Second Quarter 2023 Economic and Market Outlook: A Tale of Two Economies

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Many economists have been forecasting a recession for 2023 due to tightening monetary policy. But that recession has not arrived yet, as fiscal policy is still stimulative; real interest rates are not yet restrictive (the nominal yield on Treasury bills remains below nominal GDP growth); the household sector still has significant savings built up during the pandemic, when rates were much lower; corporations extended the maturity of their loans, making them less vulnerable to higher rates; and the dominant service sector is less sensitive to interest rates.

Many economists have been forecasting a recession for 2023 due to tightening monetary policy. But that recession has not arrived yet, as fiscal policy is still stimulative; real interest rates are not yet restrictive (the nominal yield on Treasury bills remains below nominal GDP growth); the household sector still has significant savings built up during the pandemic, when rates were much lower; corporations extended the maturity of their loans, making them less vulnerable to higher rates; and the dominant service sector is less sensitive to interest rates.

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair.” The opening of Charles Dickens’ A Tale of Two Cities is probably the most famous in literature. It also aptly describes the very different states of the two major sectors of the U.S. economy: manufacturing and services.

Despite the Federal Reserve raising interest rates 5%, to a 16-year high of 5.0%-5.25%, since its first hike in the Fed funds rate in March 2022, the economy has defied forecasts of a recession, as employment continues to show strong growth, consumers are spending freely, and the housing market appears to be stabilizing (see section on residential real estate below). While spending on goods has slowed (as has goods price inflation), spending on services, which are less sensitive to interest rates and constitute about 78% of GDP, continues to be strong even as economic growth has slowed. As a result, the rate of increase in prices on services remains well above the Fed’s target.

We have a tale of two economies. I’ll begin by reviewing what is happening in the sectors that are most sensitive to interest rates – sectors where it is “the worst of times.”

Manufacturing

The US ISM Purchasing Managers Index (PMI) is a diffusion index summarizing economic activity in the manufacturing sector in the U.S. The index is based on a survey of manufacturing supply executives conducted by the Institute of Supply Management (ISM). Participants are asked to gauge activity in a number of categories like new orders, inventories and production, and these subindices are then combined to create the PMI. A PMI above 50 indicates an overall expansion of the manufacturing economy, whereas a PMI below 50 signifies it is shrinking. As seen in the table below, the manufacturing sector has been in recession for seven months:

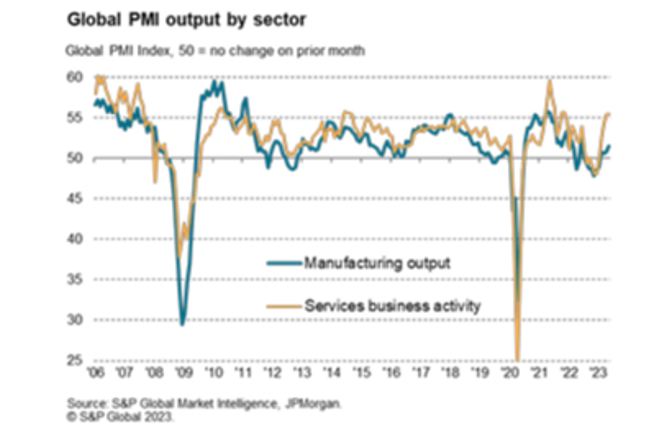

We see the same trends globally. The May 2023 J.P. Morgan Global PMI Composite Output Index, produced by S&P Global, showed that while manufacturing output rose for a fourth straight month in May, the overall rate of growth remained modest. It also showed that new order inflows for goods shrank for an 11th straight month; new export orders for goods fell worldwide at the fastest pace since end of 2022; and the PMI future expectations indices showed that manufacturers’ confidence had sunk to a five-month low and was below the survey’s long-run average. As a result of weak demand, average prices charged for goods leaving the factory gate fell for the first time in three years. That’s good news in the fight against inflation but bad news for corporate profits.

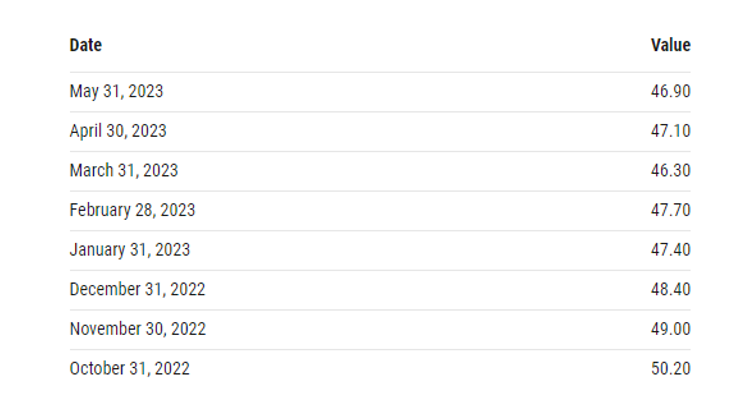

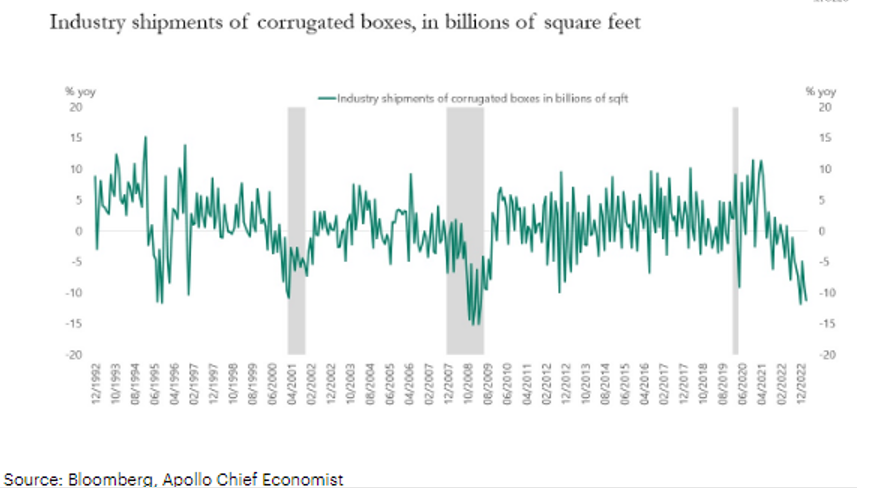

Another sign of weakness in the manufacturing/goods sector is that sales of cardboard boxes have been declining over the past year.

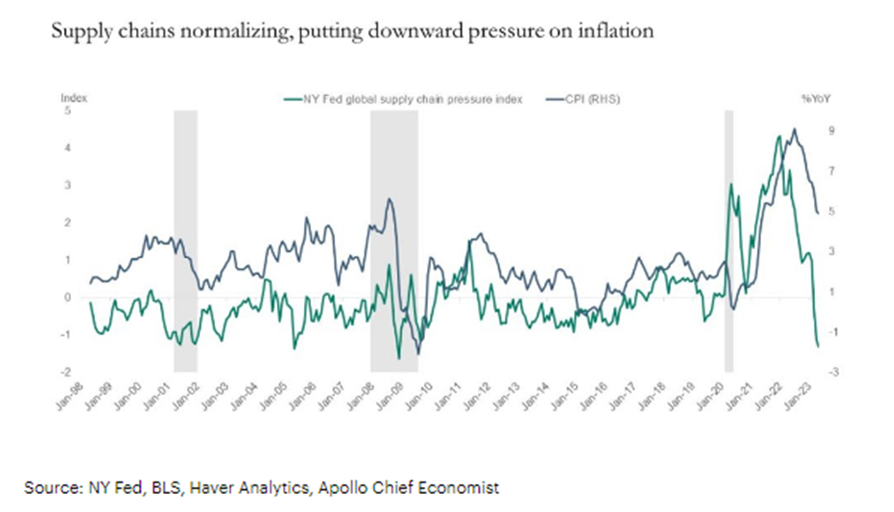

Supply chain problems have eased, helping to reduce goods-price inflation.

