Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Depending on risk and diversification, 401(k) plans have lost between 4% and 20% so far this year. Unlike most other periods when stocks lost money, bonds have not defended well this time. Target-date funds (TDF) have a wide spread of performance for those near retirement.

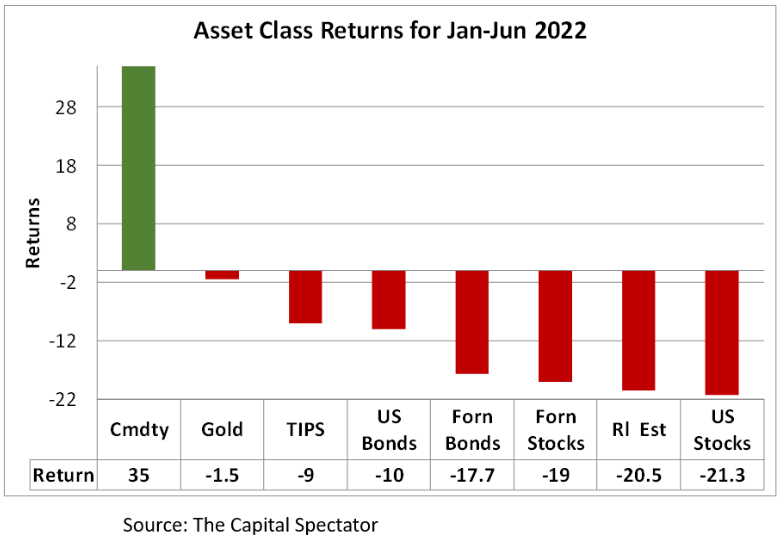

All asset classes except commodities lost money in the first half of 2022. U.S. stocks lost the most, plummeting more than 21%.

How have 401(k) investments fared? The answer to this question usually depends on risk and diversification, but not so this year unless you managed risk with cash.

Traditionally, risk has been controlled with bonds, which have not protected this time, with U.S. bonds losing 10% and foreign bonds losing 17.7%. Going forward, bonds will continue to lose money as the Fed takes the brakes off of its zero interest rate policy (ZIRP).

The loss

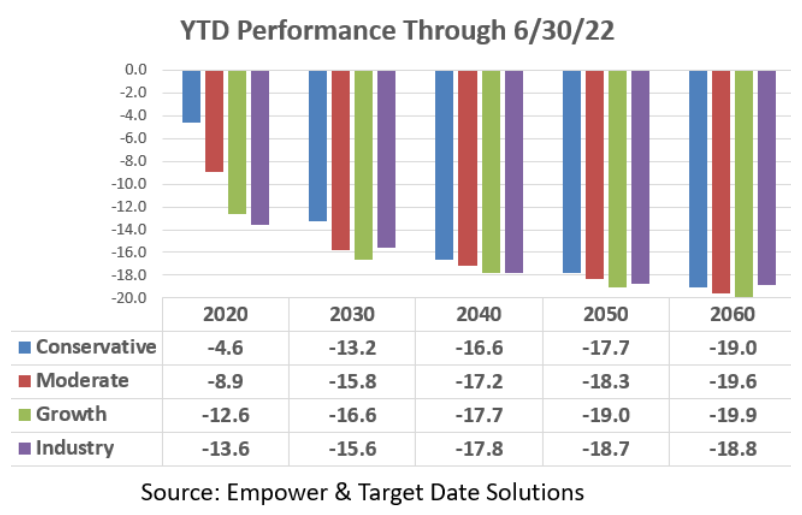

TDF performance provides a good barometer for what investors should expect, as shown in the following graph. Losses can range between 4.6% and 19.9%, a 15% spread, depending on investment horizon and your risk is controlled (managed).

Here’s a breakdown of the results. The important message is that bonds are not protecting.

