Snap Goes the Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

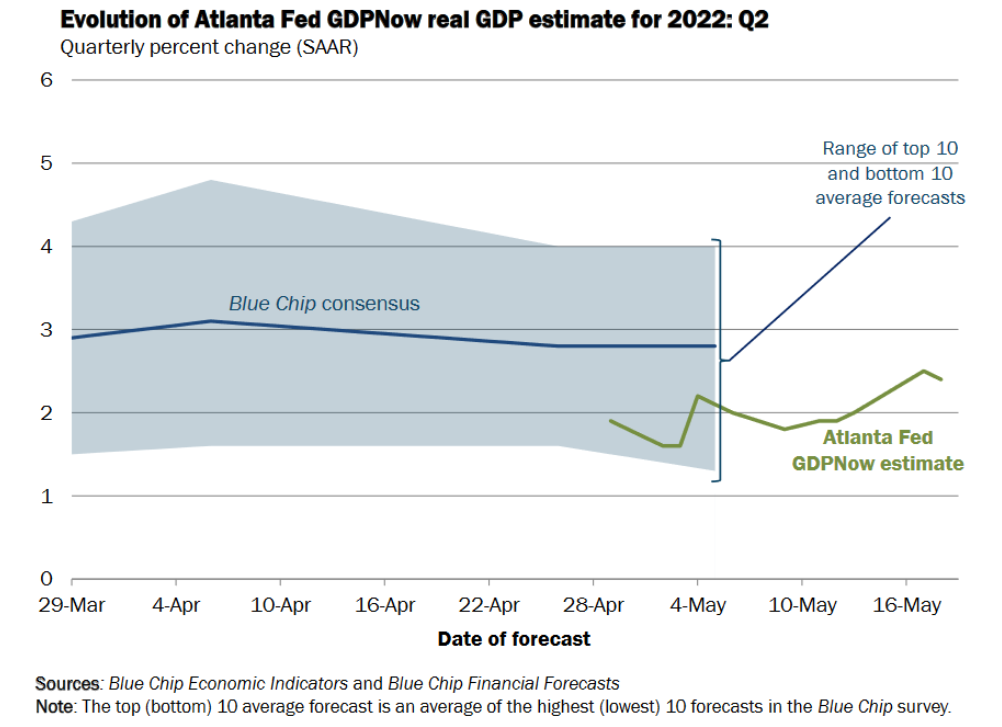

First-quarter 2022 GDP fell by 1.4%. Many economists and Fed members foresaw the economy slowing from its robust 6.9% pace in the fourth quarter of 2021, but few predicted an economic contraction. Despite the poor start to the year, many economists are optimistic about second-quarter growth.

The graph below shows the consensus estimate for second-quarter GDP growth is 3%, and the Atlanta Fed GDPNow model expects 2.4% growth.

Following the first-quarter GDP, economist Ian Shepherdson, a frequent guest on CNBC, wrote, "The economy is not falling into a recession."

I beg to differ with Ian and the "consensus."

Recent warnings from corporate executives and rapidly declining regional manufacturing surveys make me wonder if a recession has already started.

Snap goes advertising

In my Daily Commentary, I led with the following paragraph about Snap, aka Snapchat:

Snap's stock fell over 40% in trading on Tuesday. Concerning us is not necessarily Snap stockholders or even the welfare of the company, but comments from its CEO. Snap's CEO writes in a letter to its employees: "...the macro environment has deteriorated further and faster than we anticipated when we issued our quarterly guidance last month."

