Our Debt Cannot Be Inflated Away

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Money printing exceeds 2.5 times the combined costs of our recent wars. It’s ginormous. Compounding that problem, the U.S. debt cannot be paid, even in inflated dollars. Serious inflation is inevitable that will crash stock and bond markets, in addition to devaluing the dollar.

Three years ago I wrote Per Capita World Debt Has Surged To More Than $200,000, one of my most-read articles. Many of the comments said money printing is the solution: “Just pay the debt with inflated money.”

In the following, I explore the practicality of settling the debt with newly printed money. We’re poking the inflation bear, but haven’t made a dent in the debt because there’s way too much of it.

Where we are now

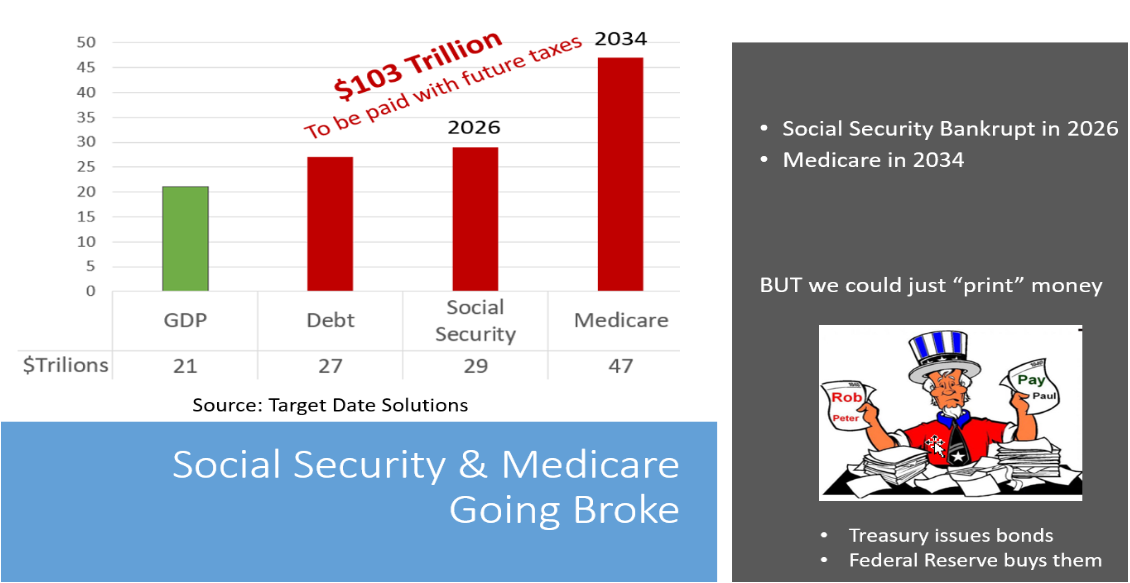

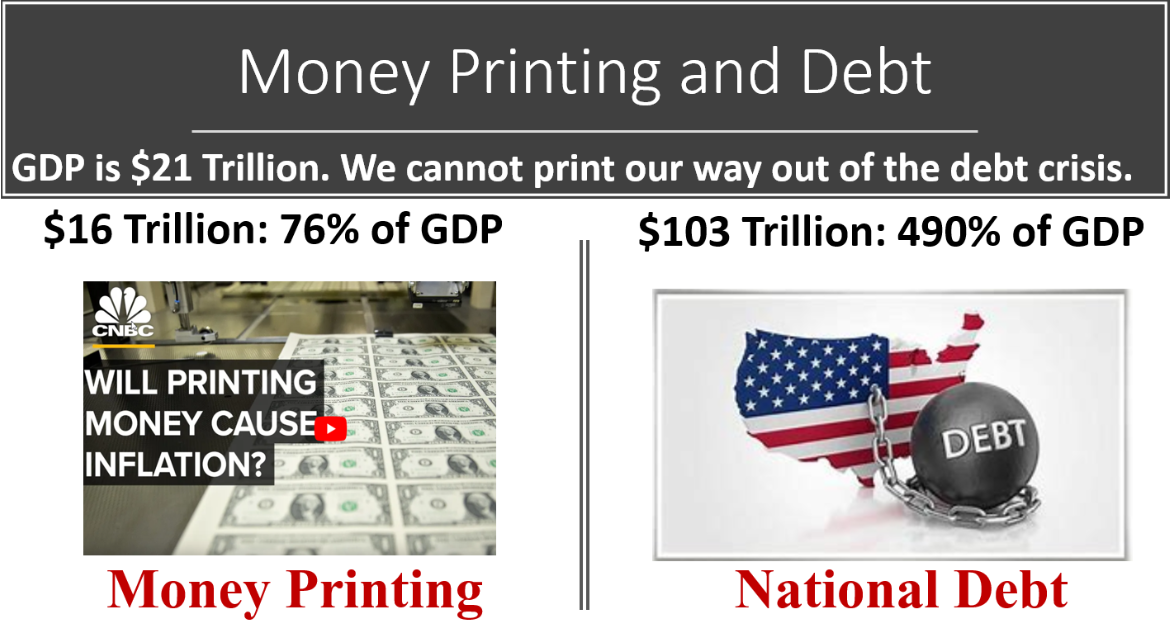

The official U.S. debt of $27 trillion is 130% of GDP, but Professor Lawrence Kotlikoff has warned about “off-balance-sheet debt” from Social Security and Medicare that totals another whopping $76 trillion. All-in U.S. debt is $103 trillion, which is 490% of GDP.

Can the government realistically print $100 trillion? In theory, the government can print all it wants, but it needs to stop when all that money causes serious inflation. There is a limit to how much money can be printed, and we’ve reached it.

