Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The big question facing the Fed is whether it should increase the Fed funds rate by 25 or 50 basis points on March 22, 2023. If Jerome Powell cared for my advice, I would tell him to take the opposite approach of President Theodore Roosevelt. Speak loudly because your stick isn't that big anymore.

President Roosevelt's "big stick diplomacy" defined his foreign policy leadership style. He believed that the U.S. should negotiate with allies and foes peacefully (softly) but make it well understood that the U.S. was prepared to strike hard (big stick) if need be.

Having raised rates by over 4% over a short period and in a very leveraged economy, the Fed no longer has the big stick it used to have. Therefore, speaking loudly with hawkish rhetoric and narrative must become a priority.

Current monetary policy stance

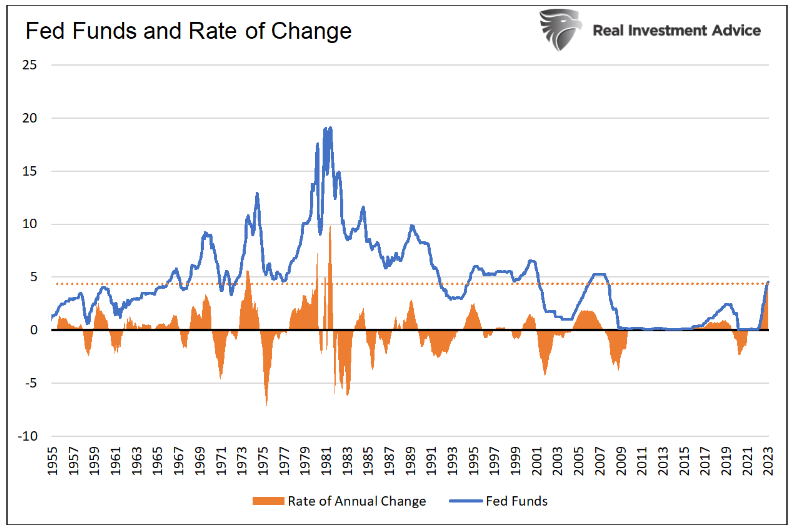

For the last year, the Fed has used its interest rate stick to thump the economy and tame inflation. Its actions were more aggressive than any we have seen in over 40 years, yet have thus far proven futile in reducing inflation.

The graph below shows Fed funds (blue) and the 12-month rate of change in Fed funds (orange). The orange dotted line shows that the current 12-month rate of change in Fed funds is double that of any period since 1981.

Fed funds are at 4.50% and expected to climb to 5.25% in the coming months.

Despite the forceful interest rate hikes, the unemployment rate is at 50-year lows, and GDP is trending above the natural growth rate. CPI appears to have peaked, but recent inflation indicators warn it may be sticky at levels higher than the Fed wants. While the economy may seem robust and inflation too high, both can change quickly as the high deficit (the “leverage tax”) exerts itself.

The leverage tax

I use the term leverage tax to describe the cost of interest expense on the economy. To better comprehend it, think about buying a car on loan. The initial purchase will boost your consumption significantly. Yet the monthly loan payment reduces the goods and services you can consume until the loan is retired, your income increases, or you can refinance at a lower interest rate. The loan impedes your ability to spend.

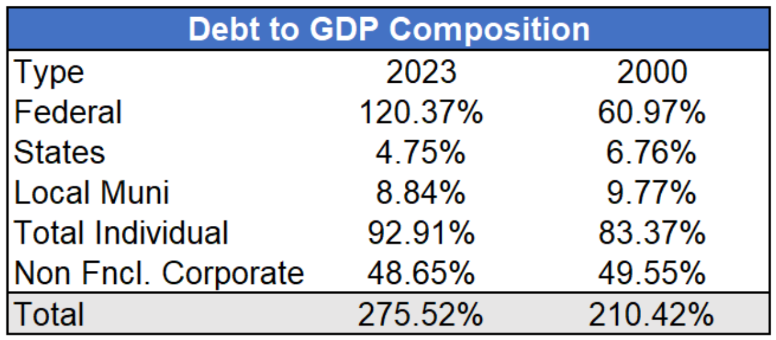

From a macroeconomic perspective, the leverage tax is a function of the total amount of debt in the system, the debt's interest rate, and GDP. The table below compares the current amount of system-wide leverage versus 2000.

