The Data Shows No Evidence of a Tech Bubble

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Tech stocks have had a great year in 2023. Despite many prognostications to the contrary, a rational evaluation of the evidence does not suggest a price bubble in tech or the overall market.

This has been a good year for the overall stock market and a great year for technology stocks. The Nasdaq 100 index – a good proxy for technology stocks – is up a whopping 39% since its late-2022 lows and up over 114% from its trough during the COVID-19 pandemic in 2020. Such strong stock performance has elicited the inevitable contention that there is a bubble in tech stocks that is waiting to snare unsuspecting investors.

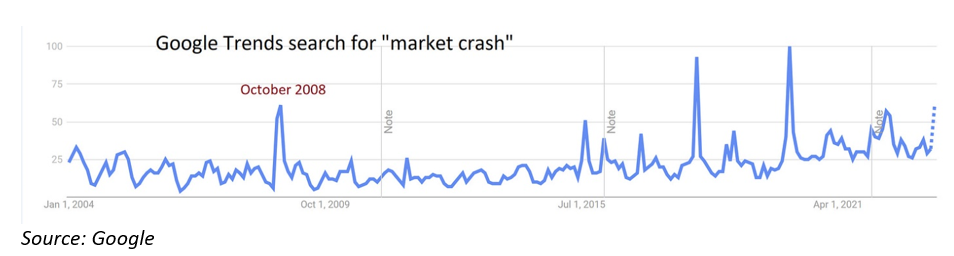

Google search volumes for “market crash” are trending near their levels in October 2008 in the immediate aftermath of the Lehman Brothers bankruptcy in September of that year. Justified or not, there is certainly a lot of concern about the possibility of a stock market bubble from investors and the news media.

One take on the tech-bubble question was articulated in this recent article where I argued that a large price run-up is not, in and of itself, a reason to think stocks are in a bubble: historically, as many large run-ups were followed by further run-ups as were followed by crashes. To distinguish booms from bubbles (i.e., booms that go bust), we need to look at a range of forecasting variables, like corporate and macro fundamentals, as well as market valuations.

Fundamentals

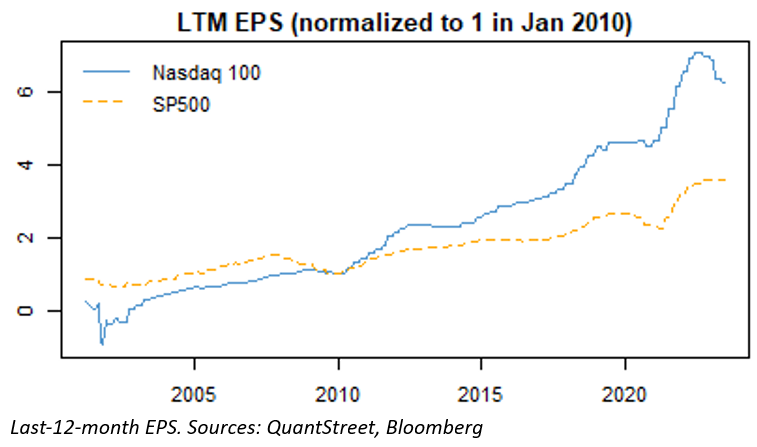

In thinking about the relative return prospects of stocks, an important consideration is the ability of said stocks to generate future income. Looking at the historical earnings per share (EPS) of the tech-heavy Nasdaq 100 versus that of the broad S&P 500 index shows that over the last 20 or so years, tech earnings growth far outpaced that of stocks overall.

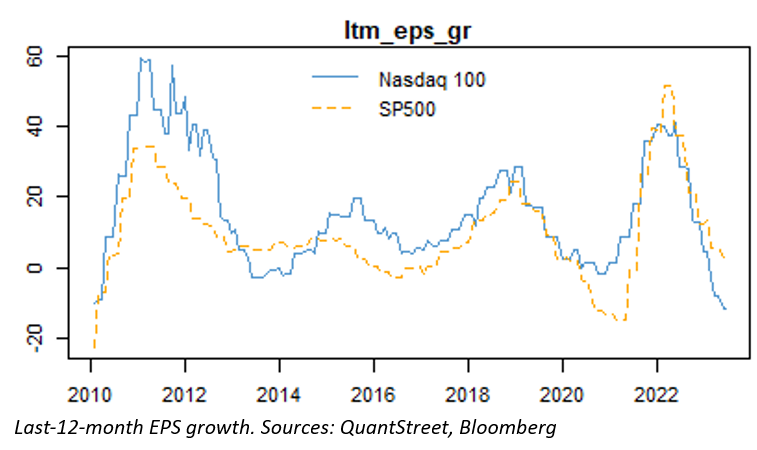

On the other hand, over the last few months the year-over-year growth in EPS has been lower for the Nasdaq 100 than for the S&P 500.

