There’s a mantra in markets that you’re not supposed to “fight” the Federal Reserve. Policymakers fight inflation by tightening “financial conditions,” and broad market rallies tend to work against that objective. So as the thinking goes, market bulls are just asking for trouble when they defy the most powerful policymaking establishment in global finance. But if you take Fed Chair Jerome Powell at his word, that thinking is no longer quite accurate.

After a 14% run-up in US stocks this year, Powell was given a golden opportunity on Wednesday — had he wanted one — to jawbone markets back into their place during a panel hosted by the European Central Bank in Sintra, Portugal. Not only did he take a pass, but he implicitly seemed to give the bulls the all-clear. Asked by moderator and CNBC journalist Sara Eisen whether recent stock and bond advances were “counterproductive,” Powell sounded as if he was basically fine with them.

Eisen: Is it counterproductive to you that the stock market has rallied, the bond market has rallied? I mean the market is fighting the Fed. The market thinks you’re closer to the end, and I mean that does make financial conditions easier.

Powell: I thought you can’t fight the Fed, wasn’t that the ... (chuckles to himself)

Eisen: You can’t fight the Fed, but they’re fighting the Fed! Is that a problem for you?

Powell: I don’t look at it that way at all. Honestly, we have different jobs. Our job is to bring inflation down to 2% and sustain maximum employment. That’s our job. That’s what we think about. We look at the data, and that’s what we care about. And markets react – different parts of the market react in different ways. It’s just not something that is a principal focus of our work.

