Markets are inherently forward-looking, but they’re not clairvoyant. Securities prices tend to reflect some well-founded assumptions about the immediate future and then a whole bunch of wild guesswork about the medium to long term. No one can see two or three — or 10 — years into the future, yet modern finance requires us to try.

There are a few ways to deal with this state of affairs. One of the leading approaches (the one I personally fall back on) is to admit the futility of the exercise and just assume “mean reversion.” You might suppose, for instance, that real profit growth always tends to return to some “normal” rate based on your reading of “recent history” (however you may choose to define it) — and that, indeed, is what the market seems to believe today.

Case in point: In the 1989-2019 period, earnings per share for nonfinancial S&P 500 companies grew by about 4% annually1 on an inflation-adjusted basis. Despite all the frenetic gyrations of the past several years — a generational pandemic, supply chain chaos, Russia’s invasion of Ukraine, the first serious inflation scare in four decades, and an aggressive and coordinated global central bank campaign to stamp out runaway prices — analysts basically expect the same pattern to continue when all is said and done. Sell-side analyst projections for the next few years suggest real earnings growth in 2024 and 2025 will be on the higher side of recent history (7.5% to 9%)2, but if they’re right, the entire wacky 2019-2025 period will average out to — you guessed it! — about 4% real earnings-per-share growth. Is market analysis really that simple? Are we just living through an elaborate period of reversion to the patterns of recent history?

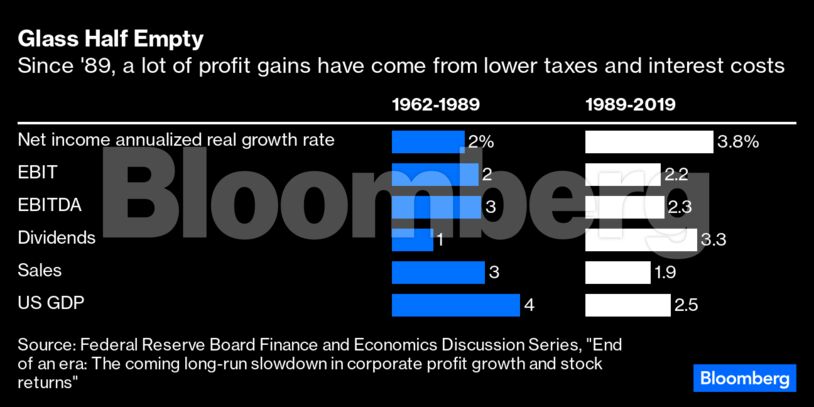

That depends on whom you ask. Consider the recent paper from Federal Reserve researcher Michael Smolyansky, depressingly titled “End of an era: The coming long-run slowdown in corporate profit growth and stock returns.”3 In it, Smolyansky deconstructs some six decades of S&P 500 returns and profits into contributions from falling interest rates; declining effective tax rates; rising earnings before interest and taxes (operating profits); and expanding price-earnings multiples. He divides the sample years into the decidedly lackluster 1962-1989 era and the stellar 1989-2019 period, and he tries to illuminate some of the key differences.

In short, it’s largely about taxes and interest. A significant share of the profit gains in the 1989-2019 period can be attributed to declining effective tax rates and lower borrowing costs; price-earnings multiple expansion — which likewise can be attributed to the decline in risk-free rates — is responsible for a lot of the rest. If those tailwinds fade, he thinks real S&P 500 returns for nonfinancial firms could converge with paltry potential US real gross domestic product growth (generally hovering around 1.8%, according to Congressional Budget Office projections). Here’s a table from Smolyanksy’s work that helps illustrate the point: Real annual EPS growth for nonfinancial S&P 500 companies from 1989-2019 was 3.8%, yet EBIT — earnings before interest and taxes — grew by only 2.2%, less than real GDP.