Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

With Silicon Valley Bank and Credit Suisse defunct, the Fed must restore confidence in the financial sector. The historical treatment for financial instability has been lower interest rates and more liquidity. The problem, however, is that the Fed is simultaneously trying to reduce inflation. The Fed must orchestrate higher interest rates and less liquidity to tame inflation.

Welcome to the paradox it faces in phase two of the Fed follies.

During phase one of the Fed's tightening campaign, it raised the Fed funds rate at almost double the pace in the previous 40 years. Furthermore, it is reducing its balance sheet by nearly $100 billion a month via quantitative tightening (QT). To the Fed's chagrin, high inflation is proving hard to conquer because economic activity remains brisk, and unemployment sits near 50-year lows. Fighting inflation requires tight monetary policy to weaken economic demand.

Phase two, unlike phase one, introduces financial instability. This inconvenient crisis drags the Fed in opposing directions. Lower interest rates and more liquidity are the keys to boosting confidence in the financial sector, but they impede the Fed's ability to fight inflation.

Fed mandates

Per the San Francisco Fed: "Congress has given the Fed two coequal goals for monetary policy: first, maximum employment; and second, stable prices, meaning low, stable inflation."

The Fed's Congressional mandates argue it should continue to focus on inflation as the unemployment rate is at historic lows and prices are far from low and stable. Economic activity, which significantly affects employment and prices, is robust.

If the Fed were to follow its mandates strictly, there would be no phase two of the Fed monetary policy. Fed funds would remain "higher for longer" until inflation moderates.

Decades ago, the Fed expanded its boundaries by prescribing a third mandate. The Fed believes it must also maintain a stable financial system to keep the economy's engine, banking, on sound footing.

Phase-zero follies

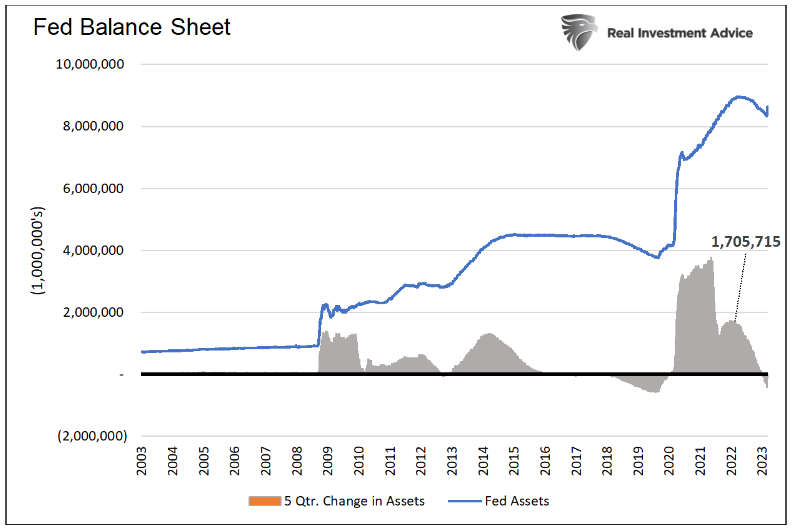

Before phases one and two, there was phase zero. Phase zero, in 2021 and the first quarter of 2022, laid the foundation for today's difficulties. During 2021 and the first quarter of 2022, the Fed kept interest rates at zero and bought over $1.7 trillion of Treasury and mortgage assets.

As shown below, the Fed added $1.7 trillion of assets between January 2021 and March 2022. That increase was more than any other five-quarter period during the financial crisis in 2008/2009. Despite rapid economic growth and wild market speculation, the Fed was turbocharging the economic engines to a degree never seen before.

The Fed was aggressive despite inflation rising from 1.4% in January 2021 to 5.28% in just six months. Inflation was running at 8.5% before it decided to do something about it. Further, inflation expectations implied by markets and forecasted by the Cleveland Fed were increasing rapidly.