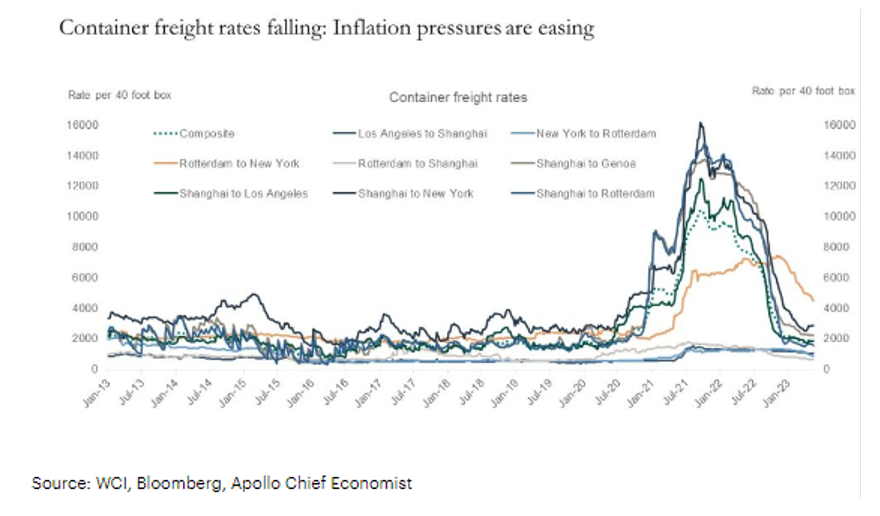

The easing of supply-chain pressures has also led to a sharp drop in container freight rates.

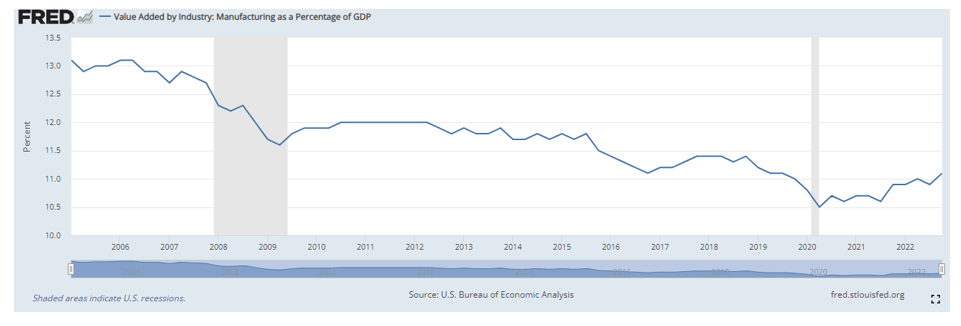

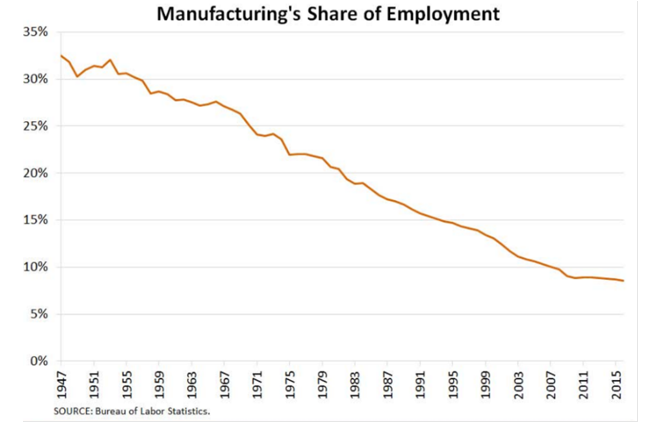

Thanks to the easing of supply-chain pressures and falling shipping costs, goods inflation is trending sharply lower (the bad news is that service-sector inflation, a much larger sector, continues to be elevated). While the manufacturing sector is still an important part of the economy, comprising about 11% of the GDP, as the table below indicates, its contribution to the GDP has been on a long-term decline.

Real estate: Commercial

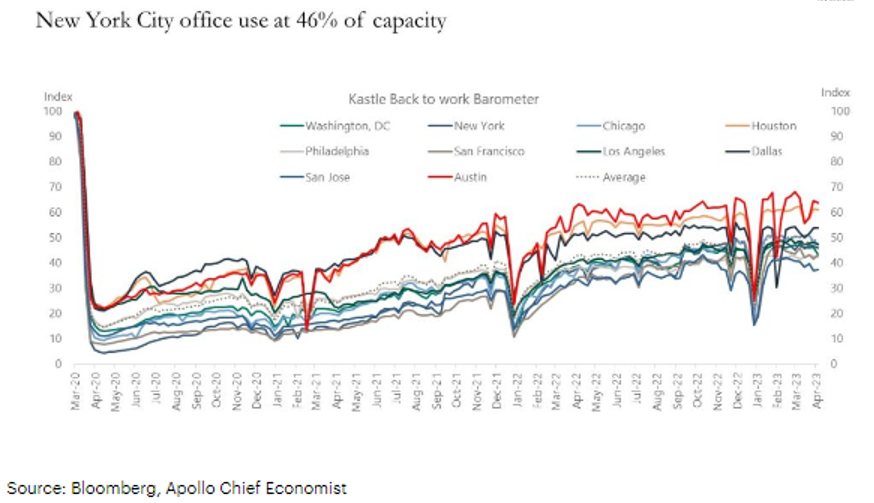

As the chart below demonstrates, the office segment of commercial RE is under considerable stress, with occupancy rates at about 50% on average. With hybrid work models now well established, a 50% occupancy rate may be the new permanent level in many metropolitan areas. In April, the New York City office occupancy rate stood at just 46%. By June 13, it had rebounded to just above 50% – the first time it crossed that level since the pandemic began. Other cities, such as Washington, D.C. and San Francisco, have yet to break the 50% mark.

With almost $1.5 trillion of U.S. commercial real estate debt due for repayment before the end of 2025 and with valuations down sharply, a big question facing borrowers is who will lend to them. And maturities will climb for the coming four years, peaking at $550 billion in 2027. Thus, it seems likely that a wave of defaults will hit commercial real estate loans to office buildings and shopping malls due to rising rates and the shift to working and shopping at home. Office exposure represents about 20% of the aggregate lending by U.S. commercial banks.

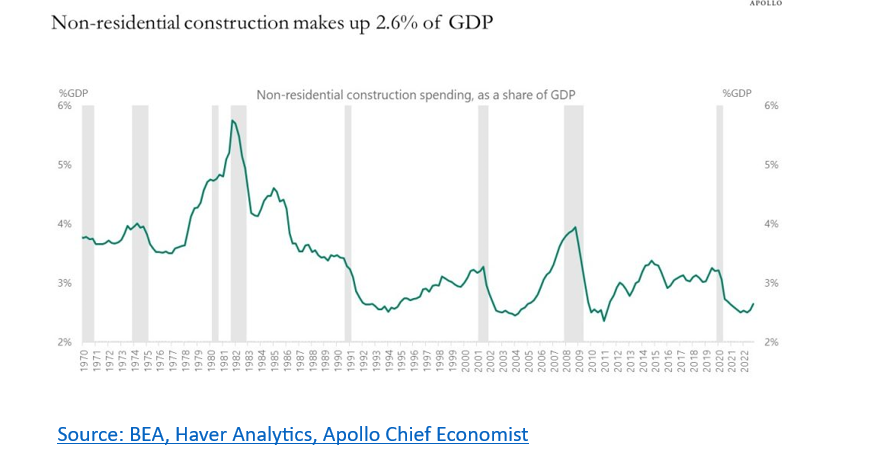

In response to the heightened risks, banks have tightened credit standards, making lending less available and more expensive – both negatives for the economy. Because commercial real estate construction is roughly 2.6% of GDP and fewer skyscrapers and shopping malls are being built, commercial real estate is likely to be a drag on economic growth over the coming years.

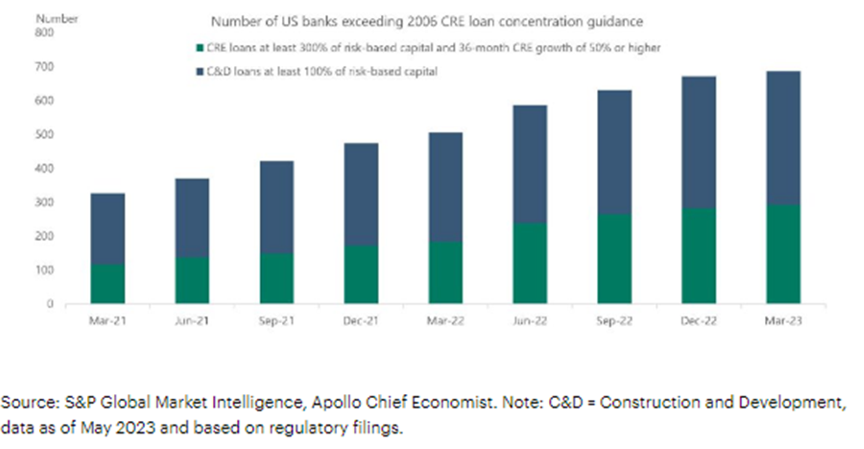

As an indicator of the scope of the problem, two years ago the number of banks exceeding the FDIC’s commercial real estate loan concentration guidelines was about 300. Today, there are almost 700.

