Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Many investors fail to understand the nuances and complexities of mortgage-backed securities (MBS). As a result, few can appreciate institutional MBS investors' role in the recent bond market rout. Instead of complaining about recent bond losses, our time is better spent exploring the machinations of MBS investors to assess where yields might be going.

This somewhat wonky article explores the unique qualities distinguishing MBS from other bond types. These characteristics help us appreciate how MBS investors contributed to the recent yield surge. Further, gives bond investors optimism that a good opportunity is approaching with a big group of bond sellers out of the way.

MBS 101

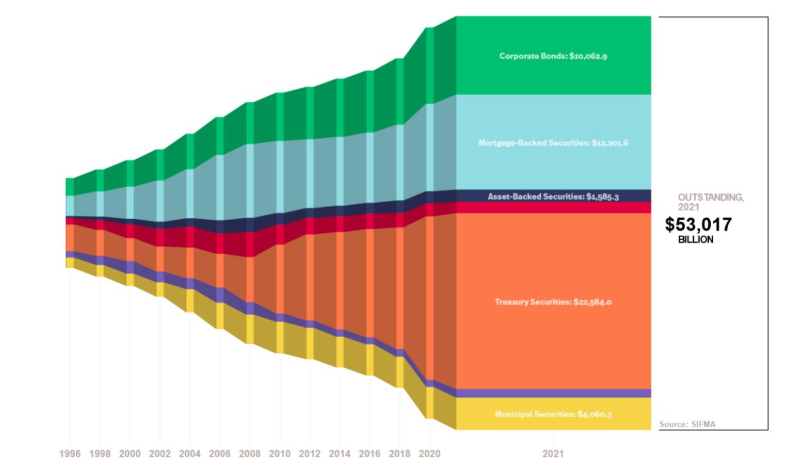

MBS are bonds secured by individual mortgages having similar characteristics. The graph below from SIFMA shows that MBS is the second largest fixed-income security behind U.S. Treasury securities.

The prepayment option attached to the underlying mortgages makes MBS distinctive from other bonds. A mortgagee can partially or fully pay off their remaining balance at any time and for any reason. Further, small amounts of principal are paid monthly by mortgagees. These traits make investing in MBS challenging but rewarding.

Adding to MBS complexity, the timing of mortgage prepayments is not solely a function of the level of interest rates. For many reasons, individuals do not refinance mortgages when interest rates suggest they should.

As a result of its unique and less predictable prepayment option, MBS cash flows are markedly different from those of other bonds. When mortgage rates are very low, many mortgagees pay off their loans due to attractive refinancing options. Also, low mortgage rates promote more housing transactions, resulting in early prepayments of mortgages as mortgagees sell their existing houses and pay off their loans. In low-rate environments, the expected life of an MBS is considerably shorter than in a higher-rate environment.

Duration and convexity

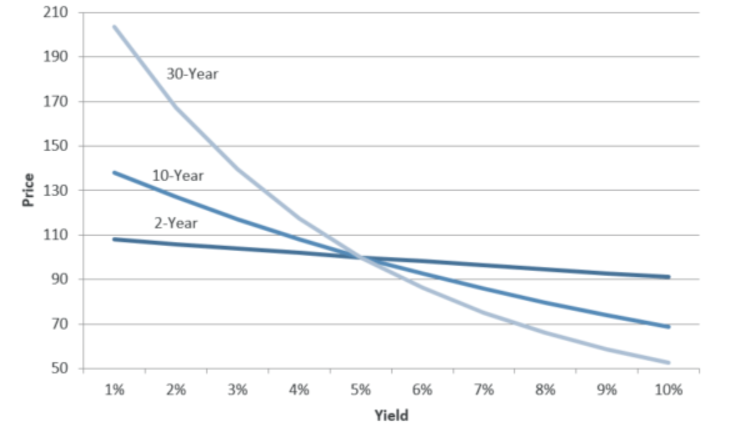

In bond market parlance, the Duration of a bond is a function of how long it will take for an investor to be repaid by a bond's cash flows. Duration is also a measure of the sensitivity of the bond's price to changes in its yield. For example, a duration of 5 means that if yields rise by 1%, the bond price will fall by 5%.

The graph below from Raymond James shows how sensitive bond prices are to changes in yields as a bond's duration increases.

The rate of change in the duration of a bond is not linear. In other words, as duration changes, the price may fall even more or rise less than one would expect, given its original duration. The nonlinearity of duration for MBS is referred to as “convexity.”

As interest rates decline, MBS prices increase less than a bond without prepayment options because the mortgage's expected maturity becomes shorter. Conversely, when interest rates rise, MBS can decrease in price by a greater amount than non-callable bonds because the mortgage's expected maturity lengthens. Both are examples of negative convexity.

MBS investors

With a basic understanding of MBS duration, convexity, and its unique return structure, let's focus on the most prominent mortgage investors.

The Fed owns $2.7 trillion in MBS, less than a quarter of the $12.2 trillion outstanding MBS. Of the MBS outstanding to the public, Fannie Mae and Freddie Mac (the GSEs) and commercial banks hold most of the remainder.

The GSEs and banks borrow money to acquire MBS. As such, they must constantly hedge to avoid material mismatches between the mortgage asset and the loan liability.

For example, if a bank buys an MBS with a duration of five and funds it by issuing a five-year CD, it is duration neutral. As long as the duration remains five, the bank should profit as it initially expected by the yield differential between the MBS and the CD.