Had the Fed realized supply lines were crippled and demand for goods and services was fueled by one of the most extraordinary doses of fiscal stimulus, it would have easily recognized inflation was a problem. It didn't, and its folly results in sticky levels of high inflation today.

Furthermore, had it started raising rates and curtailed quantitative easing (QE) in early 2021, not only would the inflationary pressures lessened, but stock and crypto speculation would not have formed the bubbles they did. Lastly, pertinent to the banking crisis, a more restrictive policy would have kept interest rates lower as the confidence in the Fed's ability to manage inflation would have been greater.

As a reminder, the current banking crisis is due to depositors fleeing banks for higher money market rates and banks carrying losses on their loans and securities due to higher interest rates. The banks are at fault for inadequate hedging and keeping deposit rates too low, but the Fed made their bed.

Phase one

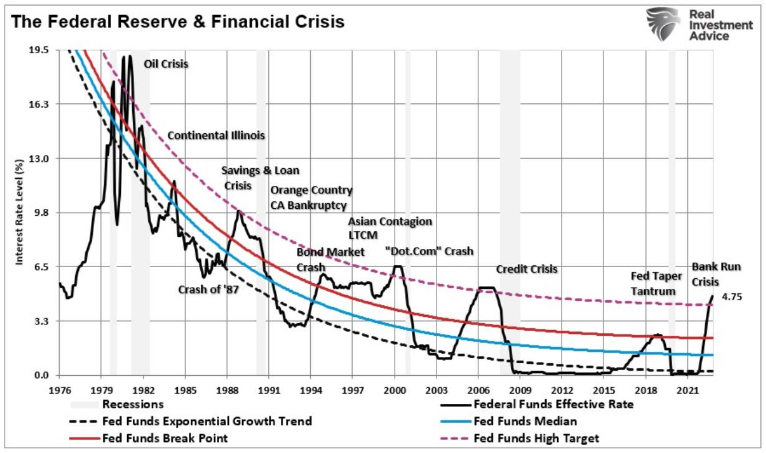

A little more than a year ago, the Fed started raising rates. Nine months ago, it gradually began reducing its balance sheet. Unfortunately, both actions were about a year too late. As such, it had to be more aggressive than it would have otherwise been.

Over the last year, I warned that the Fed would raise rates until something breaks. As labeled below, soaring interest rates are breaking the banks.

The transition from phase one to phase two

In Speak Loudly Because You Carry a Small Stick, I gave Jerome Powell my two cents on monetary policy. Speak more hawkish and put fear into the markets. Let the markets and banks tighten financial conditions and lending standards and therefore avoid raising rates too much.

Little did I know that hours after publishing my article, Silicon Valley Bank would fail and drag the global banking sector down. Jerome Powell's stick is now much smaller as the odds of a financial crisis are considerable.