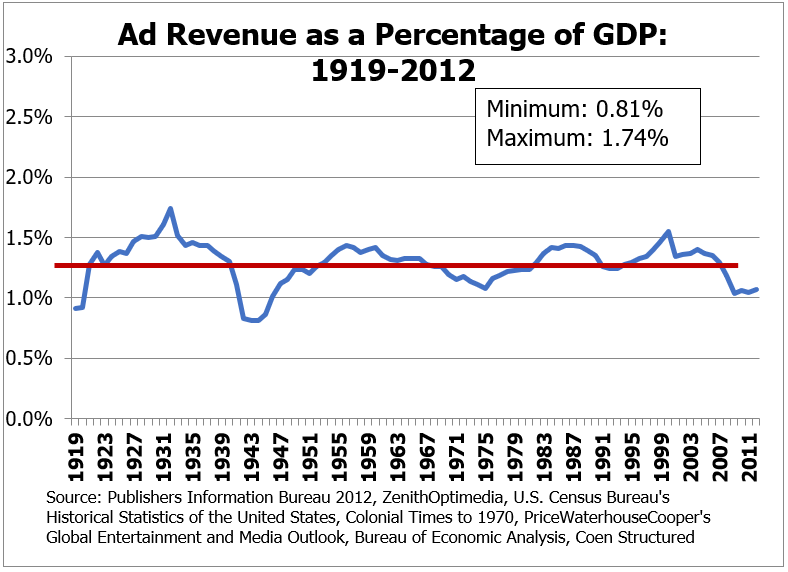

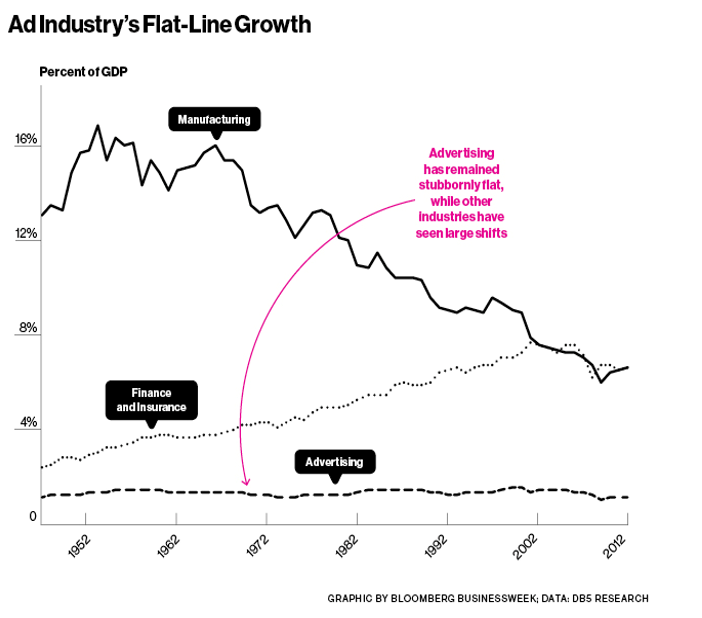

Snap is a social media company deriving 99% of its revenue from advertising. Importantly, from a macro perspective, advertising expenditures tend to track well with the economy per the graphs below.

Snap is just one company, and typically I would not read much into the warning. However, his comments about a "further and faster" decline in the economy are significant because of their timeliness and that advertising expenditures are strongly linked to economic activity.

It is becoming more evident by the day that many companies cannot pass higher prices and expenses on to consumers. As such, they must cut or limit costs wherever possible. Advertising is an easy place to start, as Snap warns.

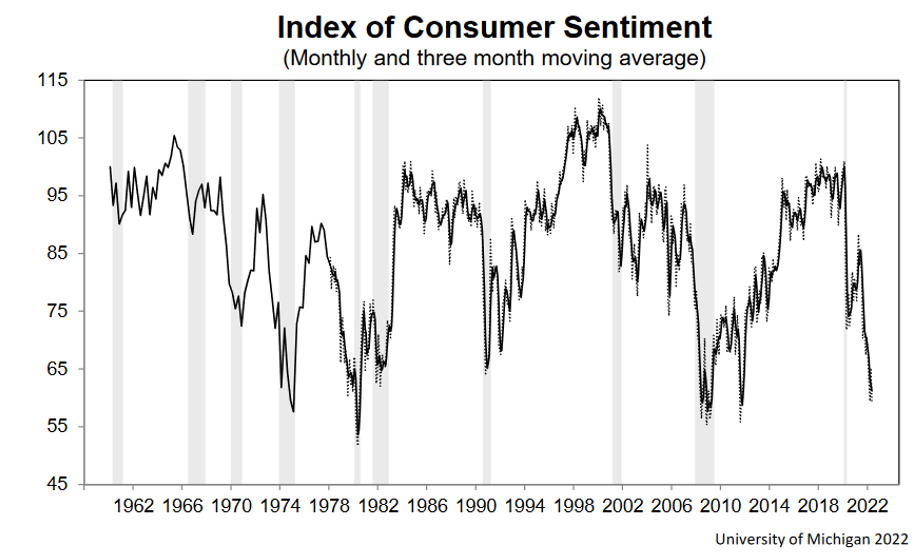

Plunging consumer sentiment

It is not just Snap and the advertising industry that troubles me. Personal consumption accounts for approximately two-thirds of economic activity. Accordingly, consumer sentiment, which is primarily a factor of the financial state of consumers, is an important indicator to follow.

The University of Michigan Consumer Sentiment Survey is near its all-time lows of the last 60 years, as shown below.

Within the report, they cite the following:

Buying conditions for durables reached its lowest reading since the question began appearing on the monthly surveys in 1978, again primarily due to high prices.

Et tu Walmart?

Walmart and Target CEOs offered critical warnings about rising costs and shifting consumer preferences in recent earnings calls.

Per Walmart's CEO Doug McMillon:

Bottom-line results were unexpected and reflect the unusual environment. U.S. inflation levels, particularly in food and fuel, created more pressure on the margin mix and operating costs than we expected.