Money is “printed” when the Treasury issues bonds. If those bonds do not clear the market, the Federal Reserve buys them. Lately the Federal Reserve has been buying most of the Treasury’s new issues.

Money printing and the U.S. debt

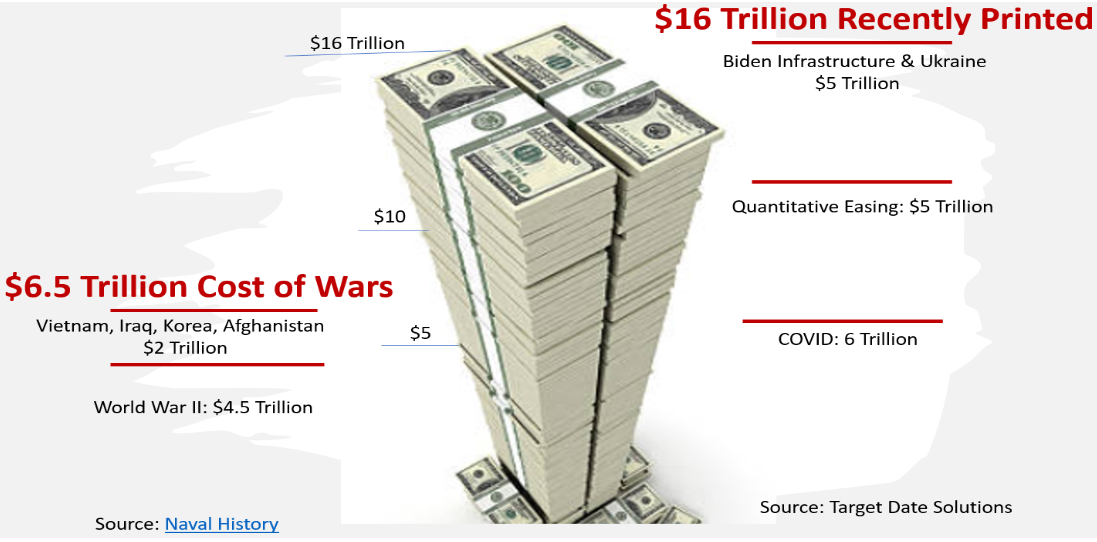

Starting with quantitative easing (QE) in 2009, the government has printed $16 trillion through 2022 so far. This has caused inflation to become serious at 8.5% and rising.

The inflation bear has been poked and it’s furious. The following picture puts $16 trillion in perspective.

A trillion dollars is a lot of money, and $16 trillion is ginormous.

According to CNBC :

If you paid out $1 per second, to settle a $1 million debt would take less than 12 days. To pay off $1 billion would take 32 years. Paying off $1 trillion at a dollar per second? 32,000 years.

A trillion is a 1 followed by 12 zeros, like this: 1,000,000,000,000.

A trillion square miles would cover the surface of 5,000 planet Earths.

A trillion people would be 10 times more than have ever lived (based on the Population Reference Bureau’s very rough estimate of 108 billion humans ever).

A trillion dollars is enough to give $3,195 to every man, woman and child in the United States. (Author’s comment: we actually got this helicopter money doled out in bigger checks)

For a typical U.S. household, making $50,000 per year, to earn enough to pay off a $1 trillion debt would take 20 million years.