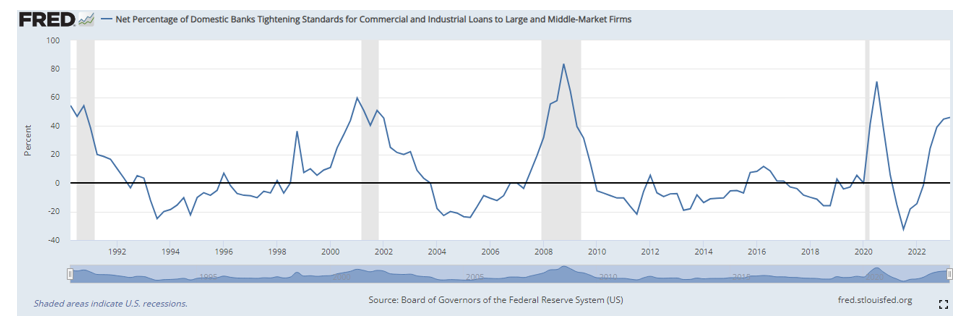

The likely coming wave of defaults along with the concerns raised by the failure of Silicon Valley Bank (SVB was not the only bank to have large losses in its securities portfolios), have led to a significant tightening of credit at banks, as seen in the chart below from the Federal Reserve. Credit is the lubricant that greases the wheels of the economy. Risk aversion by bank lenders means fewer loans and more expensive capital for small and medium businesses. And once this tightening begins, it can become self-fulfilling as workers are laid off and capital expenditures are cut back.

In a 2007 speech titled “The Financial Accelerator and the Credit Channel,” Ben Bernanke noted that financial markets themselves can become the source of macroeconomic volatility due to the withdrawal of liquidity. High volatility – and therefore high uncertainty about credit availability – can have pernicious downstream consequences: “A weak banking system grappling with nonperforming loans and insufficient capital or firms whose creditworthiness has eroded because of high leverage or declining asset values are examples of financial conditions that could undermine growth.” He argued: “Changes in financial conditions may amplify the effects of monetary policy on the economy, the so-called credit channel of monetary-policy transmission.”

Nearly half of banks reported stricter loan standards for small businesses in the previous three months, according to a survey of senior loan officers released by the Federal Reserve Board in May. More than half said they expect to tighten small-business lending standards further in 2023.

Secondary effects

The increase in commercial real estate office vacancies due to working and shopping from home will hit municipal tax revenues hard, as they rely heavily on property taxes. A secondary impact of the shift to working/shopping from home is that revenues at retail stores and restaurants located near offices are falling, as will property values, sales tax revenues and related income tax revenues. Public transportation revenues also have fallen sharply, adding to municipal revenue woes. This will lead to belt-tightening and reduction of services, and a possible negative feedback loop in some major cities. For example, according to a Bloomberg analysis, remote work’s enduring popularity is costing New York City more than $12 billion a year. Municipal bond buyers should be very careful in their security selection, limiting their purchases to the highest quality credits.

Real estate: residential

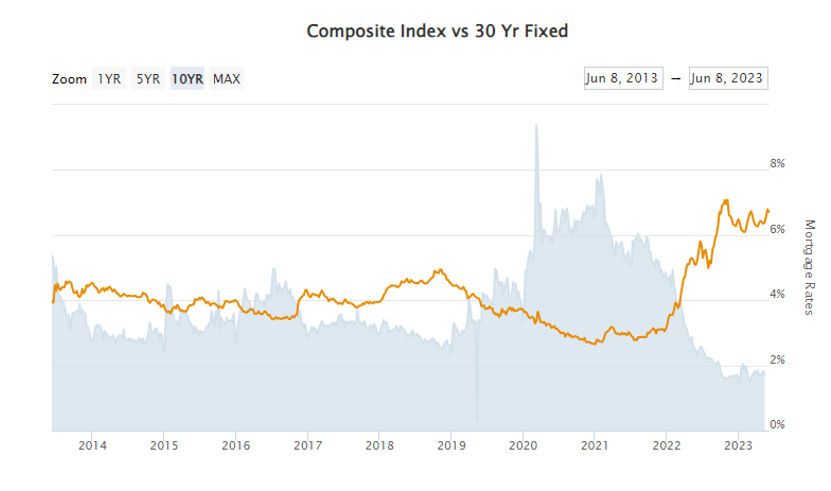

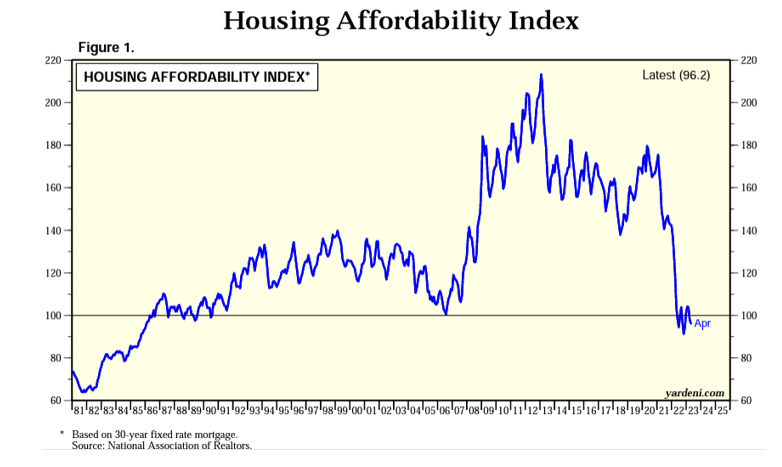

The sharp rise in interest rates dramatically impacted the important housing sector of the economy. As of June 8, applications by home purchasers were down 31% from a year ago, and applications for refinancing were down 45%.

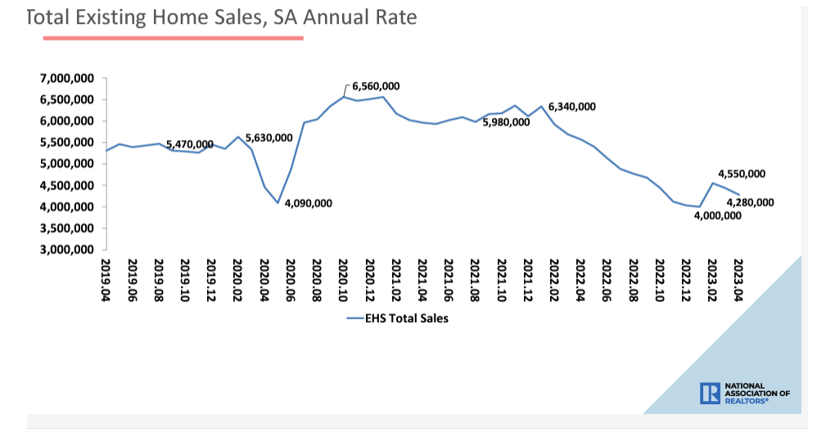

The impact of the rise in rates can be seen in the chart showing U.S. home sales:

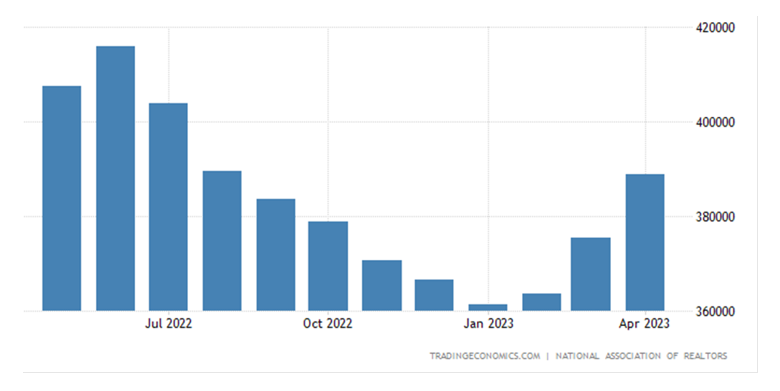

The impact of rising interest rates is shown in the chart below. Over the seven months from July 2022 through January 2023, single-family home prices in the U.S. fell consistently before turning around in February 2023. However, they have been rising since, increasing to $388,800 in April from $375,400 in March, though they remain well below the peak reached in June 2022.