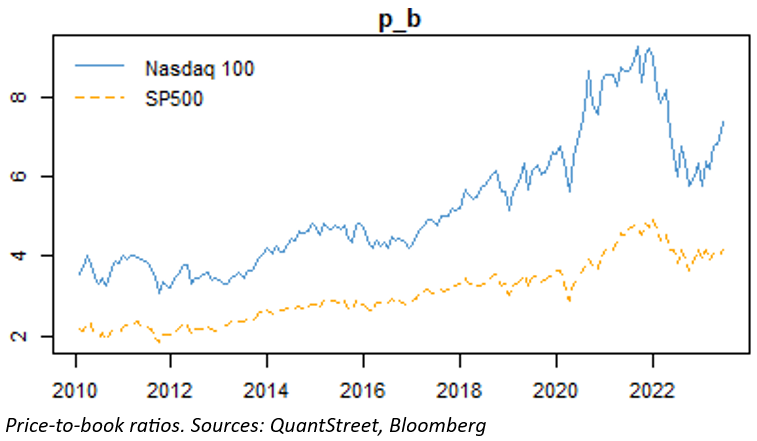

To look at valuations, I examined the price-to-book ratio (P/B), which equals the market value of one share of an index divided by its book value. The P/B ratios of both the Nasdaq 100 and the S&P 500 have been trending up in recent years (perhaps reflective of a general upward trend in valuations that has taken place over the last 150 years). Even so, relative to the S&P 500 index, the P/B ratio of the Nasdaq 100 is now elevated relative to historical norms.

Finally, the interest rate environment is a tough one for stocks. Yields on 10-year Treasury bonds – near 4% – are well above the dividend yield of the S&P 500 index (around 1.5%), which makes stocks relatively unattractive compared to Treasury securities, at least when not accounting for the possibility of price appreciation.

Combining this information suggests that tech stocks, relative to the overall stock market, have faster growing earnings (though not over the last year) and higher valuations. In addition, the high interest rate environment makes all stocks look less attractive relative to Treasury securities.

But such logic is inherently imprecise. A more precise formulation of the problem is: Given the state of multiple fundamental, economic, and price-based metrics and their historical relationship to future returns, what is the appropriate return forecast for tech (and other) stocks?

Year-ahead return forecasts

At QuantStreet, our approach to this question is to apply analytical tools to make the above intuition precise. Using data on 13 stock market sector indexes, we estimate a model that relates index characteristics to one-year-ahead returns using data since January of 2010. Estimating the model reveals several interesting patterns in how index characteristics are related to future returns:

- Past returns, measured over 6 or 12 months, have little bearing on future returns.

- Positive three-month returns are not related to future returns, but negative three-month returns tend to get almost completely (70%) reversed over the subsequent year.

- Higher price-to-book ratios are, indeed, associated with lower future returns, which each 1x increase in the P/B ratio being associated with 4.2% lower next-year returns.

- Past volatility, i.e., the degree to which stock prices fluctuate daily, is strongly positively related to future returns, likely because stock prices get discounted during high-volatility periods in markets.

- Surprisingly, past earnings growth is negatively related to future returns, perhaps because indexes with fast growth over the prior year tend to get overpriced and those with slower growth tend to get underpriced.

- Higher interest rates are associated with lower future returns with each percent increase in 10-year Treasury yields associated with a 2% lower year-ahead stock return.

The above points emphasize why using a model-based approach yields important insights into asset allocation (and other investing) decisions. Models quantify intuition, which allows us to weigh disparate influences and come up with a logically consistent answer.