As it shows, the amount of debt today has risen to 2.75 times that of the size of the economy, having grown significantly over the last 20 years. While there is more debt as a percentage of GDP, the leverage tax did not increase nearly as much.

Since 2000, total debt has risen 264%, yet the interest expense on the debt is only up 40%. Such is the magic of declining interest rates.

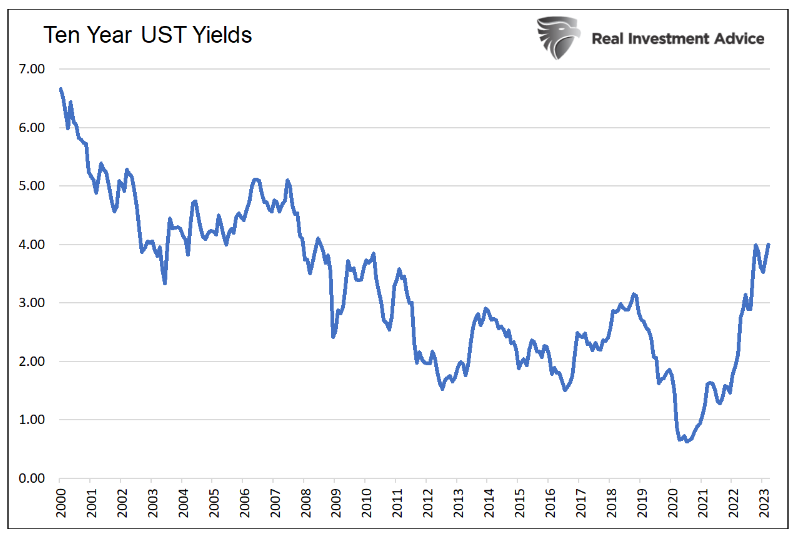

As shown below, interest rates have fallen significantly since 2000. More debt drove economic activity but, on the margin, did not increase the future financial burden significantly.

Interest rate magic no more

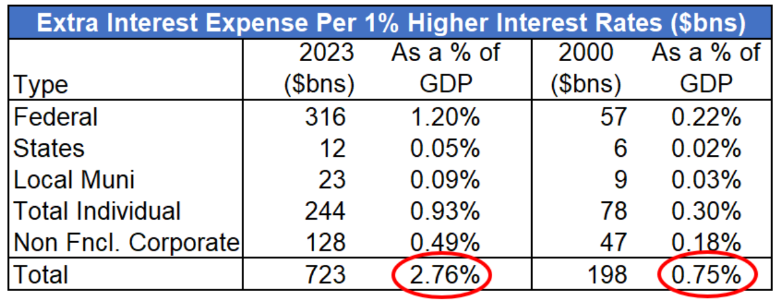

Interest rates are now rising rapidly, and the leverage tax will follow. To help quantify the increasing burden, I share the table below.

The table estimates what each 1% increase in interest rate costs the economy as a percentage of GDP. Before panicking, realize that most of the debt has a fixed interest rate, so it will take a while to reset at higher levels.

I used the five-year Treasury as a proxy for interest rates to approximate how higher interest rates will dampen the economy over time. The five-year note currently yields 4.25%, about 2.50% above its 1.75% average of the last 12 years. Most maturing debt was added when interest rates were below 2%.

If only 20% of debt matures this year and is rolled over, the additional interest cost could be equivalent to 1.38% of GDP. The percentage will continue to increase as more debt matures and gets reissued at higher rates.

The process whereby higher interest rates slowly but increasingly weaken the economy is known as the lag effect.

HOPE and the lag effect

In Janet Yellen Should Focus On Hope, I employed the HOPE framework to show how higher interest rates take time to ripple through the economy.

Per the article:

The Fed first hiked rates on March 17, 2022, by .25%. Assuming it takes a year or longer for the full impacts of a rate hike to be experienced, the first, relatively small rate hike is not fully being felt. There were seven more after March 2022, accounting for an additional 4.25% of interest rate increases.