The combination of rising interest rates and home prices has resulted in the Housing Affordability Index falling below the level (100) at which a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home using a 30-year fixed-rate mortgage. The index also remains just slightly above its lowest level in about 36 years.

The problem of affordability, combined with the increasing tightness of the credit market, likely will result in residential construction (about 4% of GDP) being a drag on the economy for the foreseeable future. Together with the commercial real estate sector, they make up about 7% of the GDP.

While the office market is weak, offices are not the only major sector of commercial real estate lending. Other sectors such as single-family homes for rent, apartments, warehouses, data centers and life science buildings all have low vacancy rates and show relatively strong growth in income.

Summarizing, manufacturing and real estate sectors are acting as drags on the economy. However, together they are only about 18% of the GDP. Consider that 70 years ago almost one-third of the workforce was engaged in the manufacturing sector of the economy, a cyclical sector that is much more vulnerable to increases in interest rates than the service sector. In June 1979, manufacturing employment reached an all-time peak of 19.6 million. However, by June 2019 it was down to just 12.8 million. Today, manufacturing’s share of employment is only about 8%.

While the manufacturing, office and residential markets have been experiencing difficult times, for the services sector, which accounts for about 78% of the GDP, it’s been “the best of times.”

Services

The May 2023 J.P.Morgan Global PMI Composite Output Index showed that services activity, fueled by the revival in post-pandemic demand for consumer services activities such as tourism and recreation, “continued to defy gravity with the pace of expansion accelerating from April to the fastest since November 2021.” In addition, “Financial services also experienced a sharp pick-up in new business growth at the second strongest rate since comparable data were first available in 2009.”

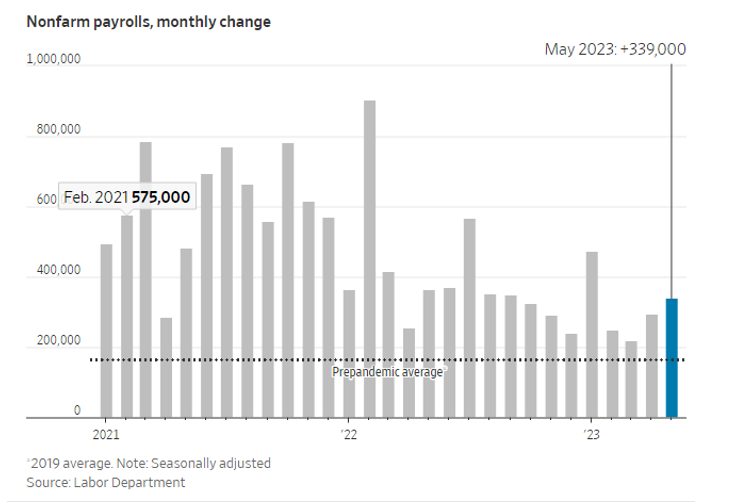

The strength of the services sector has contributed to the strength of the labor market. The May report showed an increase in employment of 339,000. And while the unemployment rate rose to 3.7% from 3.4%, the labor market remained tight, allowing wages to increase at a faster pace (hourly earnings grew 4.3%, similar to gains in the prior three months) than is consistent with the Federal Reserve’s inflation target of 2%. The labor force participation rate (the share of Americans who are working or actively seeking jobs) remained flat in May at 62.6% and below the February 2020 pre-pandemic level of 63.3%. That partially reflects the aging U.S. population. Among workers aged 25 to 54, the participation rate rose to 83.4%, a level last reached in 2007.

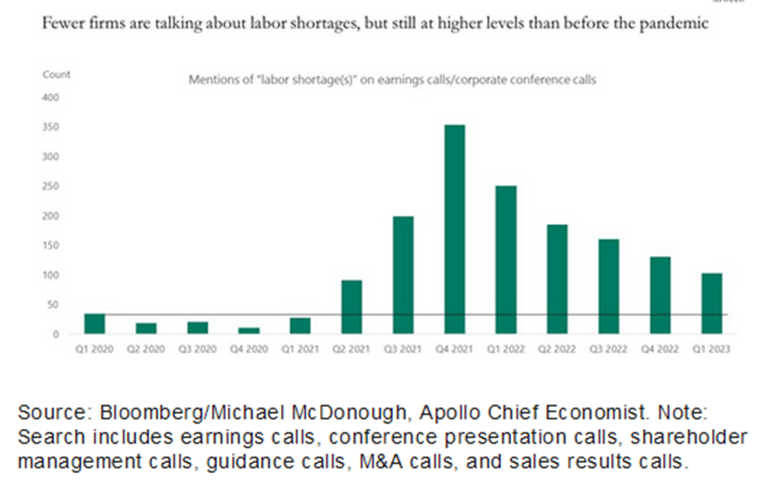

The strength of the services sector, along with the tightness in the labor market (the April report showed 10.1 million job openings compared to 5.7 million unemployed, a ratio of 1.8), is making the Fed’s task to reduce inflation to its 2% target more difficult. And job growth continues above the pre-pandemic level. Labor hoarding due to a tight labor market is a likely explanation. While fewer firms are talking about labor shortages, they are still at much higher levels than before the pandemic.

Further complicating the Fed’s inflation-fighting task is that productivity has been negative for five straight quarters, the longest run since records began in 1948. Nonfarm business labor productivity fell at an annual rate of 2.1% in the first quarter from the fourth, and was down 0.8% in the first quarter from a year earlier. One explanation for declining productivity is that the shift to working from home generated a hit to productivity – and the impact grows with the cumulative loss of creative exchange and mentoring. When productivity falls, it is harder to keep inflation in check (and corporate profits are negatively impacted). The 2.1% drop in labor productivity contributed to the 4.2% increase in unit labor costs in the nonfarm business sector in the first quarter of 2023. While the 4.2% increase is down from the increase of 6.3% in 2022, it is higher than the fourth quarter’s increase of 3.2%.

The strength of corporate and consumer balance sheets has also contributed to the services sector and economic growth.

Corporate and consumer balance sheets

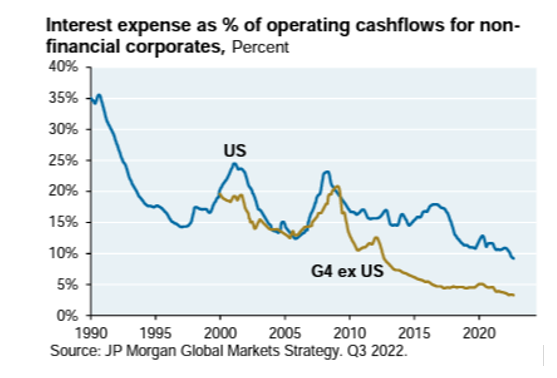

Many U.S. and global companies took advantage of the low-rate environment in the post-pandemic era and refinanced their fixed-rate debt. As a result they have the lowest interest expense to cash flow in decades. Some may not feel a material impact from rising interest rates until 2030.

In addition, U.S. households are in excellent shape, as their ratio of liabilities (debt, leases, property taxes and rents) to net wealth is relatively low, having declined by about 50% since the Great Recession, and household leverage is currently at levels last seen in the early 1980s.

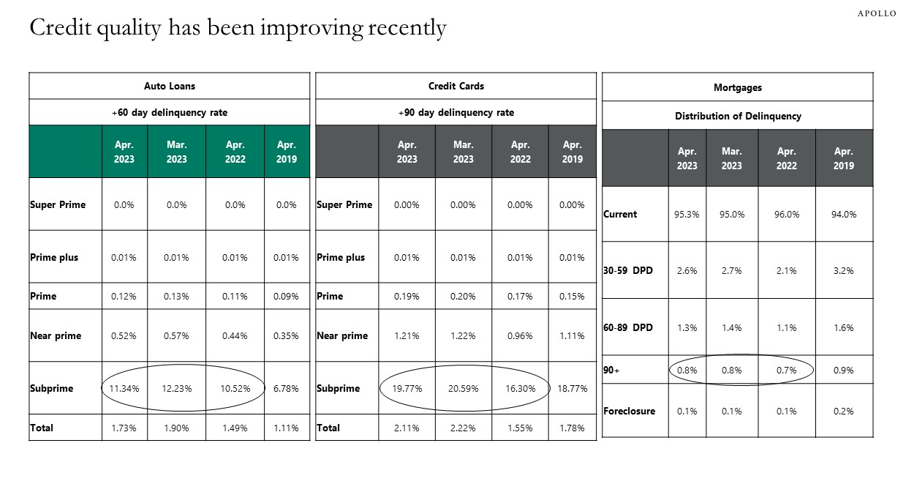

Also, after rising earlier in the year, the latest data shows a modest improvement in credit card and auto loan delinquency rates for subprime, near prime and prime borrowers). This is the opposite of what would be expected when the Fed is trying to tighten financial conditions.

