There are many ways to lose money in down markets, and buying fleeting rebounds is among the best. The Nasdaq Composite Index boomeranged 10% last week from its March 14 low, safety-trade gold posted its worst week since June 2021 and money poured into speculative exchange-traded funds including Cathie Wood’s ARK Innovation ETF.

It’s easy to fall for the idea that the worst is behind us. But with war raging in Ukraine and inflation soaring, the coast is far from clear. So was last week the start of another sucker’s rally? History suggests investors should be wary.

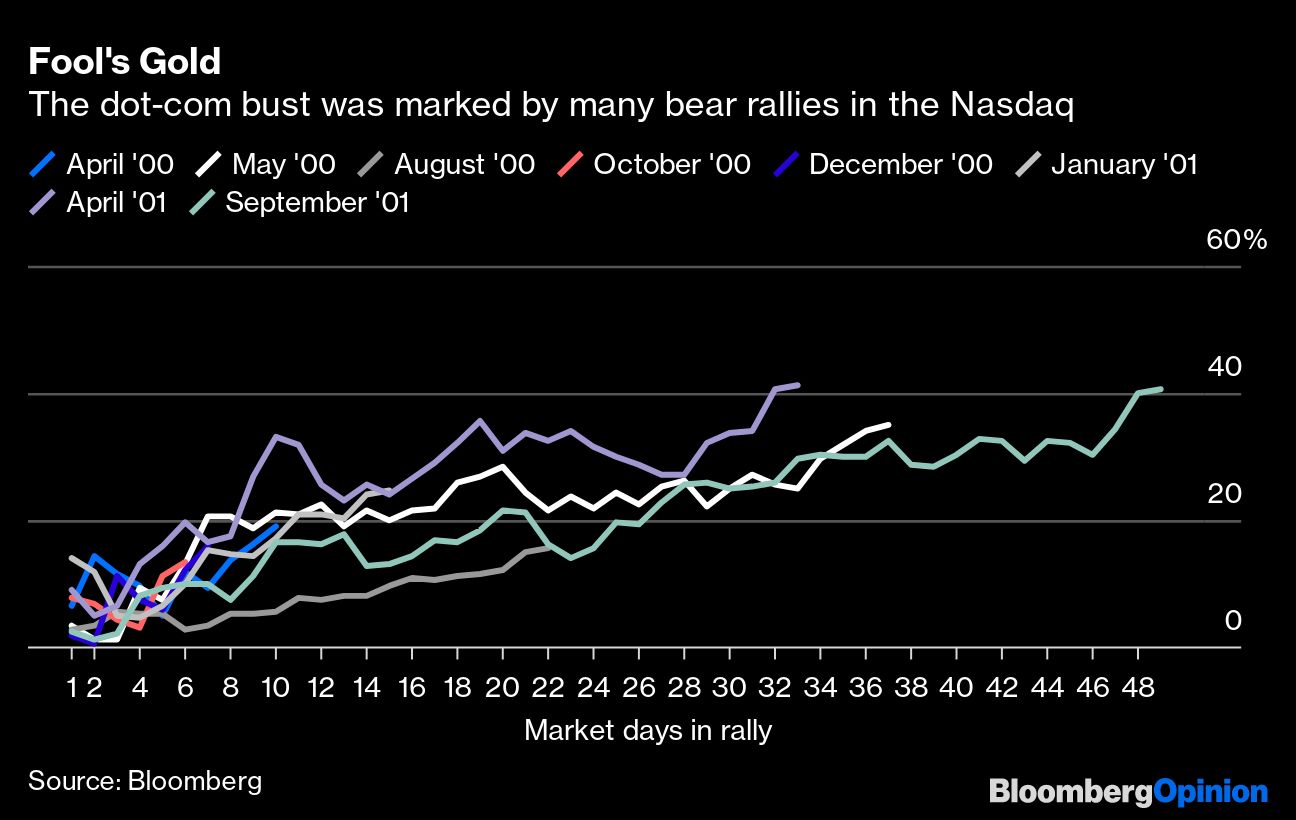

Short-term rebounds are common at the start of a down market. In the first couple years of the dot-com bust, I tallied at least eight significant bear market rallies, with three in the first five months.

Likewise, the Great Recession had at least half a dozen significant bear market rallies, half before and half after Lehman Brothers filed for bankruptcy in September 2008. In both markets, the bounces were insidious because they were so varied in size and duration — from a week to several months long — making it impossible to know at the time the difference between a dead-cat bounce and the start of a new bull market.

So is this 2000 all over again, or is there some fundamental reason to believe the market is set to resume its long-term upward trend?

Let’s review what has transpired. First, the bloody war in Ukraine headed for the one-month mark, with Ukraine rejecting Russia’s demand that it give up the southern port of Mariupol. Diplomatic negotiations have flashed what the market has periodically interpreted as tentative progress, but it’s hard to believe the Kremlin is negotiating in good faith. Meanwhile, Ukrainian President Volodymyr Zelenskiy continued to win pledges of military aid from Western governments, if not a no-fly zone over his country, and Russia paid international bond investors, easing fears of a default for now.

Ultimately, the mixed developments yielded a West Texas Intermediate crude oil price of about $112 a barrel Monday as questions swirled as to whether the European Union would ultimately ban Russian oil imports as part of a new round of sanctions. Despite Monday’s run-up, energy-related risks have started to feel moderately more contained than they did earlier this month, when prices seemed only to rise and nobody knew where the furious surge would end. The market has now gone nearly two weeks without a new high, and that’s taken some of the edge off.

Second, the Federal Reserve delivered on its first rate increase since 2018 as Chair Jerome Powell pulled off the performance of a lifetime. Speaking Wednesday, Powell managed to convince the market not only that he was prepared to fight rising consumer prices but that the U.S. economy and labor market were sufficiently strong to handle higher interest rates and the withdrawal of stimulus that would accompany the inflation fight. Stocks have been more or less jubilant ever since though did pull back some on Monday as Powell gave a speech affirming his willingness to raise the federal funds rate by more than 25 basis points in coming meetings “if we conclude that it is appropriate.” (Nothing new, but the repetition must have finally convinced some investors that he truly means it.)

But this has been a sentiment-driven rally. The pep talk from Powell and the relative stability in oil, though at elevated prices, made everyone feel better, but they don’t add up to much. Vladimir Putin can still shock the market at any time, and investors haven’t fully grasped what it will take to rein in the worst inflation in 40 years. As Morgan Stanley’s chief U.S. equity strategist Michael Wilson put it in a note to clients, the past week was “nothing more than a vicious bear market rally.” He added, “While it may not be completely finished, it is a rally to sell.”

The Nasdaq isn’t technically in a bear market anymore after its recent recovery. For the most part, there’s nothing wrong with buying a diversified portfolio of stocks when they go on sale, especially if you’re investing for the long run to send your newborn baby to college in 18 years. But something tells me that last week’s dip buyers have a more aggressive strategy in mind, and history tells us they should be careful.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin