Gundlach: Buy Bonds, Not Stocks

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits There is plenty of opportunity in the bond market, particularly in low-risk Treasury bonds and in the mortgage markets, according to Jeffrey Gundlach. A year ago, stocks were cheap; now, he said, “Bonds are absolutely cheap relative to stocks.”

There is plenty of opportunity in the bond market, particularly in low-risk Treasury bonds and in the mortgage markets, according to Jeffrey Gundlach. A year ago, stocks were cheap; now, he said, “Bonds are absolutely cheap relative to stocks.”

“Owning bonds is better than white-knuckling it in stocks in an economy that is going into a recession,” Gundlach said.

Gundlach spoke to investors via a webcast, which he titled “Dust in the Crevices,” and the focus was on his flagship total-return fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

The title was from Gundlach’s hobby as an art collector. He said he was inquiring about a 110-year-old sculpture and was told it had “dust in the crevices,” which is normal for a piece of art that old. But he realized the same is true of our financial system in the context of the debt-ceiling debate. The debt ceiling has been raised 99 times since 1913. “This debt-ceiling thing is pretty dusty,” he said, “as is our method of getting past it.”

Gundlach said inflation is “in retreat,” and that removes the biggest obstacle to lower yields.

“This why bond yields have stopped going up,” he said. The 10-year Treasury cannot get to 4% and stay there.

He has recommended long-duration bonds since last October. It is safe to own longer term bonds, Gundlach said. There will be a rally, at least initially, in longer term bonds if there is a recession.

Gundlach has increased the duration on DBLTX to its highest level ever.

“We have seen the peak in interest rates in this cycle,” he said.

Ongoing fiscal woes

The debt-ceiling saga is one byproduct of the growing federal deficit. As he has in the past, Gundlach railed against the rise in government debt.

“We have abandoned fiscal rectitude and the deficit is climbing quickly,” he said. This will be particularly problematic if there is a recession. “We are already at levels that should be scary based on past recessions,” Gundlach said, adding that the probability of a recession is going up.

“Politicians need to admit that they need to address the deficit in the next few years, not 10 years from now,” he said. Historically deficits rose because of world wars and events of that magnitude. But now, he said, there hasn’t been a balanced budget in his lifetime, which is 64 years.

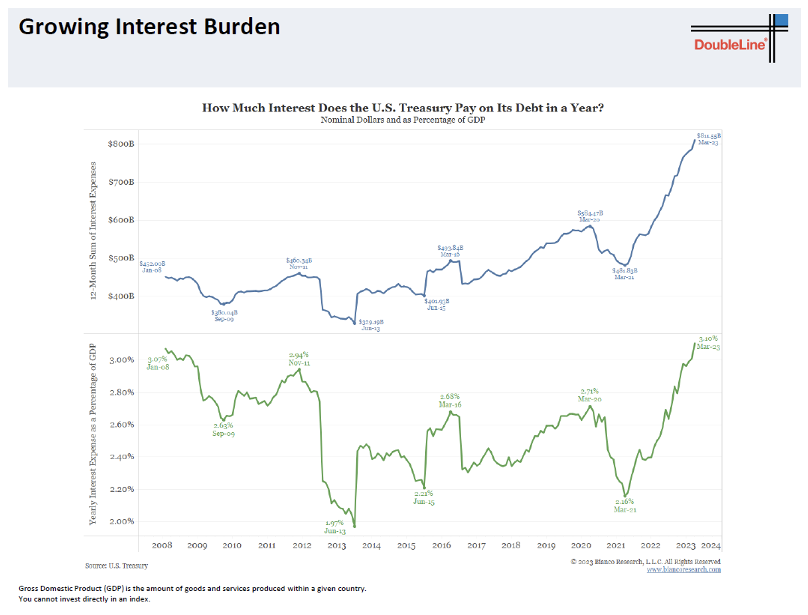

The real kicker is the growth in interest paid on the deficit, as he showed in the graph below.

The amount of interest paid was fine when rates were near zero, he said. But now the deficit is increasing, and the Fed has been raising rates. This caused the rancor in the debt-ceiling talks, he said, and “the deficits will swallow all tax increases in the next few years.”

“We have to raise taxes or restructure entitlement programs,” he said.

“If you look closely into the crevices of our financial system, there is a lot of dust,” he said. “It will be a focus of the 2024 presidential campaign.”

How likely is a recession?

Gundlach cited many economic indicators, some of which indicated a recession is imminent. Others did not.

The leading economic indicators (LEIs) are “absolutely full-on recessionary,” he said. Their momentum has gotten worse over the last six months, he said, meaning that soon we will be at the front end of a recession.

Consumer expectations are getting “really, really bad” relative to the future, although relative to the present they are not. “The conditions for a recession are ripe,” he said.