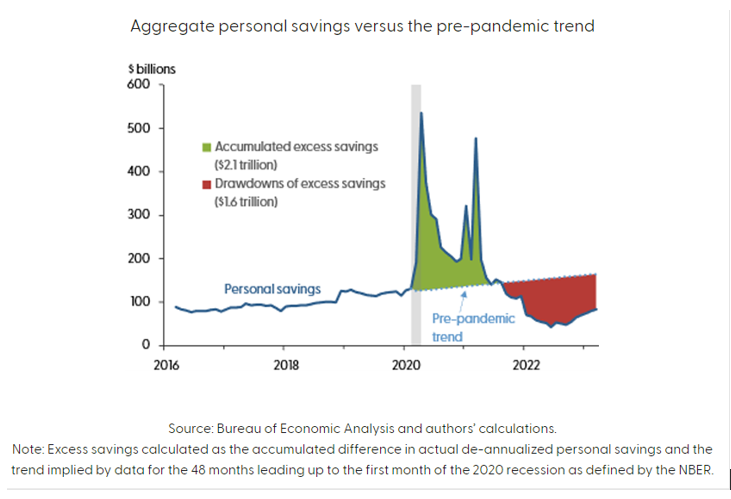

Helping to explain strong consumer spending and falling delinquency rates is that while households have been running down their excess savings built up during the pandemic, a study by the Federal Reserve Bank of San Francisco found that they still have sufficient savings to support spending through at least the fourth quarter of 2023. But the excess savings eventually will be eroded, and the suspension of student-debt repayments ended. In addition, should the unemployment rate rise, households are likely to have a greater appetite for savings and significantly shift their spending habits.

Summarizing, the shift to a much larger services sector, which is much less sensitive to interest rates, means that we have a historically weaker transmission mechanism of monetary policy – the long and variable lag of monetary policy has gotten longer. It’s likely, then, that the costs of capital will remain higher for longer because that is what is needed for the Fed to reduce inflation from 5% currently to the 2% target. It’s possible that the Fed will have to raise the Fed funds rate to 5.5% or even 6% to win its inflation fight.

Making the task more difficult is that the U.S. has a long-term problem of underinvestment in crucial assets like housing (the U.S. faces an estimated shortage of about 4 million homes, as new home construction slowed dramatically after the great recession, with fewer new homes built in the 10 years ending 2018 than in any decade since the 1960s), energy supplies and public infrastructure in combination with the current undersupply of labor.

Another capacity issue is that the shift toward renewable energy and decarbonization further increases the need for critical minerals, shortages of which are expected to worsen in the coming years, also due to underinvestment. And the trend to deglobalization to diversify supply chains is inflationary because of already-tight labor markets, and it is necessary to build out wind and solar power. Additionally, backup thermal capacity must be built and maintained without supporting infrastructure (e.g., roads, bridges, electric power) due to decades of underinvestment. Here’s an example: Taiwan-based TSMC is a leading producer of semiconductors. It has begun the process of building one of its factories in Arizona. It has high operating costs, a lack of trained personnel and construction snags, all of which may result in U.S. chips costing 50% more to produce than the same chips in Taiwan. While deglobalization might be good for many workers, and for national security, it has negative implications for the fight against inflation.

This is the economic outlook from two forward-looking indicators:

The LEI

The Conference Board Leading Economic Index® (LEI) for the U.S. declined 0.6% in April 2023 (the 13th consecutive monthly decline) to 107.5 (2016 = 100), following a decline of 1.2% in March. The LEI is down 4.4% over the six-month period between October 2022 and April 2023 – a steeper rate of decline than its 3.8% contraction over the previous six months (April-October 2022).

Inverted yield curve

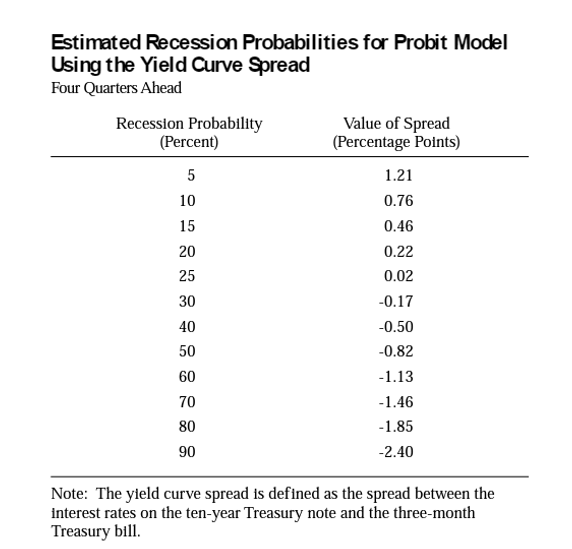

The yield curve has remained inverted at historically high levels. The authors of the Federal Reserve of New York’s study, “The Yield Curve as a Predictor of U.S. Recessions,” concluded: “The yield curve – specifically, the spread between the interest rates on the 10-year Treasury note and the three-month Treasury bill – is a valuable forecasting tool. It is simple to use and significantly outperforms other financial and macroeconomic indicators in predicting recessions two to six quarters ahead.” The reason for the relationship is that monetary policy has a significant influence on the yield curve spread and hence on real activity over the next several quarters. A rise in the short rate tends to flatten the yield curve as well as slow real growth in the near term, and expectations of future inflation and real interest rates contained in the yield curve spread play an important role in the prediction of economic activity. The following chart shows the probability of a recession depending on the slope of the yield curve. As of June 13, the spread between the three-month bill and the 10-year note had widened to 1.41%, indicating a probability of recession approaching 70%. That’s consistent with a Bloomberg survey of analysts that puts the probability of one occurring within the next 12 months at 65%.

However, monetary policy is not yet truly restrictive because the Fed funds rate is still below the growth rate of nominal GDP as well as below the year-over-year core inflation rate, as the CPI for all items less food and energy increased by a seasonally-adjusted 0.4% in May, up 5.3% over the year. Thus, it is certainly possible, if not likely, that the Fed will have to raise rates more and keep them higher for longer – a further tightening of monetary policy and increasing the risk of a recession.

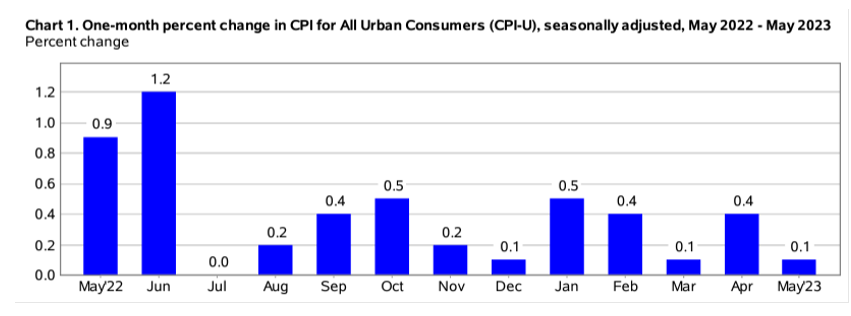

The chart below shows the monthly change in the CPI for All Urban Consumers (CPI-U). While the annual (last 12 months) inflation rate fell from its peak in June 2022 at 9.1% to 5.3% in May 2023, after the June 2023 report the comparisons will be more difficult, as July 2022’s CPI was flat, and August’s increase was just 0.2%. Thus, if the July and August 2023 data shows increases higher than those (which seems likely) the 12-month CPI will move in the wrong direction: higher.

Monetary policy works with long and variable lags

The largest combined monetary and fiscal stimulus experiment in the history of the U.S., which led to the sharp rise in inflation, ended just a year ago. The Federal Reserve ended its program of quantitative easing (QE, buying bonds) in March 2022 and began a program of quantitative tightening (QT, selling bonds or allowing bonds to mature without rolling them over into new purchases) three months later, in June. It is currently shrinking its balance sheet by about $100 billion a month. The Fed has only attempted QT once before: October 2017-September 2019. A recent study by economists at the Federal Reserve Board of Governors estimated that reducing the balance sheet by its current pace would be roughly equivalent to raising the Fed’s policy rate by half a percentage point. However, the authors stressed that their estimate was “associated with considerable uncertainty.” And the Fed has already raised the Fed funds rate by 5% since the start of 2022.