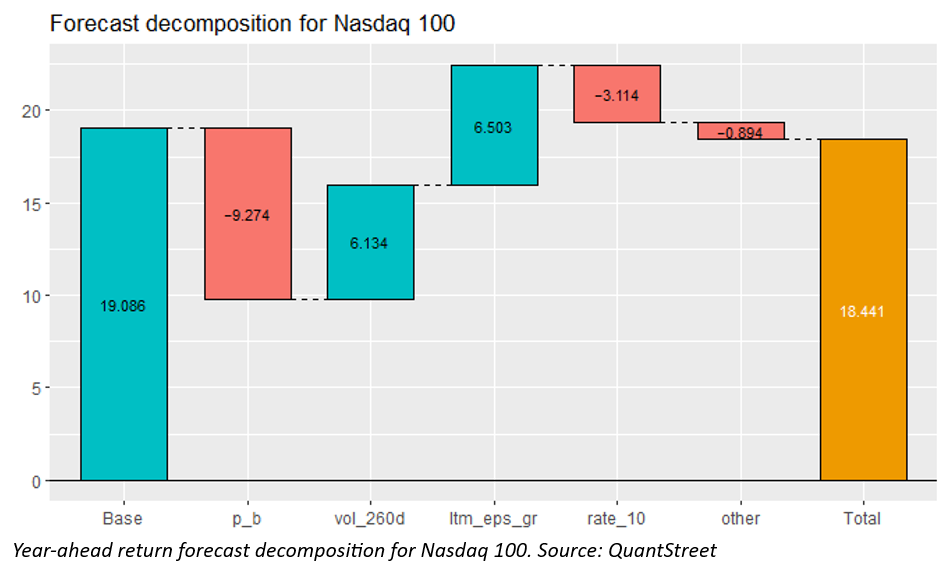

Applying this model to the Nasdaq 100 yields the following return forecast:

The line marked “base” shows the Nasdaq 100 return forecast if all forecasting variables are exactly equal to their average values during the time period used to estimate the model. Each subsequent bar shows how this forecast should be adjusted due to the current state of the forecasting variables.

- As expected, the first bar (p_b) decreases the base forecast by 9.3% due to the relatively high P/B ratio of the Nasdaq 100.

- The second bar increases the forecast by 6.1% due to high Nasdaq 100 return volatility and its historically positive association with future returns.

- The EPS growth bar shows that the lower EPS growth over the last year forecasts 6.5% higher returns for the Nasdaq 100, because of the tendency of sector indexes with slow past growth to trade at a price discount.

- The next bar shows that the high level of 10-year Treasury yields suggests that future returns should be 3.1% lower.

- Finally, the bar labeled “other” combines the influences of several other forecasting measures, none of which has a large impact on the year-ahead return forecast.

Putting everything together yields the total forecast of 18.4%, which is healthy for an asset class widely reported to be in bubble territory.

Investor takeaways

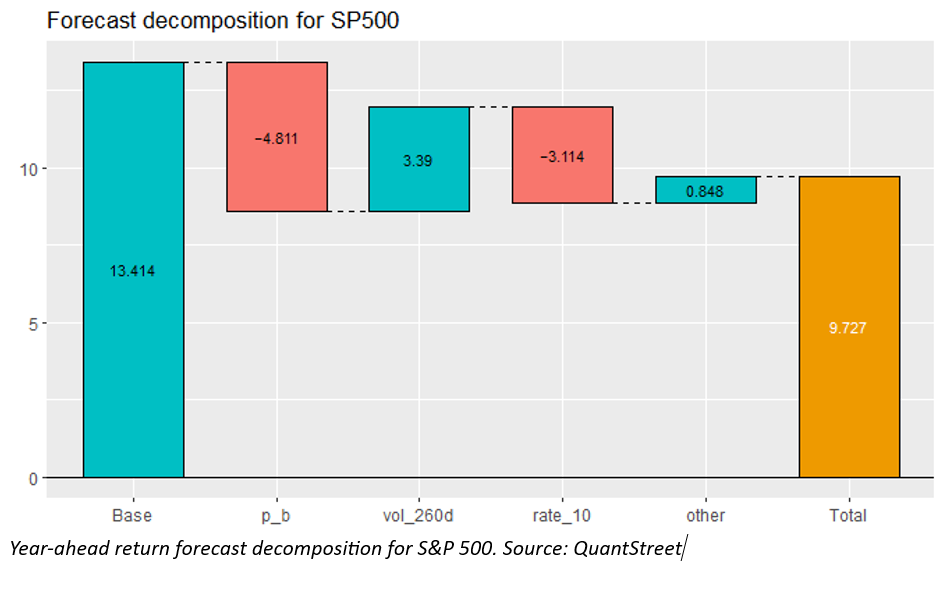

The point of this and my prior article on the alleged tech stock bubble is that loose intuition is not a useful investing practice. My prior article showed that past high returns are not necessarily indicative of a price bubble. The present argument suggests that a rational evaluation of forecasting metrics historically associated with future sector-level stock returns paints a sanguine picture for tech stocks and for the market overall (see figure below).

Of course, this does not mean that tech stocks or the overall market can’t fall dramatically over the next year. Financial forecasts are notoriously imprecise, and many unanticipated outcomes might occur. Investors should carefully consider their own risk tolerance and liquidity needs before making any investing decisions. Those who need assistance should contact a qualified financial advisor.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All