Unfortunately for our bank, yields are always changing. Therefore, duration is constantly shifting. For instance, if yields rise appreciably, the duration of an MBS will increase, but the CD will still have a five-year duration that will shorten predictably as time passes. In this case, the MBS investor has a duration mismatch. The mortgage price will fall more than the theoretical price of the CD. In this case, the MBS investor will lose money because of the mismatch. Given the nature of leverage, the gains or losses are much larger than the difference between the MBS yield and the rate of the CD.

MBS investors use interest rate swaps, shorting U.S. Treasury bonds/futures, and options to manage duration. These instruments effectively adjust the duration of the mortgage. The critical point is that these instruments ultimately result in the selling of U.S. Treasury securities when the duration of mortgages extends and buying of them when it declines.

MBS investors this year

As mortgage rates shot up by 4% over the last year, Banks and the GSEs were forced to aggressively hedge their rapidly widening duration mismatches. They shorted U.S. Treasury bonds, directly and indirectly, fueling the higher yield surge. MBS legend Harley Bassman refers to this type of feedback loop as a convexity vortex. Essentially, increasing hedging needs drive yields higher which begets more hedging and higher yields.

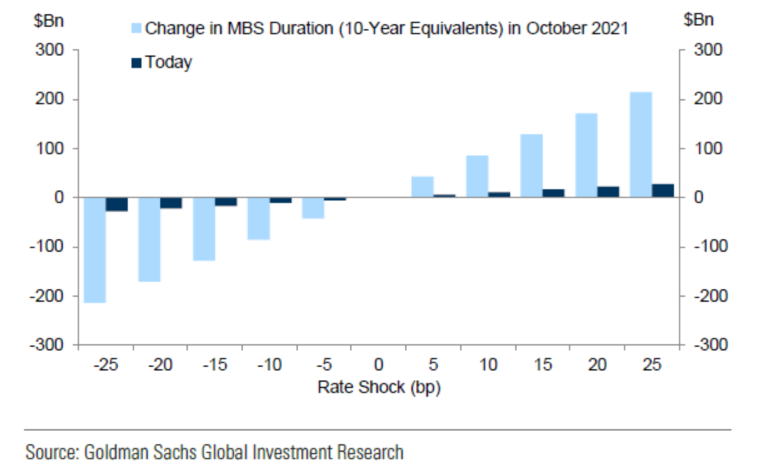

Mortgages durations are maxed out

With an explanation of a critical factor behind this year's bond rout, here is a silver lining.

Almost no one is refinancing mortgages at today's prevailing mortgage rates. Further, the number of home sales is falling rapidly. As a result, MBS prepayments are minimal, and MBS durations are extended. Even if yields continue upward, MBS durations should only trickle higher. As a result, the hedging needs for banks and GSEs to protect against higher durations will be minimal.

The graph above estimates how much in 10-year Treasury notes an MBS investor would need to hedge with versus a year ago. Per Goldman Sachs, a year ago, a .25% increase in yields required banks and GSEs to conduct approximately $200 billion worth of hedging activity (shorting bonds). Today, a .25% move requires about a tenth of that amount.

Institutional mortgage investors are no longer the bond market's problem. Importantly, when yields decline, they will need to exit their hedges. Ultimately, those collective actions will help push yields lower reversing the recent abrupt rise in yields.

Summary

MBS hedgers are certainly not the only investors to blame for the recent sharp increase in yields. But they are a large and known commodity.

Bond yields may keep rising, but a significant influencer of yields is done selling. Further, if and when bond yields start falling, these same investors will need to hedge in the opposite direction. MBS vortexes work both ways. Soon, MBS hedgers may be tripping over each other to buy bonds.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com.

Contact him at [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. The prepayment option attached to the underlying mortgages makes MBS distinctive from other bonds. A mortgagee can partially or fully pay off their remaining balance at any time and for any reason. Further, small amounts of principal are paid monthly by mortgagees. These traits make investing in MBS challenging but rewarding.

The prepayment option attached to the underlying mortgages makes MBS distinctive from other bonds. A mortgagee can partially or fully pay off their remaining balance at any time and for any reason. Further, small amounts of principal are paid monthly by mortgagees. These traits make investing in MBS challenging but rewarding. The rate of change in the duration of a bond is not linear. In other words, as duration changes, the price may fall even more or rise less than one would expect, given its original duration. The nonlinearity of duration for MBS is referred to as “convexity.”

The rate of change in the duration of a bond is not linear. In other words, as duration changes, the price may fall even more or rise less than one would expect, given its original duration. The nonlinearity of duration for MBS is referred to as “convexity.” Mortgages durations are maxed out

Mortgages durations are maxed out The graph above estimates how much in 10-year Treasury notes an MBS investor would need to hedge with versus a year ago. Per Goldman Sachs, a year ago, a .25% increase in yields required banks and GSEs to conduct approximately $200 billion worth of hedging activity (shorting bonds). Today, a .25% move requires about a tenth of that amount.

The graph above estimates how much in 10-year Treasury notes an MBS investor would need to hedge with versus a year ago. Per Goldman Sachs, a year ago, a .25% increase in yields required banks and GSEs to conduct approximately $200 billion worth of hedging activity (shorting bonds). Today, a .25% move requires about a tenth of that amount.