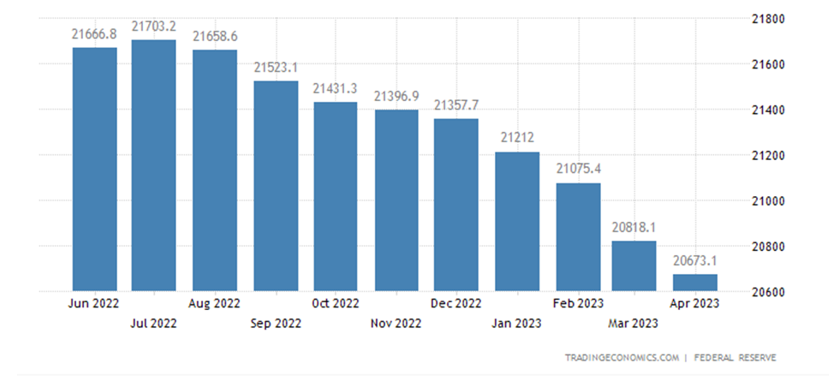

As seen in the chart below, we have seen an unprecedented decline in the M2 money supply over the past year. Changes in monetary policy and economic growth (and inflation) work with long and variable lags (historically 6-18 months) – and the lags may have gotten longer as the service sector’s share of the economy has grown.

Corporate profits

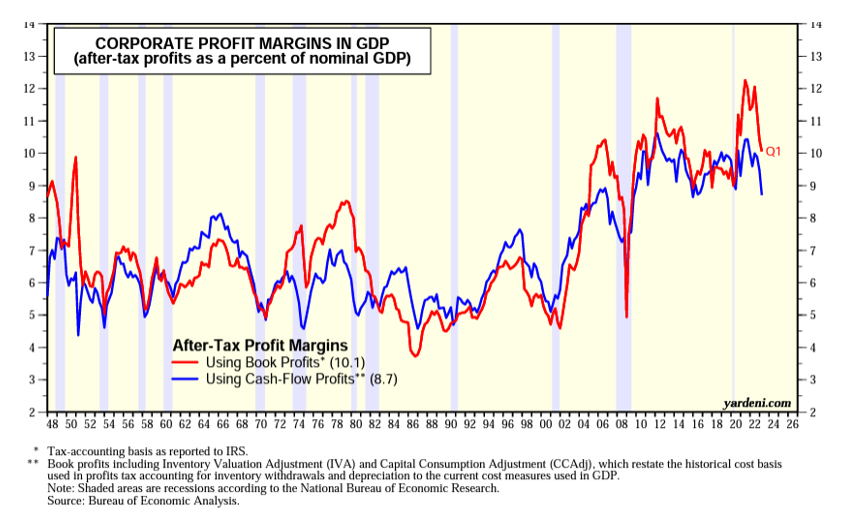

Tight labor markets, while good for wages and the economy (consumer spending accounts for 68.3% of GDP), have the reverse effect on corporate profits. Thus, we could see a margin squeeze (a negative for the stock market) as the negotiating power shifts from employer to employee. The chart below shows that profit margins have been falling for more than a year:

In addition, tight labor markets mean that wage growth will likely continue to be stronger than the Fed would like, and inflation may be harder to bring down to the target. The tight labor markets could make corporations reluctant to reduce their workforce even if demand slowed, with negative effects on productivity and margins.

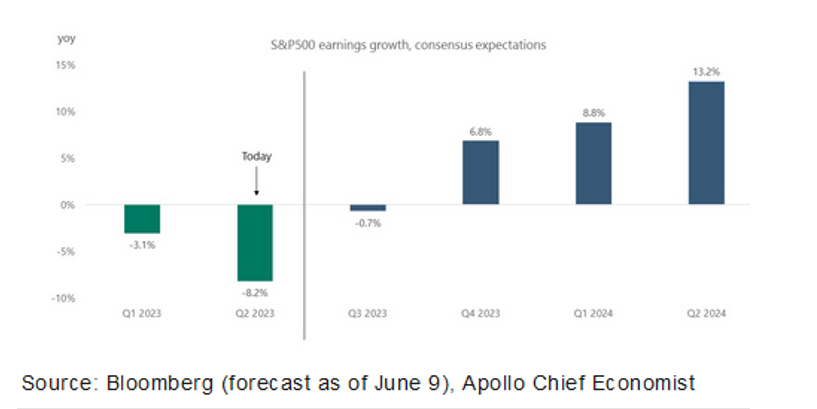

The U.S. Bureau of Economic Analysis (BEA) reported that profits of domestic financial corporations decreased $25.4 billion in the first quarter, following a decrease of $59.0 billion in the fourth quarter. And profits of domestic nonfinancial corporations decreased $109.3 billion compared with a decrease of $22.9 billion in the fourth quarter. While the stock market has roared back, with valuations rising, there have now been two quarters in a row of declining corporate profits.

In 2022 the S&P 500 earned $219.49. Edward Yardeni reported that despite the decline in the first quarter and the forecast of a likely recession, the full-year 2023 forecast from analysts is for earnings to be basically flat at $220.75 (as of June 8). Given that recent earnings growth has been negative, the market thinks we have the worst behind us and that earnings growth is expected to bottom this quarter and then improve rapidly.

This contrasts with the bond market’s inverted yield curve, which forecasts a high likelihood of recession. The earnings forecast will only be correct if core inflation continues to move quickly down toward 2%. If core inflation remains around 4%-5%, the Fed will likely resume raising rates and keep them higher for longer, putting downward pressure on demand in the economy and ultimately earnings.

With the S&P 500 at $4,369 (as of close June 13), the forward-looking price-to-earnings ratio is 19.8. That’s an earnings yield (E/P) of 5.0%, below that of the 5.2% rate on riskless one-month Treasury bills.

There are other areas of concern regarding the economy and markets.

Increases in corporate tax rates

Businesses are getting hit in 2023 with a variety of tax increases even as the risk of recession rises along with interest rates. The tax hikes are arriving for two reasons: provisions of the 2017 tax reform that are phasing out and increases passed as part of the Inflation Reduction Act.

1. The 2017 tax reform spurred investment by letting businesses immediately deduct the full cost of hardware, like trucks and machines. The maximum early deduction drops this year to 80%, and it will continue to decrease each year until it disappears in 2026.

2. January 2022 marked the end of full expensing for corporate research and development. Companies could previously deduct R&D spending from their next tax bill but now must spread the deduction over several years (five years for domestic spending, 15 for international).

3. The cap on the business interest deduction dropped last year when the formula changed to exclude amortization. This is good tax policy, as the tax code should not subsidize debt over equity. However, it comes at a bad time due to the combination of rising interest rates and the risk of recession.

4. The Inflation Reduction Act created a new corporate minimum tax, a 15% levy that hits large U.S. firms earning more than $1 billion in book income annually. The tax will fall heavily on industries like real estate and mining that currently benefit from congressional carve-outs.

5. A 1% stock buyback tax is applied to repurchases of stock by publicly traded companies, which is an alternative way of taxing dividends. These increases will not only negatively impact corporate earnings, but the more investment is taxed, the less the investment, negatively impacting the economy as well.

Debt-to-GDP ratio rising

The Congressional Budget Office projects a federal budget deficit of $1.4 trillion for 2023, with the deficits rising in future years. For example, it estimates the debt will swell to 6.1% of GDP in 2024 and 2025 and will reach 6.9% by 2033. Rising interest rates, required to fight inflation, only worsen the problem. The concern for the markets is that high levels of debt-to-GDP can adversely impact medium- and long-run economic growth for the following reasons:

- High public debt can negatively affect capital stock accumulation and economic growth via heightened long-term interest rates, higher distortionary tax rates and inflation, and placing future restraints on countercyclical fiscal policies that will be needed to fight the next recession (which may lead to increased volatility and lower growth rates).

- Large increases in the debt-to-GDP ratio could lead to not only much higher taxes, and thus lower future incomes, but also intergenerational inequity.

- Increased government borrowing competes for funds in capital markets, crowding out private investment by raising interest rates. Higher rates, along with higher taxes, increase the cost of capital and thus stifle innovation and productivity, reducing economic growth.