The mission is to fight inflation. It came from money printing and will wreak havoc (even hyperinflation) if left unabated.

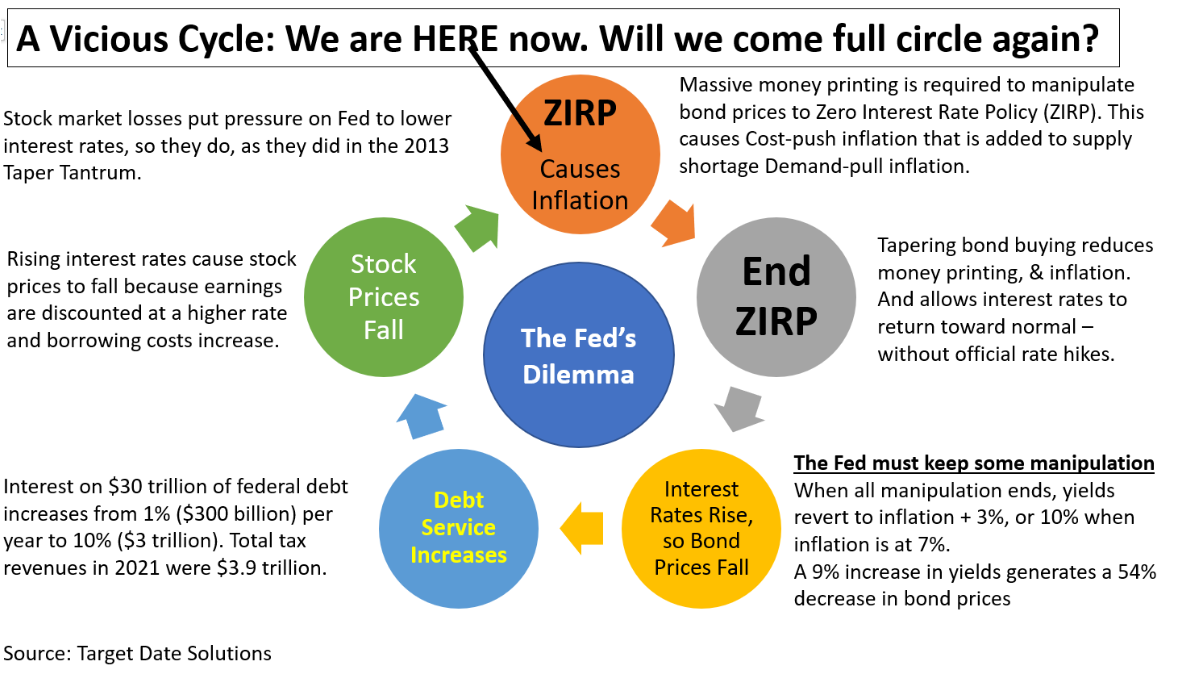

The Federal Reserve to the rescue

The irony is that the Fed has been charged to fight the problem it helped to create. As cowboy wisdom advises, “When you find yourself in a hole, stop digging.” The Fed has been manipulating bond prices to keep interest rates low, executing its zero-interest-rate policy (ZIRP). Now it will have to “taper,” meaning it will allow interest rates to increase.

Rising interest rates are bad for stock and bond markets. Unmanipulated, interest rates will average 3% above inflation, so 11% in an 8% inflationary environment. A 9% increase from 2% to 11% will cause 10-year bond prices to plummet 54% because their duration is 6.

Stock prices will also fall because security analysts will discount future earnings at higher rates. That’s what happened in 2013’s taper tantrum. Stock prices fell in response to tapering, so the Fed backed off. But this time backing off will fuel the inflation fire that the Fed is supposed to extinguish. The following chart details the problem. The Fed is in a corner.

Some say the Fed will opt to maintain ZIRP, allowing inflation to soar. Which do you think the Fed will choose, controlling inflation or interest rates? It can’t do both.