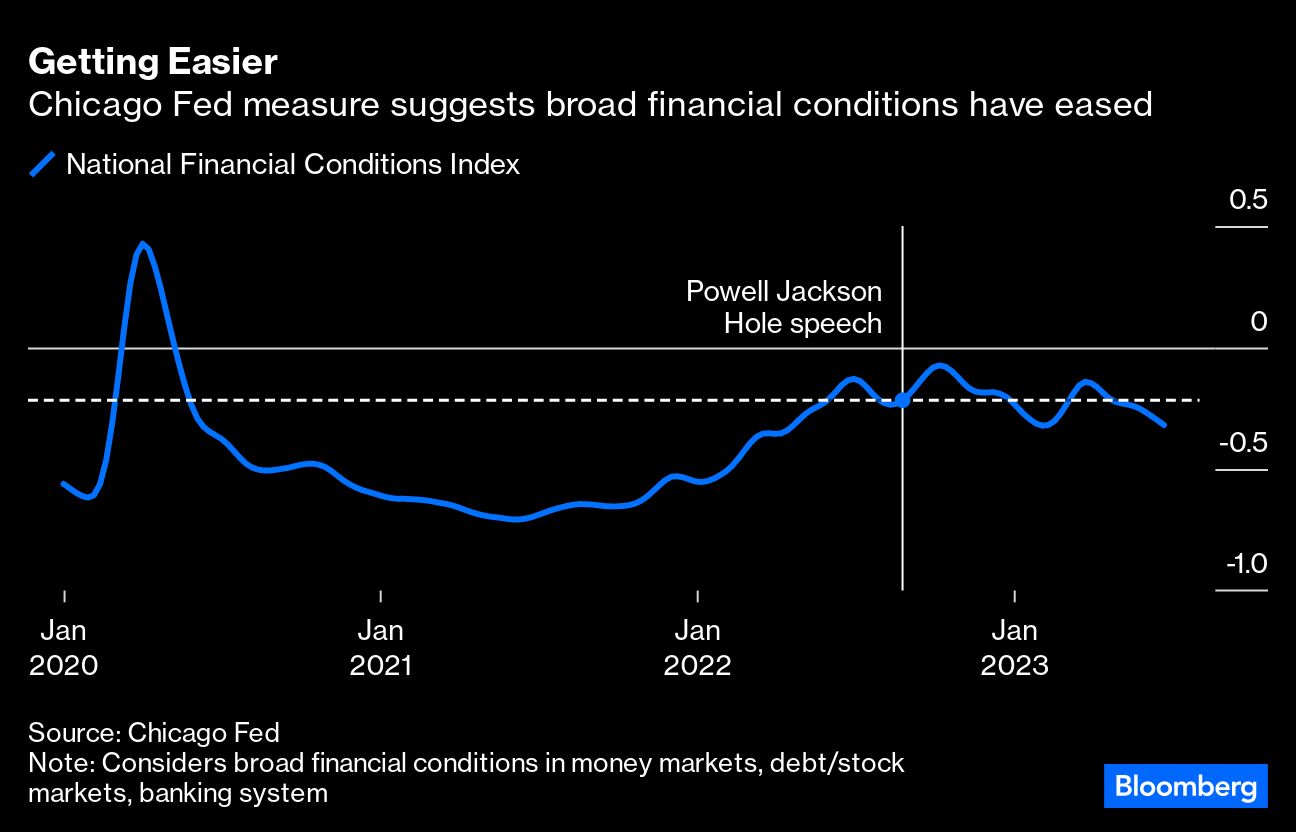

The description of Powell’s operating philosophy, of course, isn’t really new, but it’s telling to hear him speak so deferentially with markets rallying as they are. The Federal Reserve Bank of Chicago’s National Financial Conditions Index shows conditions are about as easy as they have been since early February.

Indeed, conditions are even easier than they were in August 2022, when chatter about a Fed “pivot” and a stock market rally seemed to provoke Powell into a short, direct and resoundingly hawkish speech at the Jackson Hole Economic Symposium that many Fed watchers thought was intended to put markets in their place. Eisen expertly addressed the Jackson Hole comparison in her questioning Tuesday, and it went like this:

Eisen: But it did seem last year like you wanted a weaker stock market. You used the word pain at Jackson Hole. It seemed like you were trying to communicate that financial conditions should tighten and less so this year. Is that right?

Powell: Not really, no. Of course we work through financial conditions, that’s what we do. All the things we do and say work through financial conditions to affect the real economy, that’s how it works. But it’s broader financial conditions. So we’re not focused on any one market. We’re never thinking, ‘Oh, let’s do this to this market.’ It’s just in general, let’s communicate what we want to do and why we want to do it, and financial conditions adjust, and that’s really all we can do.

I have a hard time believing that Powell was as indifferent about market outcomes last year as he implies, but he clearly doesn’t think he needs to stand in the way of a risk rally today. One reason, I’d posit, is that the situation has changed fundamentally from last summer’s rally to today’s. A year ago, core inflation still hadn’t peaked, and there was widespread uncertainty about the degree to which inflation expectations would remain anchored. The drivers of inflation were still widely misunderstand, and policymakers seemed to believe that they needed to use all the tools at their disposal to prevent it from moving higher or becoming entrenched — including aggressive jawboning.

Some 10 months later, inflation has clearly peaked; inflation expectations are under control; and central bankers have collected much more evidence about what drove prices higher in the first place. Fed policymakers will want to maintain some restraint on the economy, but it hasn’t been clear that modest loosening of financial conditions has impeded their efforts thus far — and stock market buoyancy certainly hasn’t been an issue. Since its October lows, the S&P 500 Index has rallied 22% all while the personal consumption expenditures deflator has dropped to 4.4% from 6.3% (reported core has been stickier, but lagged housing disinflation should remedy that soon).

The late investor Martin Zweig, who accurately predicted the 1987 Black Monday crash, is credited with the “don’t fight the Fed” maxim, and it’s generally served investors well over the years. The saying was perhaps most potent under the Alan Greenspan Fed, when discussions of the “wealth effect” from stocks and real estate were prevalent in policymaking circles. As the thinking went, higher portfolio values and home prices made people feel richer, which made them more likely to spend money and fuel demand — generally a net positive but potentially a net negative if you’re fighting inflation. As transcripts show, Greenspan himself grew uneasy in the mid-1990s that rallying stocks could stand in the way of his goal of a Goldilocks economy with tame inflation sustainable growth. Of course, he ultimately got over it and allowed the rally to run (a period I’ve written about at some length here). But today’s central bankers rarely discuss the wealth effect with Greenspan’s zeal and prefer to discuss stocks through the prism of broader “financial conditions.”

I have little doubt that Zweig’s wisdom served traders well early in the Fed hiking cycle of 2022-2023, when policymakers were facing an inflation scare with poorly understood roots and no known endpoint. Under those circumstances, Powell and his colleagues were clearly motivated to assume everything — even the stock market — was a potential threat to their endgame. The situation in June 2023 is nowhere near as frightening, and Powell has no reason to stamp out a rally when there’s little evidence at all that it’s contributing to the problem.

So is “don’t fight the Fed” wrong? Or outdated? I’m sure it will be useful again some day. But at present, there doesn’t seem to be much harm in fighting a central bank that’s explicitly promising not to fight back.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.