The yield curve, based on the two- to 10-year spread, has de-inverted about eight to 13 weeks before a recession historically. It has started to de-invert, he said, “but not by much.” If short rates start falling, it will be recessionary. “This puts us close to a recession,” he said.

The ISM new orders indicator “looks very recessionary already,” as does the PMI. “The manufacturing economy is already in a recession,” Gundlach said.

Loan-officer lending-survey data shows that lending standards historically tighten going into a recession. It is suggestive that the economy will be in a recession within a year, according to Gundlach. Loan growth is contracting, and he said it is already a problem for economic growth.

“If the unemployment rate rises in any meaningful way,” he said, “it will signal a recession. Right now, it is close to indicating a recession.”

He showed consumer survey data that asked people whether they were better or worse off than a year ago. Since 2018, the percentage who said they are worse off has gone from 13% to 35%. Those were the worst readings in the last nine years.

He also showed data indicating that middle-management jobs are decreasing, which he said are “getting hollowed out” due to artificial intelligence and other technological advances. “Higher income people are starting to feel the pain of the situation,” he said.

Gundlach said that the Bloomberg office-product index has “collapsed” and is at a new low. Bank failures as a percentage of GDP are at levels similar to the Depression and the global financial crisis.

The problem facing banks is that their portfolios aren’t throwing off enough money, and they can’t afford to pay depositors enough. “If the Fed raises,” he said, “there will be further problems in the banking system.”

There are already massive unrealized losses in the banking system, according to Gundlach. Banks must own long-term debt. Contrary to what many pundits claim, he said they can’t hedge that risk. “If you want the income,” he said, “you cannot hedge.” If the Fed hikes rates, he said it could lead to “further dust ups” in the banking system.

Inflation is receding

Gundlach said that inflationary pressures are subsiding, and that will accelerate if there is a recession.

Money supply growth is the most negative since the Depression, he said, which is not inflationary. “That contraction takes the pressure off inflation,” he said. “When M2 declines, inflation relaxes, and vice versa.”

Headline CPI is 4.9%, and it should come down. But core inflation is 5.5%, which he said is “sticky.”

Inflation has been elevated over the last two years, he said, but it is not being stoked by money supply growth.

The Fed would be satisfied if inflation declined to 3%, according to Gundlach.

“The CPI will certainly fall if there is a recession,” he said, “but it depends on the shape of a recession.”

Services and food are the big contributors to headline inflation. Energy is deflationary, with oil stuck at approximately $70/barrel.

Wholesaler price increases are 2.3%, and those historically lead the CPI, which signals lower inflation. That increase is at pre-pandemic levels, he said.

Import prices are down -4.4%, and export prices are down -5.5%, which he said are “deflationary levels” at odds with those who are bearish on bonds.

Wage growth is the one metric that is not signaling an end to inflation. It has been sticky at approximately 6%, Gundlach said, except for the middle-management positions that are being lost.

The capital-market outlook

Gundlach doesn’t like commodities because the economy is weakening, and it is heading into a recession. He has been bearish on commodities for almost two years, he said.

Gold, at $1,965, has done well over the last year. But he said he is “less bullish” on it because of technical patterns.

The opportunity is in fixed income.

The Fed made a mistake by waiting a year too long to raise rates, which is why inflation rose and became sticky. It should have raised rates by 200 basis points at the time when it started raising rates. If it had done that, he said, it would have made bank failures less likely.

But the Fed’s actions have driven up rates to very attractive levels.

The copper-gold ratio suggests that 10-year yield should be near 2%.

The yield-to-worst on CCC-rated bank loans is near 19%, but those companies are marginal, and defaults are expected. Some high-yield debt yields more than 13%, but that includes many candidates for defaulting. Defaults start about a year after lending standards tighten, he said, and that began before the SVB crisis.

“Watch out for bank loans,” he said. “There will be defaults, and the recovery rate will be worse than the historical 70% rate. It is already approximately 50%, he said, and it will be worse if there is a recession.

Since 2007, an increasing percentage of new-issue high-yield debt has been secured. That makes it lower risk than during the global financial crisis. Spreads are a little on the “snug side,” however, Gundlach said. “If there is a recession, it will be the unsecured bonds that will be most vulnerable.”

Emerging-market spreads have tightened less than the investment-grade market. They typically widen when the dollar is strong, he said, although that has not happened this year.

Housing prices have not dropped much, which is strange. There is no stress in the residential housing market, meaning there is no default risk in the mortgage market. Mortgage delinquencies are near all-time lows. But mortgage-backed spreads rose rapidly because of fears surrounding SVB and the disposition of mortgages held by banks.

“This could be one of the most attractive times to own agency mortgages,” Gundlach said. “The mortgage market is systematically cheap.”

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All