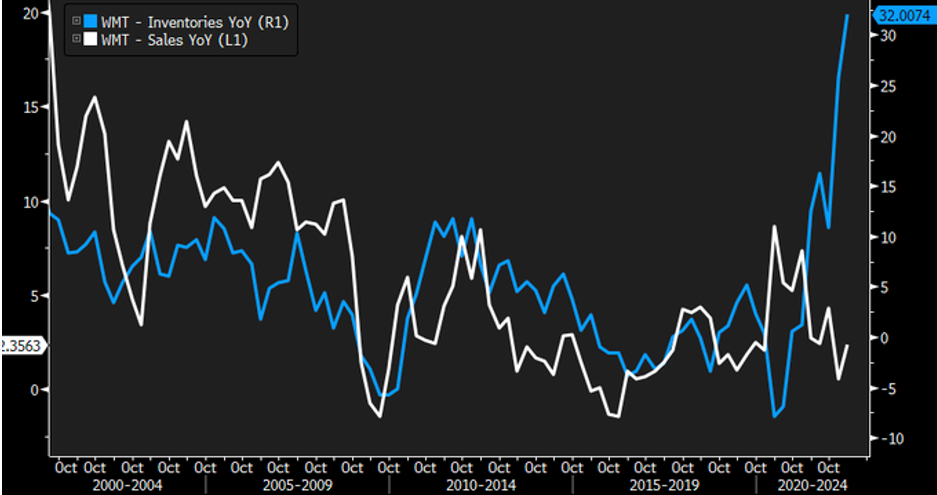

We like the fact that our inventory is up because so much of it is needed to be in stock on our side counters, but a 32% increase is higher than we want. We'll work through most or all of the excess inventory over the next couple of quarters.

Per Target's CEO Brian Cornell:

Throughout the quarter, we faced unexpectedly high costs, driven by a number of factors, resulting in profitability that came in well below our expectations, and well below where we expect to operate over time…lower-than-expected sales of discretionary items from TVs to bicycles

We never expected the kind of cost increases in freight and transportation that we're seeing right now.

Consumers must spend more money on food, gas, and other necessities, leaving less money available for many discretionary products that stores like Target and Walmart sell. At the same time, wages, transportation, and inventory costs are rising rapidly. Retailers are increasingly struggling to pass on those higher costs to their customers.

Equally important, as Doug McMillon mentioned, inventories are increasing. The graph below shows that Walmart's inventories are growing at the fastest rate since 2000. Burgeoning inventories will result in fewer new orders, ultimately weighing on the manufacturers of their goods.

Gloomy regional manufacturing surveys

Economic data from the government is often delayed by at least a month and sometimes a quarter. However, timelier data sources can help us bridge the gap until government data is released.

The prominence of manufacturing in the United States is not what it used to be, but it still strongly correlates with the economy. Helping us assess the state of manufacturing is a series of regional and national surveys. Often the surveys are released within a week or two of when they were taken. Here are a few tidbits from my Daily Commentary on two such recent surveys:

- The May New York Fed Empire State Manufacturing Survey fell sharply into economic contraction levels at -11.6. Last month the Empire index stood at +24.6.

- The Philadelphia Fed Manufacturing Index, like the Empire State Index, came in well short of expectations. The index is now 2.6, down from 17.6 and expectations of 16.5. As shown below, the index still signals manufacturing expansion, but just barely so. The index fell to its lowest level in two years.

On May 24, 2022, the Richmond Fed Survey shrunk into contractionary economic territory at -9, versus a forecast of 10 and previous reading of 14. Per the report:

Additionally, the local business conditions index continued its decline to -16 in May, from -10 in April. Firms are also less optimistic about conditions in the next six months as the index decreased to -13 in May from -1 in April.

Many manufacturing executives surveyed already feel the brunt of weakening economic activity and pushback from retailers.

Stocks, bonds and the Fed

Bond yields have fallen over the last two weeks. Bond investors and traders are breathing a sigh of relief as increasing recession odds should weigh on inflation.

Weakening growth and lower inflation should result in lower bond yields. However, the risk is that inflation does not materially weaken with the economy, yet the Fed becomes less hawkish. If so, bond traders might rightfully fear the Fed is not fighting inflation enough.

Stock investors would love to see the Fed relent from its hawkish rhetoric. However, unlike bond investors, they are not enthused about a possible recession. Pressure will likely remain on stock prices until the Fed relents. If they ease back on the hawkish rhetoric, we must wonder if stock investors will worry the Fed is being too easy on inflation.

Unless there is a steep drop in inflation in the coming months, the Fed runs the risk of reacting to weak economic growth at the expense of taming inflation.

Summary

I would not rule out an announcement later this year by the National Bureau of Economic Research (NBER) backdating an official recession start date to May or even April.

Despite the data and commentary, many economists still discount the possibility of a recession. With one month left in the quarter, there is plenty of time for a resurgence in economic activity. That said, real-time data, including sentiment, corporate earnings, and manufacturing surveys, point to a rapidly slowing economy.

While others wait for more official government economic data, I prefer to consider how quickly weakening economic activity and possibly lower inflation will change Fed rhetoric and ultimately affect our portfolios.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All