Graphing hope

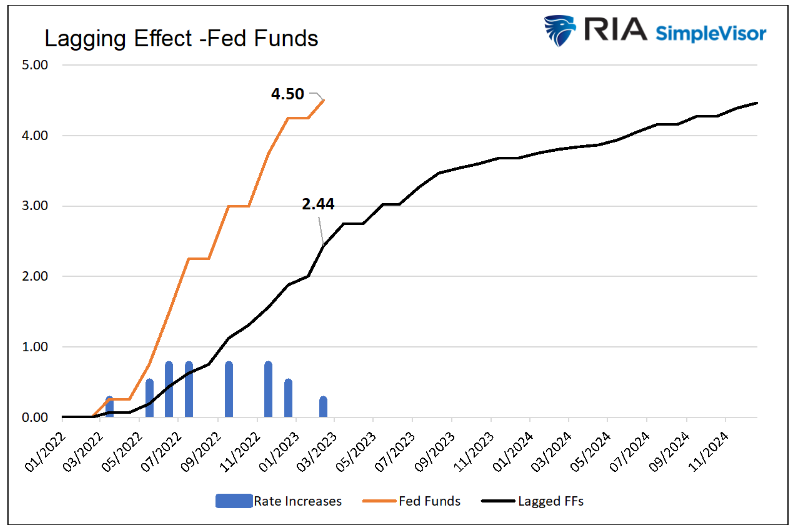

To help quantify the lag effect, I make a few assumptions to visualize when the prior rate hikes fully affect the economy. To do so, I assume the rate hikes affect the economy with the following lags:

- 25% first month

- 50% within three months

- 75% within nine months

- 85% within 15 months

- 100% within two years

The lags assumptions are estimates and likely conservative. The point is not to quantify the impossible but to raise awareness that interest rate hikes aren't effective immediately. As the graph below shows, the Fed funds rate as of mid-March is 4.50%, yet the lagged-effective Fed Funds rate is likely about 2% less.

Time for the Fed to manage financial conditions

The Fed has already raised Fed funds significantly. But as far as economic activity is concerned, it is as if the Fed only did about half of what it did. The lagged Fed funds rate is rising rapidly and will increasingly tax the economy significantly.

Does Powell want to increase the tax on tomorrow's economy further or wait for previous rate hikes to take full effect?

As we think about the question, remember that the amount of leverage in the system is significant and that higher rates risk the potential for serious financial difficulties. Therefore, Jerome Powell should aim to stop inflation with weaker "financial conditions" as his Fed funds stick becomes increasingly dangerous to swing.

Financial markets are a vital way monetary policy is transmitted to the broader economy. As such, higher stock prices, which Powell describes as "an unwarranted easing of financial conditions" driven by a dovish Fed will further incite inflation, forcing the Fed to stay aggressive.

If Jerome Powell and the Fed can maintain a very hawkish tone and threaten higher rates for longer, the stock market may weaken and tighten financial conditions. Speaking loudly and hawkishly would help the Fed's effort to tame inflation without further risking financial and economic catastrophe.

Summary

The path ahead is fraught with risk for the Fed. On the one hand, it risks not doing enough regarding the actual policy to normalize inflation. On the other hand, it could raise rates too much and create a financial crisis.

Given the lag effect of prior rate hikes and the massive leverage embedded in the economy, I advise Powell to speak very loudly but take limited further action regarding rate hikes. If Powell takes my advice, the stock market could return to last October's lows or even lower. Regardless of whether such activity is taken, talk of more quantitative tightening (QT) and higher Fed funds will scare investors.

Putting ourselves in Powell's seat and weighing the decisions he has to make is one way to appreciate better what the future may hold.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. Fed funds are at 4.50% and expected to climb to 5.25% in the coming months.

Fed funds are at 4.50% and expected to climb to 5.25% in the coming months. As it shows, the amount of debt today has risen to 2.75 times that of the size of the economy, having grown significantly over the last 20 years. While there is more debt as a percentage of GDP, the leverage tax did not increase nearly as much.

As it shows, the amount of debt today has risen to 2.75 times that of the size of the economy, having grown significantly over the last 20 years. While there is more debt as a percentage of GDP, the leverage tax did not increase nearly as much. Interest rate magic no more

Interest rate magic no more The table estimates what each 1% increase in interest rate costs the economy as a percentage of GDP. Before panicking, realize that most of the debt has a fixed interest rate, so it will take a while to reset at higher levels.

The table estimates what each 1% increase in interest rate costs the economy as a percentage of GDP. Before panicking, realize that most of the debt has a fixed interest rate, so it will take a while to reset at higher levels. Time for the Fed to manage financial conditions

Time for the Fed to manage financial conditions