-

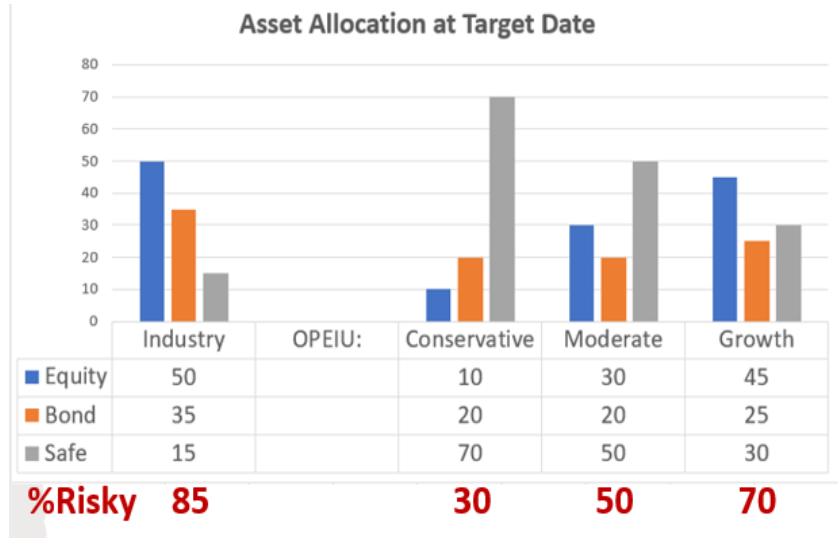

Industry is the S&P TDF index composite of all TDFs. Most TDFs manage risk with bonds. At the target date (2020 fund in the graph) they are 50% in equities and 35% in bonds, so 85% in risky assets, losing 13.6%, protecting by a meager 5% against the 18.8% loss for 2060 funds.

-

The conservative, moderate and growth funds are TDFs used by the National Retirement Savings Plan (NRSP) of the Office & other Professional Employees International Union (OPEIU), one of the largest AFL-CIO unions. It manages risk with stable value. The conservative fund is 70% in stable value at the 2020 target date. The conservative 2020 fund has lost 4.6%, protecting by a substantial 14% against the 19% loss in the 2060 fund.

The growth fund is 30% in stable value, compared to 35% in bonds for the industry. All three OPEIU risk levels have protected more than the industry in their 2020 funds

Conclusion

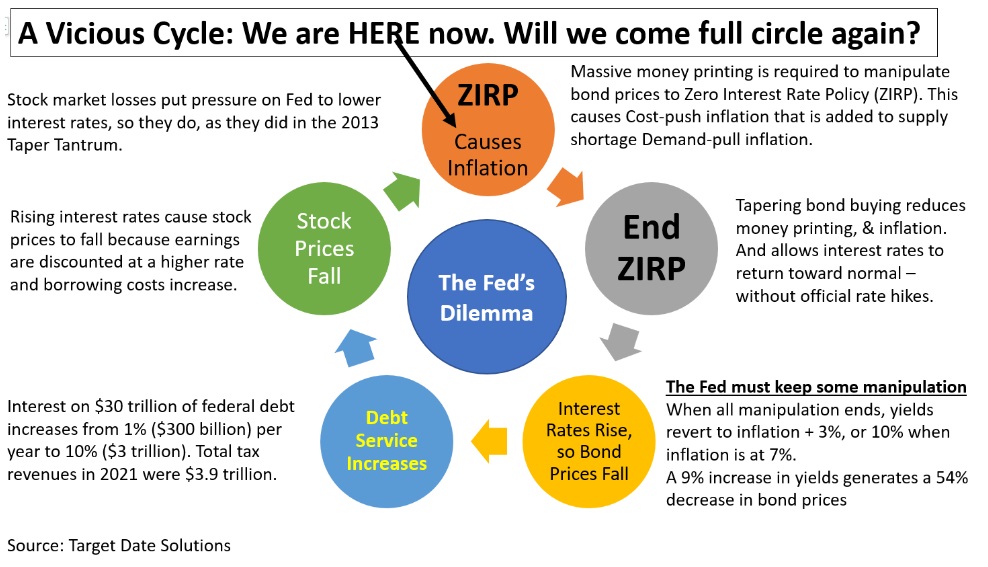

The end of ZIRP is just beginning because the Fed cannot continue ZIRP and fight inflation. ZIRP requires money printing that causes inflation.

The Fed is trapped in the cycle shown below. Many say the Fed will give up the fight against inflation because it harms stock prices. This is what happened in the “taper tantrum” of 2013.

Which do you think the Fed will choose – fight inflation or refuel the stock market bubble? In his Beast on Wall Street book, Dr. Robert Haugen explained that the stock market crash of 1929 was the cause of the Great Depression, rather than a leading indicator. In other words, concerns about a recession should center on the U.S. stock market.

Ronald Surz is co-host of the Baby Boomer Investing Show and president of Target Date Solutions and Age Sage, Target Date Solutions serves institutional investors, namely 401(k) plans. Age Sage serves do-it-yourself individual investors.

His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book Baby Boomer Investing in the Perilous 2020s and he provides a financial educational curriculum .

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.