All dollars are not created equally; some are worth more than others. Why? Because some money can be used without incurring taxes, while other money must be taxed at either capital gains or ordinary income rates.

All dollars are not created equally; some are worth more than others. Why? Because some money can be used without incurring taxes, while other money must be taxed at either capital gains or ordinary income rates.

One of the toughest dilemmas I wrestle with is whether to consider future tax liabilities from unrealized gains in the portfolio and taxes from withdrawing from traditional retirement accounts. It’s a very important issue for which there has been little media coverage.

To put it concisely, Roth dollars are the client’s most valuable money, followed by taxable money, with traditional tax-deferred dollars being the least valuable.

The simple example

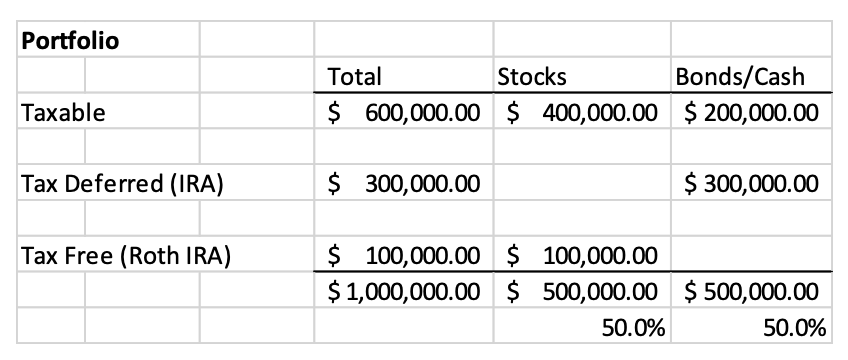

Let’s take a simple example of a $1 million portfolio.

This client’s asset location appropriately minimizes taxes. The 50% allocation to stocks was their target. But all this money isn’t theirs. Assume the tax-deferred money has a zero basis and the taxable portfolio has a $100,000 long-term gain. Further, say the client is in the 37% ordinary-income marginal tax bracket (state and federal) and the 20% long-term capital-gains rate.

The tax-deferred account would be taxed at 37%, and the client would have to pay $20,000 in capital gains taxes if they sold the stocks.

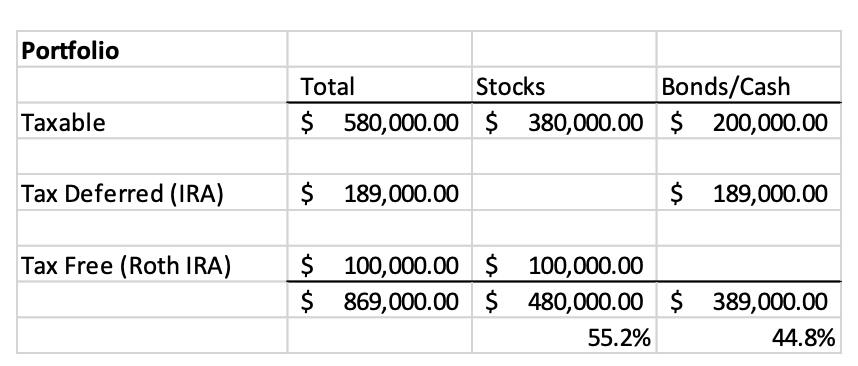

In this simple case, the client has a portfolio that is really only worth $869,000 with just over 55% in stocks, or five percentage points over their desired 50% stock allocation.

To get back to their target 50% stock example, they would need to sell $45,000 of stocks and move to bonds either in their taxable or Roth account.

Introducing real-world complexities

Unfortunately, neither taxes nor portfolios are as simple as the one I’ve just described. As far as taxes go, there are many unknowns, such as:

Tax complexities

- How much lower will their ordinary income tax bracket be in retirement? Perhaps they can be in the 17% bracket.

- Could they be in the zero-percent long-term capital gains tax-bracket? It’s currently at least $116,950 for married filing jointly, though 5% state taxes would apply in this example. (The zero percent long-term capital gains bracket goes to $89,250, plus at least the standard deduction of $27,700).

- What changes will Congress make to tax rates? Should we put in a reserve for possible rate increases?

- What if income tax is replaced by a consumption tax, such as the fair-tax act?

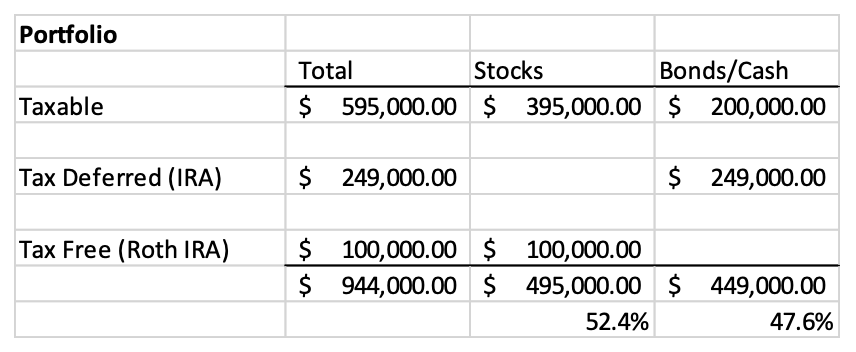

After adjusting to the 17% ordinary-income tax bracket and 5% long-term capital-gains bracket, the situation changes yet again. Now the client has a $944,000 portfolio that is only 2.4 percentage points from target.

Next, we take into account the underlying investments in the accounts. Are all gains in the taxable account long-term? Do some of the holdings not qualify for long-term capital gains? Will the 3.8% investment income tax come into play? What if the taxable portfolio has an unrealized loss?

In looking at the tax-deferred account, did the client make some after-tax contributions to their traditional IRA? Would there be a penalty if they withdrew from their Roth account either because they aren’t 59.5 years old or haven’t had the account for five years? In fact, the tax-deferred account would be subject to the 10% penalty unless they took a 72(t) election of substantially equal payments.

Often the client has dozens or even hundreds of holdings in their taxable account. I’ve recently gone through a client’s portfolio and tax-adjusted each security. It was more precise.

Where I come out on the issue

These adjustments are more accurate, though the complexities make the results confusing and difficult to understand. But this doesn’t mean I ignore the issue.

I advise clients that the Roth is the most valuable money, as it will never be taxed again – and always put in the disclaimer “under current law.” It would typically be the last money they would ever want to spend.

I also explain that the traditional tax-deferred money is their least valuable money, as it’s a partnership between the client and the state and federal governments. They will have to buy the governments’ share out before they can use it.

I look at the future taxes from unrealized gains and apply safe withdrawal rates to look at withdrawals after taxes. In this million-dollar portfolio example, using a 3.5% safe withdrawal rate adjusted each year for inflation, the $35,000 annual real withdrawal includes the tax consequences.

As with many things in life, theory and reality often clash. In theory, we should be using some estimate to tax-adjust client holdings. Doing so makes it more precise. The reality, however, makes it precisely useless to the client.

While my advice is to not ignore the issue of future tax liabilities from the portfolio, it comes with the caveat that this should be done without creating complexities that imply false precision. It will create a work of art no one can understand.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

All dollars are not created equally; some are worth more than others. Why? Because some money can be used without incurring taxes, while other money must be taxed at either capital gains or ordinary income rates.

All dollars are not created equally; some are worth more than others. Why? Because some money can be used without incurring taxes, while other money must be taxed at either capital gains or ordinary income rates.