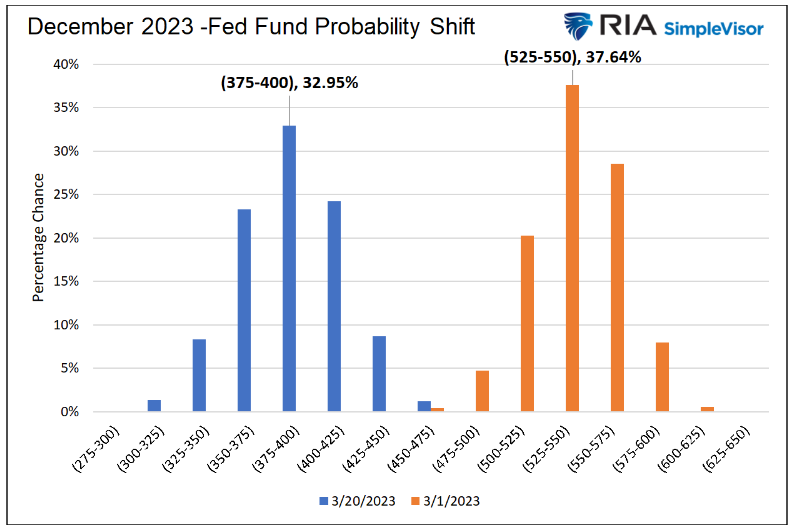

As I share below, the Fed funds futures market sniffed out the Fed was up against a new opponent. On March 1, the market implied a 37% chance Fed funds would end the year between 5.25-5.50%. Some traders bet Fed funds could be 6% or more. Only 20 days later, the market thinks Fed funds may end up below 4% by year-end.

Phase two

Phase two is the delicate balance of inflation and financial stability. The Fed must maintain credibility that its determination to fight inflation is still strong. But it must also convince the market it will provide ample liquidity to restore confidence in the banking system.

Maintaining a balance between such opposing objectives is fraught with risk.

If the Fed leans too much toward financial stability, the reignition of inflation fears may scare markets. In such a case, bond yields and commodity prices will rise and further inflame the banking crisis. It will also require the Fed to take more action to stamp out inflation.

Conversely, the banking crisis can quickly spread if the Fed does not provide enough liquidity because it worries too much about inflation.

Tightening lending standards = Recession

As if balancing two opposing forces weren't complicated enough, recent bank events significantly increase the odds of a recession. Following the events of the last week, banks have no choice but to bolster their balance sheets. Consequently, they will tighten loan standards, making borrowing harder and more expensive.