- If the government’s debt trajectory spirals upward persistently, investors may start to question the government’s ability to repay debt and therefore demand even higher interest rates.

- Growing interest payments consume an increasing portion of the federal budget, leaving lesser amounts of public investment for research and development, infrastructure and education.

The empirical evidence supports theory. Reviews of the literature, including studies such as the 2020 paper, “Debt and Growth: A Decade of Studies,” and the 2021 paper, “The Impact of Public Debt on Economic Growth,” have found that at low debt levels, increases in the debt ratio provided positive economic stimulus in line with conventional Keynesian multipliers. However, once the debt ratio reached higher levels (between 75% and 100% of GDP), further increases in the debt level as a percentage of GDP had a negative impact on economic growth. As a specific example, the authors of the 2013 study, “Does High Public Debt Consistently Stifle Economic Growth?,” examined the relationship between public debt and GDP growth among 20 advanced economies in the postwar period. They found a negative relationship between debt-to-GDP and economic growth: Growth in countries with a debt-to-GDP ratio between 60% and 90% was 3.2%, but was 2.4% for countries with a ratio between 90% and 120%, and fell to just 1.6% for countries with a ratio between 120% and 150%. The problem for the U.S. is that it is now well within that danger zone.

Given the empirical findings, financial plans should at least consider the prospect of a negative impact on economic growth caused by rising debt and that it could lead to lower future equity returns.

Having reviewed the positives and the concerns, and keeping in mind that everything reviewed is well known by the markets (and thus incorporated into prices), what do professional economists forecast for the economy? The consensus forecast should be considered “the wisdom of crowds.”

Philly Fed’s Second Quarter 2023 Survey of Professional Forecasters

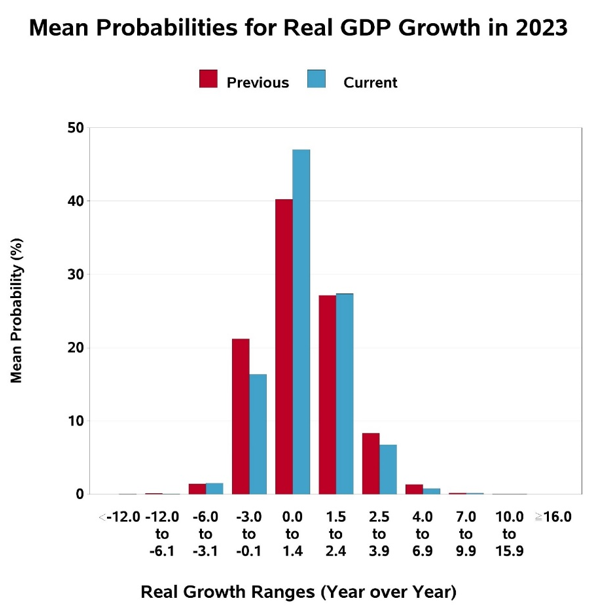

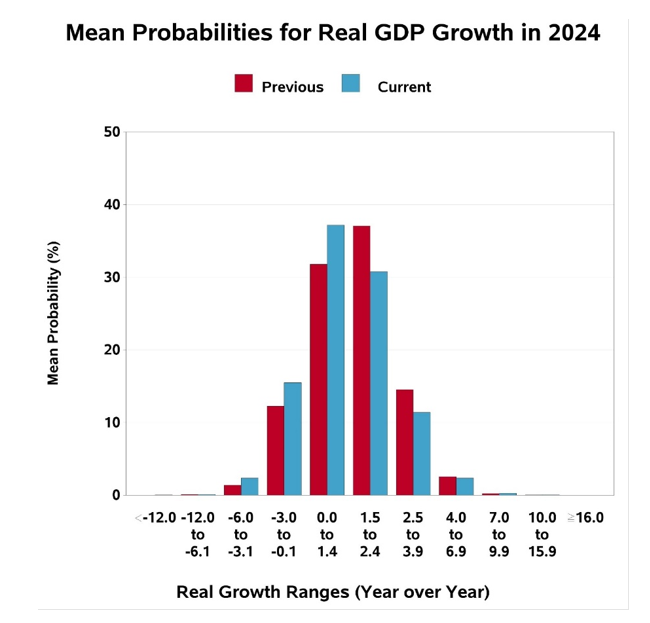

The second quarter 2023 survey, released on May 12, projects real GDP to increase 1.3% in 2023 (the third quarter being the weakest, with 0.0% growth expected) – not a single quarter of negative economic growth, let alone a recession, but just a “soft landing.” They also forecast that economic growth will remain weak in 2024 (growth of just 1.0%). The forecasters predict the unemployment rate will increase from its current rate of 3.7% to 4.1 in the fourth quarter of 2023, and then to 4.2% in the first quarter of 2024, the same rate projected for the full-year average. In terms of inflation, the consensus forecast is for the core CPI to fall to 4.1% in 2023 and 2.7% in 2024.

The following charts show the mean probabilities of real GDP growth in 2023 and 2024. The consensus is that the risk of recession has decreased.

The charts imply that the future is unknowable. Thus, investors should treat the mean forecast of 1.3% growth in 2023 in a probabilistic, not deterministic, way. Another way to think about it is that the forecasters put the odds of a negative quarter of economic growth at 45% for the third quarter, 42% for the fourth quarter, 39% for the first quarter of next year, and 32% for the second quarter – the risks of recession are declining.

The consensus forecast also calls for moderating inflation, though not sufficiently enough to reach the Fed’s objective of 2%. The forecast for the CPI in 2023 increased slightly from the prior quarter’s forecast of 3.4% to 4.1%. However, though it does call for inflation to continue to fall to 2.7% for 2024, it would still be running hotter than the Fed’s 2% target.

Having reviewed the consensus forecast of professional economists (the wisdom of crowds) for the economy, geopolitical risks (potential black swans) also could impact the economy and markets.

Geopolitical risks

While there are always uncertainties created by geopolitics, one would be hard-pressed to think of a time, other than during a world war, when we faced so many at once. Not only is there the ongoing war in Ukraine and the risks it presents, but there is increased tension between the U.S. and China, now the world’s second largest economy. There are also regular threats from North Korea. And the International Atomic Energy Agency reported it found traces of near-weapons-grade enriched uranium (84%) in Iran during a January 22 inspection. Israel views this as an existential threat and feels it might be forced to act before Russia provides Iran with increased defensive capabilities that could prevent Israel from acting. And with the election of the Netanyahu government in Israel, tensions in the West Bank and Gaza have increased.

While each of these risks has a small chance of occurring, investors should make sure their portfolios are not taking more risk than they have the ability, willingness or need to take, avoiding the mistake of treating even the highly improbable as impossible.

As if investors didn’t have enough things to worry about, the risks from climate change are having a greater impact on economies, inflation and markets.

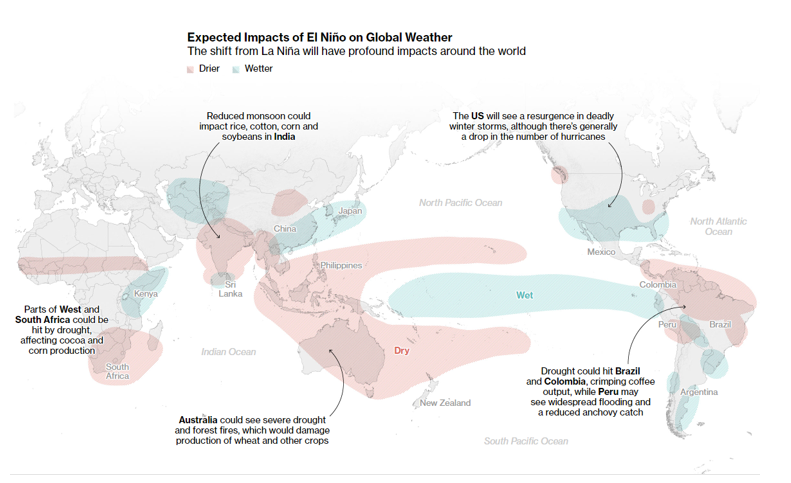

Climate risks

As seen in the chart below, the shift to a warming phase with the arrival of the first El Niño in almost four years creates the potential for damage to an already fragile global economy. According to Bloomberg Economics modeling, previous El Niños resulted in a marked impact on global inflation, adding 3.9 percentage points to non-energy commodity prices and 3.5 points to oil. They also hit growth to GDPs, especially in Brazil, Australia, India and other vulnerable countries.

