The Federal Reserve, the European Central Bank and the Bank of England all preside over inflation rates that have surged to quadruple their 2% targets. One of their brethren is highly skeptical of their chances of success in calming price increases. It may turn out that they’ve been lucky rather than good in achieving price stability in recent years — and their luck has run out.

A few weeks ago, Jeremy Rudd, a senior economist at the Fed, published a paper that does little to inspire confidence in the ability of policy makers to prevent stagflation from afflicting their economies. Moreover, one of his conclusions — that anchoring inflation expectations has little effect on prices — suggests the current mania among central bankers for raising interest rates may exact a cost on growth without a corresponding benefit of achieving their chief policy goal.

Rudd examined a surge in US inflation in the second half of 1960, noting parallels between then and now. It’s his assessment of what’s been learned in the intervening period — or rather, what remains unknown — that’s most striking:

Perhaps the most sobering fact, though, is how little practical benefit six decades’ worth of additional experience has provided us: Our understanding of how the economy works — as well as our ability to predict the effects of shocks and policy actions — is in my view no better today than it was in the 1960s.

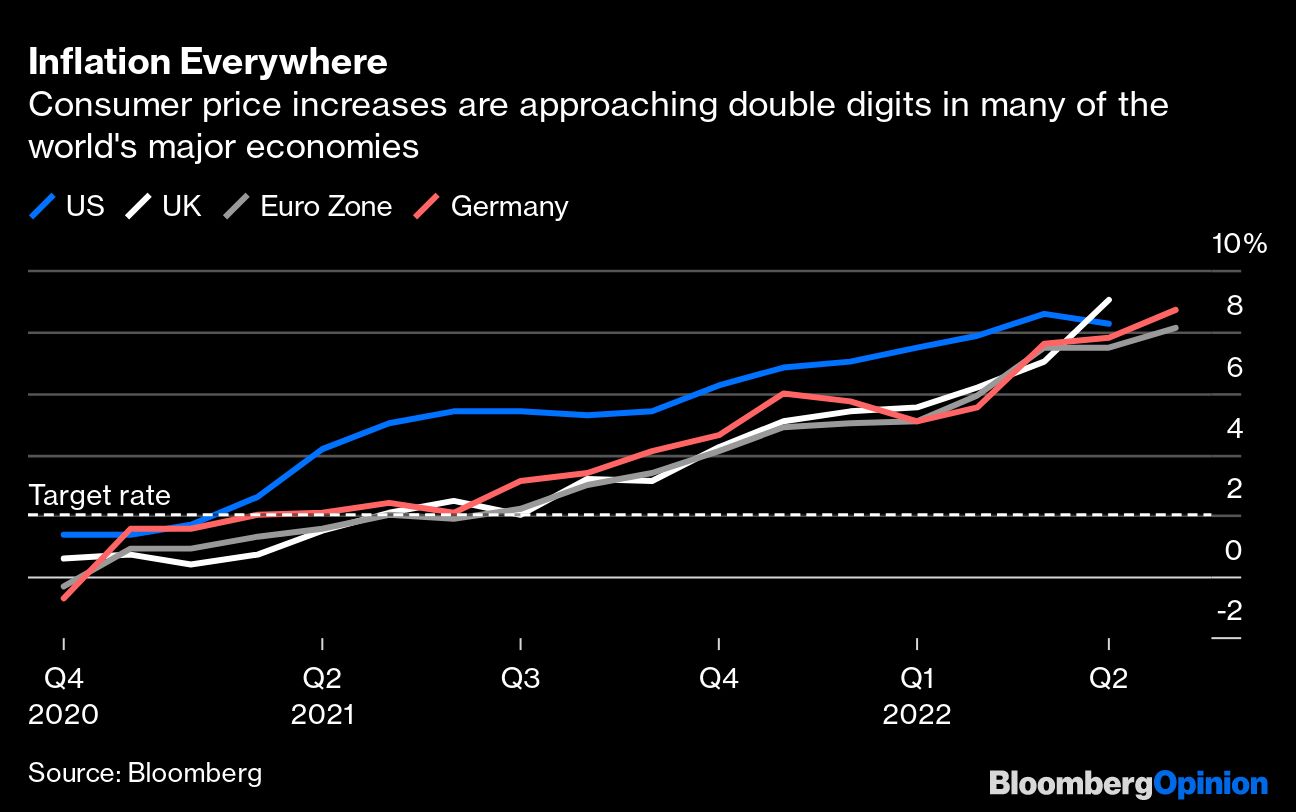

The current bout of rising prices has certainly caught today’s central bankers napping. Figures last week showed consumer prices in the euro zone rising at a record pace of 8.1% in May, up from 7.5% in the previous month and faster than the 7.8% anticipated by economists. In the UK, the Bank of England expects inflation to surpass 10% in the coming months. And economists expect the US to post its fourth consecutive increase of more than 8% on June 10.

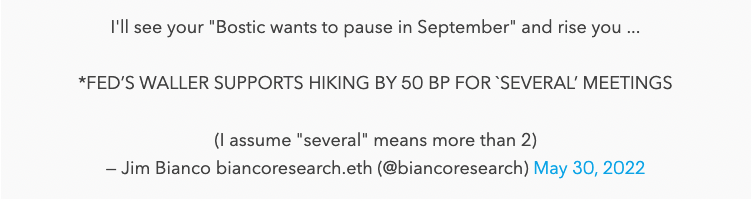

It’s understandable, if not forgivable, that the forward guidance policy makers are currently delivering is all over the place. “For me, I think a pause in September might make sense,” Atlanta Fed President Raphael Bostic said on May 23. Contrast that with Fed Governor Christopher Waller’s comments last week that “I support tightening policy by another 50 basis points for several meetings,” and the path for at least the next three US central bank decisions is as clear as mud, as Jim Bianco of Bianco Research alluded to in a tweet:

ECB President Christine Lagarde has attempted to give financial markets clarity about what her institution is planning, committing last month to raising interest rates by a quarter-point in July and again by the end of the third quarter. That would bring the bank’s deposit rate to zero, up from -0.5%.