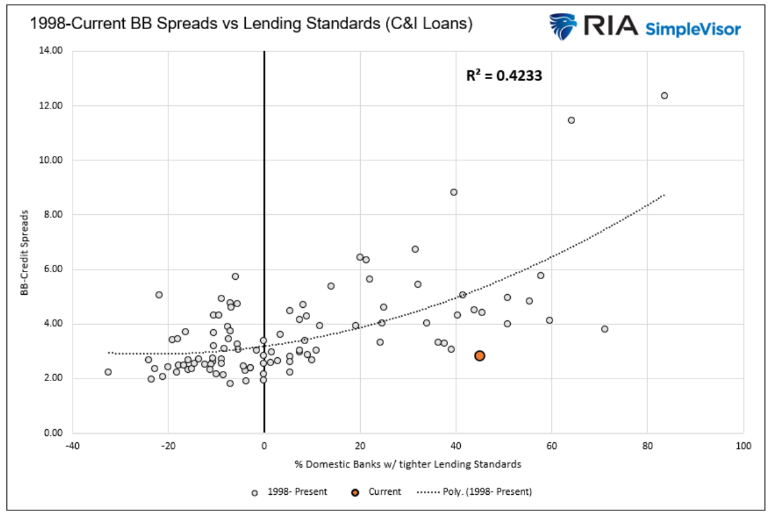

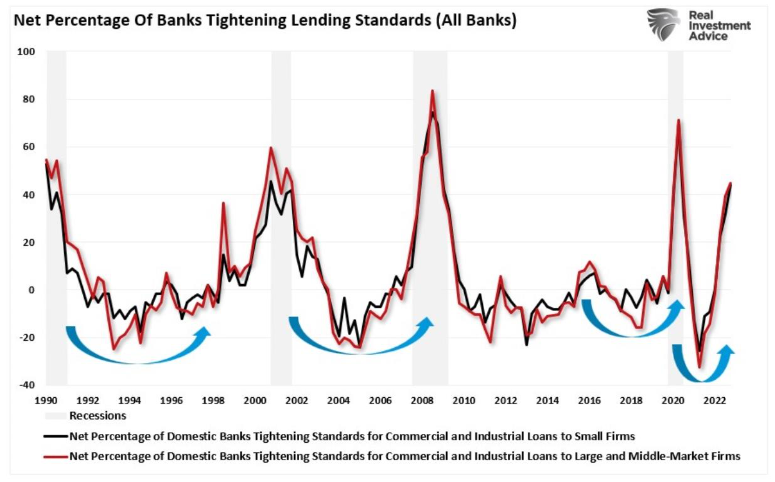

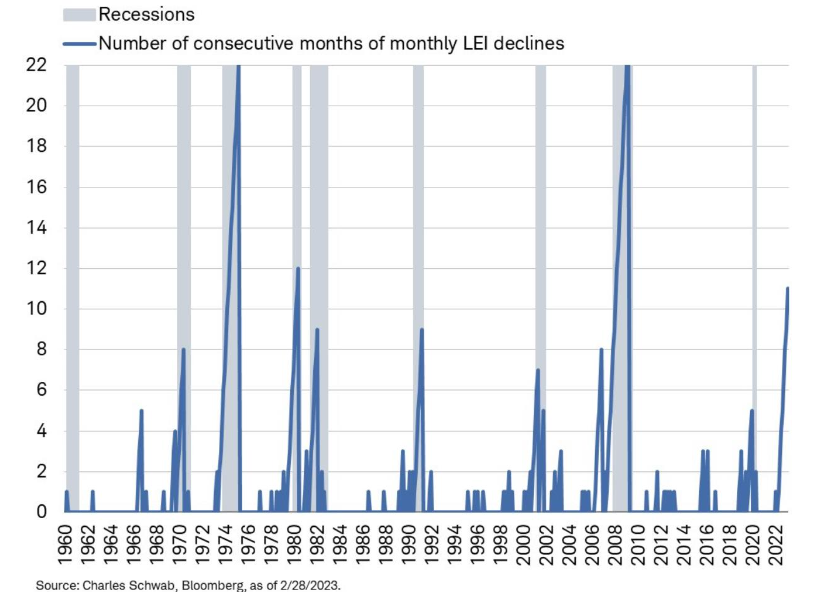

The first graph below shows the strong correlation between tightening standards and corporate high-yield bond spreads. High-yield bond spreads are a good proxy for bank loans. Based on the scatterplot, a 2.5% increase in corporate bond spreads is likely. Further, the estimate may be understated as lending standards have yet to reflect recent events. The following graph highlights the robust relationship between tighter lending standards and recessions. The third graph shows that leading economic indicators (LEIs) have declined for 11 straight months, never seen before without the economy being in or heading into a recession.

Summary

In the long run, stocks are fraught with risk.

If the Fed provides liquidity and restores confidence in banking, inflation fears will resurrect the "higher for longer" policy. As we saw last year, such policy accompanied higher bond yields and lower stock prices.

If the Fed is not supportive enough of the banking sector with lower rates and liquidity, the banking crisis can quickly get out of hand. A waterfall in stock prices and much lower bond yields can quickly occur if they lose control of the crisis narrative.

Of course, there is a probability the Fed succeeds in this delicate task and tackles inflation while avoiding deepening the banking crisis. Even in that preferred case, the economy must still grapple with tighter financial standards resulting from the banking crisis. A recession, lower corporate earnings, and weaker stock prices are likely in that situation. Bond yields will likely decline in an economic downturn as inflationary pressures lessen.

Stocks may rally in the coming weeks or months as it appears the banking crisis is over, and the Fed is set to pause and pivot. But beware, this may be the calm before the recession.

Following your trading rules will prove very important as the year progresses.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. The Fed was aggressive despite inflation rising from 1.4% in January 2021 to 5.28% in just six months. Inflation was running at 8.5% before it decided to do something about it. Further, inflation expectations implied by markets and forecasted by the Cleveland Fed were increasing rapidly.

The Fed was aggressive despite inflation rising from 1.4% in January 2021 to 5.28% in just six months. Inflation was running at 8.5% before it decided to do something about it. Further, inflation expectations implied by markets and forecasted by the Cleveland Fed were increasing rapidly. The transition from phase one to phase two

The transition from phase one to phase two