Bursting the stock market bubble

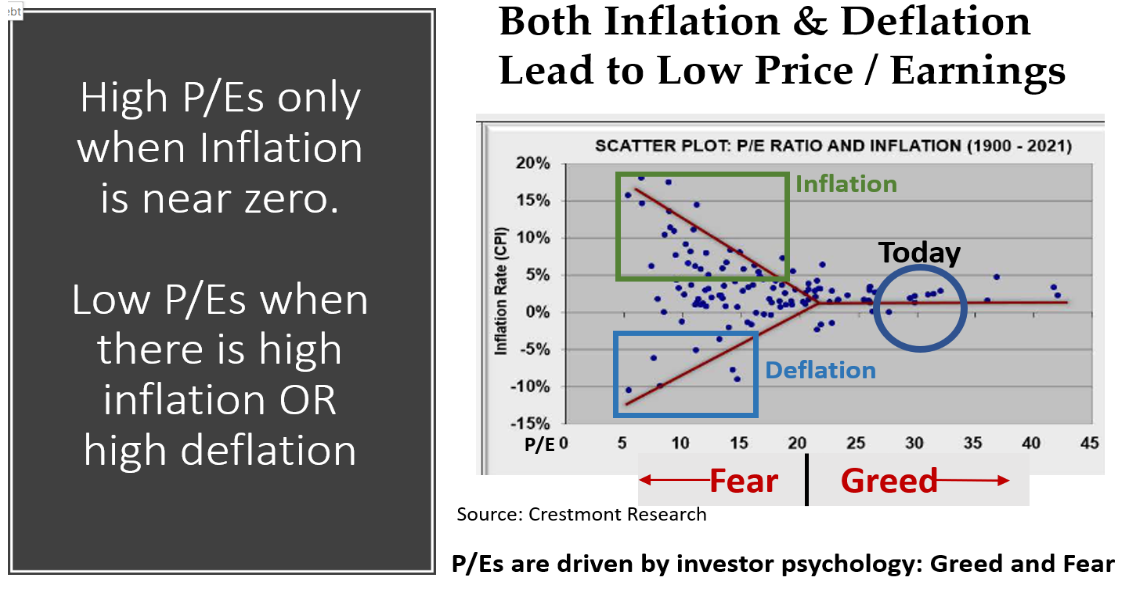

Although many have tried, no one has successfully explained why the U.S. stock market has soared to unprecedented levels – extremely expensive by any measure. But Crestmont Research has documented the necessary level of inflation to sustain high stock prices.

Inflation has to be near zero in order to sustain our high price/earnings, as shown in the image below. The implication is that fear takes hold when inflation is at extremes, either high or low, so investors are unwilling to pay a premium for future earnings.

High inflation will burst the stock market bubble.

Topsy turvy model portfolios

We’ve all heard the investment manager commercial: “You deserve a tailored portfolio, not a cookie-cutter strategy.” And you probably thought to yourself that this was disingenuous since this manager does what every manager does – match you up to an off-the-shelf model.

Most, if not all, money managers and consultants use model portfolios, and most use bonds to limit risk. Low-risk models hold a lot of bonds and high-risk models hold a lot of stocks.

In the next few years, as interest rates rise and bond prices fall, low-risk models will lose more than high-risk models when bond prices fall more than stock prices. Model-portfolio performance will be topsy turvy, disappointing investors.

Target date funds (TDFs) will disappoint too, with near-dated funds losing more than long-dated. Funds for those near retirement are supposed to protect, but they won’t.

The problem is that bonds will not protect for the foreseeable future. To solve this problem, model and TDF developers will need to replace bonds with safe assets like T-bills and Treasury Inflation Protected Securities (TIPS). The Federal Thrift Savings Plan (TSP), for example, uses a government guaranteed G Fund instead of bonds in its TDFs.

Model-portfolio providers, TDFs and turnkey asset management providers (TAMPs) will be slow to make this move to safety and most will never make the change, opting instead to suffer along with competitors.

Challenges create opportunities. New and better models, and model providers, will appear.

Conclusion

Buddha said, “Impermanence is eternal.” The world is always changing. The stage is set for rising inflation that will force up interest rates, and rising interest rates will burst the stock market bubble. Something has to burst it.

A stock market correction is more than 7.5 years overdue.

In the Thucydides Trap, China could get the last laugh if the U.S. dollar loses its status as the world’s reserve currency.

Most of our 78 million baby boomers are in the risk zone spanning the five years before and after retirement when investment losses can irreparably ruin the rest of life. They are especially vulnerable to what lies ahead. They need to protect against losses and inflation with assets like TIPS, commodities, precious metals, and the like. If they are invested in TDFs, they need to get out because they are not safe.

Ron Surz is CEO of Target Date Solutions, Age Sage, and GlidePath Wealth Management, and co-host of the Baby Boomer Investing Show that you can binge watch on Patreon. He authored the Book Baby Boomer Investing in the Perilous Decade of the 2020s.

Please watch and support our Baby Boomer Investing Show and visit our Baby Boomer Libraries, our Target Date Fund blog, and our GlidePath blog.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All