flat in the period. That suggests either (a) the market thinks it discounted the invasion correctly before it happened, including the rapid rise and fall of oil prices or (b) the market is simply confused by everything that’s transpired and isn’t ready to pick a direction.

I’m betting on the latter, and I think that’s about to change.

As my colleague John Authers wrote this week, the U.S. economy is in ambiguous economic territory when it comes to the war. It’s 5,000 miles from the conflict zone, isn’t particularly dependent on Russian energy and went into 2022 with a rather rosy outlook for growth and corporate earnings. Although it’s certainly vulnerable to a recessionary energy-price shock, oil futures markets seem to have guessed right, at least for now, that the most extreme prices would not persist.

But the U.S. also started with far more exuberant valuations set against the worst inflation in four decades and the promise of rising interest rates, all of which is still true. The growth impact from the war and the retaliatory sanctions won’t be as painful here, but it’s still a net negative on top of an already daunting combination of risks — threats that can be tackled only through a rare combination of deft monetary policy and outside assistance. Strictly speaking, the Federal Reserve needs to raise rates just enough to curb inflation at the same time that other problems beyond its control — high gas prices and snarled supply chains — get resolved somehow.

Ultimately then, the Fed will decide the trajectory of this market, starting with its policy decision on Wednesday. It’s all but certain that the U.S. central bank will announce a 25-basis-point increase, but investors will be parsing Chair Jerome Powell’s words and dissecting the so-called dot plot of rate projections through 2024.

Critically, investors want to know if this will be a “dovish hike” or the start of something more aggressive. Will the Fed lift interest rates a bit — perhaps through its June meeting — and then assess the situation? Or are policymakers already preparing for something even remotely resembling the 1980s campaign of former Fed Chair Paul Volcker, a man Powell considers “one of the greatest public servants of the era.” Volcker, of course, was in charge the last time inflation reached these levels, and unemployment surged during his watch in the name of restoring price stability.

If the Fed begins to answer those questions Wednesday, the U.S. stock market may finally pick a trajectory. A dovish interpretation will probably fuel some semblance of a recovery, while a hawkish takeaway will do the opposite.

Clearly, U.S. stock investors haven’t ignored the war. It has indeed accelerated the rotation away from growth stocks and, to a greater degree, from highly speculative and often unprofitable companies. But the broad market indexes have spun their wheels, and that may be set to change.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.