Dartmouth scientists estimated that the 1997-1998 El Niño led to $5.7 trillion in lost GDP over the following five years. The risks are most acute in the tropics and the southern hemisphere. On the other hand, the El Niño reduces hurricane activity in the Atlantic Basin – during an El Niño year, the probability of two or more hurricanes making landfall in the U.S. is 28%, while during neutral years the probability is 48% and 66% during La Niñas. That’s good news for those living in hurricane-prone areas and for investors with exposure to U.S. hurricane risks through their investments.

Having reviewed the economic news as well as the risks investors should consider, what is the outlook for the financial markets?

Markets

While investors have many reasons to be less than optimistic as central banks around the globe engage in more restrictive monetary policy to fight the unexpected inflation surge, valuations already reflect that concern. Morningstar shows that Vanguard’s U.S. Total Stock Market Fund (VTSMX) has a P/E of 18.3. Its Developed Markets Index Fund (VTMGX) has a P/E of about 13.0, and its Emerging Markets Stock Index Fund (VEIEX) has a P/E of 11.8. Value stocks are trading as if we were already in a serious recession. As examples, Avantis’ U.S. Small-Cap Value ETF (AVUV) is trading at 7.8 times earnings; its International Small-Cap Value ETF (AVDV) is trading at a multiple of 7.5; and its Emerging Markets Value ETF (AVES) also is trading at a multiple of just 7.5. On the other hand, the large-growth stocks are trading at historically very high valuations. For example, the Vanguard Growth ETF (VUG) is trading at a P/E of 27.4.

The earnings yield (E/P) is as good a predictor as we have of future real returns. Thus, a P/E of 27.4 translates (based on its reciprocal) to an expected (not guaranteed) real return of 3.6%; an 18.3 P/E translates to an expected (not guaranteed) real return of about 5.5%; and a P/E of 7.5 translates into an expected (not guaranteed) real return of 13.3%. For stocks, it doesn’t matter to markets whether the future news is good or bad, only whether it is better or worse than expected. The markets seem to be expecting almost the worst possible outcomes, at least for value stocks, as valuations are near levels reached at the depth of the great recession.

The stock market is a leading economic indicator. As such, markets tend to bottom well before economic indicators such as GDP, payrolls, earnings, housing, peak delinquencies in corporate debt and household credit. During the great recession, while the economy did not bottom until the end of the second quarter of 2009 and the unemployment rate kept rising through October, the stock market bottomed on March 9, 2009.

What will happen to corporate profits given what seems likely to be a slowdown in economic activity while labor markets remain tight? The current 2023 earnings forecast for the S&P 500 Index is about $222. With the S&P 500 at about 4,000, that’s a forward-looking P/E of about 18. If corporate profits get squeezed because of wage pressures and a slower economy, and earnings were to fall to, say, $200 (as would likely be the case even in a recession), equities could come under significant pressure, especially if the Fed has to raise rates much beyond 5% to subdue inflation.

Summary of economic and market outlook

The four main themes covered were:

- Inflation: The strong services sector, tight labor markets, continued fiscal stimulus, trend toward deglobalization, years of underinvestment in infrastructure and housing, weak productivity due to working from home, and monetary policy that has yet to turn truly restrictive means inflation is likely to remain higher for longer than the Fed would like.

- Interest rates: The persistence of inflation, significantly higher than the Fed’s 2% target, will likely lead to rates remaining higher for longer. It would not be a surprise to see the Fed resume raising rates after its June pause.

- Access to capital: The problems of the banking system (as highlighted by the failure of Silicon Valley Bank and several others) mean that credit conditions will likely continue to remain tight for an extended period. That will make it more difficult for companies to access capital and roll over existing loans when they mature. Investors should expect defaults and losses to increase in sectors that are most susceptible to higher interest rates and the economic cycle. The equity and debt securities of higher quality companies are likely to perform better in such an environment, and private credit is likely to be a beneficiary.

- Valuations: While valuations of large growth companies are highly elevated, the valuations of small value stocks are trading as if the next great recession were already upon us.

What should investors do?

Be prepared for volatility. As of this writing, the VIX (a measure of the market’s volatility) is trading at about 14, about 30% below its historic average. Given all the uncertainty investors are facing, it is surprising that it is trading at such a low level.

There are two ways to address the risks of a portfolio’s volatility. The first is to reduce exposure to stocks and longer-term bonds and bonds with significant credit risks while increasing your exposure to shorter-term, relatively safe credit risks. By raising interest rates dramatically, the Fed has made that alternative more attractive than it has been in years. For example, for those concerned about inflation, the yield on five-year TIPS has increased from about -1.6% at the start of 2021 to about 1.9% on June 13, 2023.

Another way to address the risks is to diversify your exposure to risk assets to include other sources of risk that have historically had low to no correlation with the economic cycle risk of stocks and/or the inflation risk of traditional bonds but have also provided risk premiums. The following are alternative assets that may provide diversification benefits. Alternative funds carry their own risks; therefore, speak to your financial professional about your own circumstances prior to making any adjustments to your portfolio.

- Reinsurance. The asset class looks attractive, as losses in recent years have led to dramatic increases in premiums, and terms (such as deductibles) have become more favorable.

-

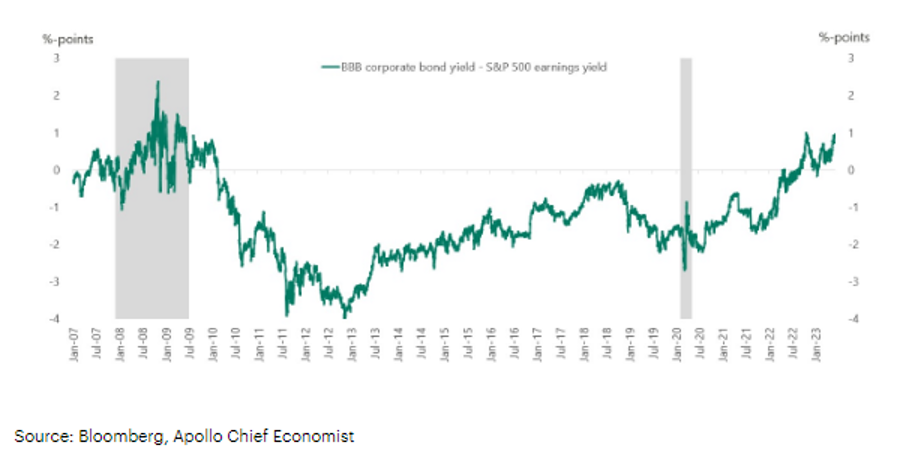

Private middle-market lending (specifically senior, secured, sponsored corporate debt). This asset class also looks attractive, as base lending rates have risen sharply, credit spreads have widened, lender terms have been enhanced (upfront fees have gone up), and credit standards have tightened (stronger covenants). As an indication of the attractiveness of credit relative to the S&P 500, the chart below shows that the yield on BBB credit is at the highest level in 15 years relative to the earnings yield on the S&P 500.

- Consumer credit. While credit risks have increased, lending rates have risen sharply, credit spreads have widened, and credit standards have tightened.

- Long-short factor funds.

- Commodities.

- Trend following (time-series momentum).

As Kevin Grogan and I demonstrated in our book, Reducing the Risk of Black Swans, adding unique risks has historically reduced the downside tail risk associated with conventional stock and bond portfolios.

Postscript

This quote from John Cochrane’s Grumpy Economist column of May 24, 2023 provides an important insight into why economic growth and productivity have slowed so much in the past 20 years:

Creeping stagnation ought to be recognized as the central economic issue of our time. Economic growth since 2000 has fallen almost by half compared with the last half of the 20th Century. The average American’s income is already a quarter less than under the previous trend. If this trend continues, lost growth in fifty years will total three times today’s economy. No economic issue — inflation, recession, trade, climate, income diversity — comes close to such numbers. Growth is not just more stuff, it’s vastly better goods and services; it’s health, environment, education, and culture; it’s defense, social programs, and repaying government debt. Why are we stagnating? In my view, the answer is simple: America has the people, the ideas, and the investment capital to grow. We just can’t get the permits. We are a great Gulliver, tied down by miles of Lilliputian red tape.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

The opinions expressed here are their own and may not accurately reflect those of Buckingham Wealth Partners (collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC). For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Information may be based on third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Mentions of specific securities are for informational purposes only and should not be construed as a recommendation. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. LSR-23-521

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All