Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Target-date funds (TDFs), which make up over half of total 401(k) assets, are not following investment theory, exposing investors to excessive risk. The TDF industry is dominated by three firms, Vanguard, Fidelity and T Rowe Price, which manage 65% of the $3.5 trillion in TDFs, stifling innovation and maintaining high risk levels. Personalized target-date accounts (PTDAs) are a promising solution to the problems in TDFs, offering a blend of managed accounts with target-date glidepaths.

TDFs are by far the most popular choice of qualified default investment alternative (QDIA). There are 40 million investors in TDFs in the US. There’s a good chance you and your clients are among them.

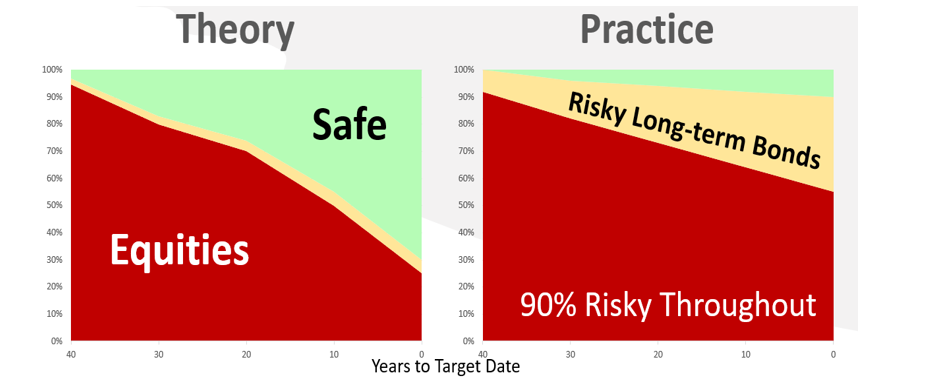

Yet, the theory that TDFs say they follow is not being followed. It’s a “big fat fake out” designed to increase profits. The book that presents the academic theory prescribes a very safe, 80% risk-free allocation at retirement, but most TDFs are 90% risky at their target date.

Consequently, defaulted participants are in great jeopardy relative to the theory and don’t know it. The theory is very protective at retirement while TDF practice is not.

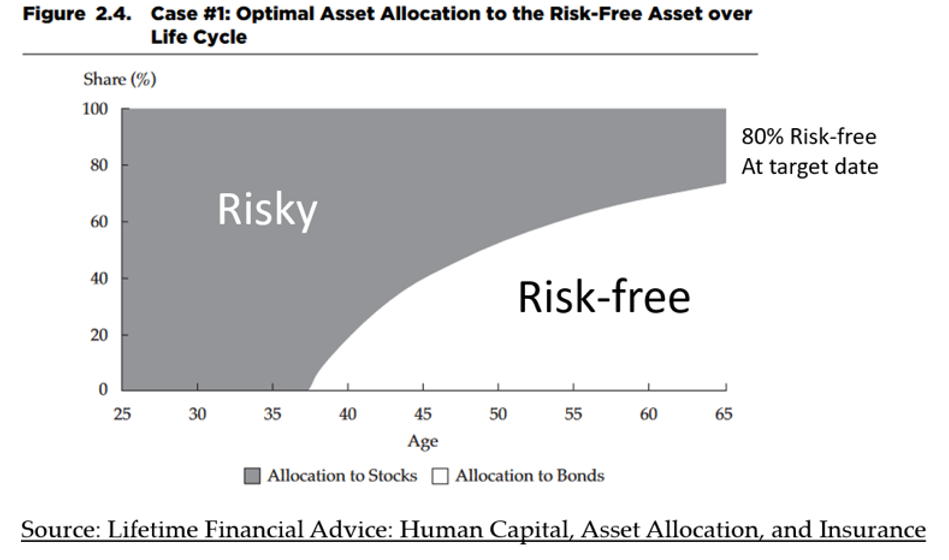

Lifetime-investment theory invests 80% safe at retirement

The book that establishes the theory for TDF glidepaths is Lifetime Financial Advice: Human Capital, Asset Allocation, and Insurance , published in 2007, the year following the passage of the Pension Protection Act of 2006 that launched the preference for TDFs as the QDIA. Four respected academics authored the book: Roger Ibbotson, Moshe Milevsky, Peng Chen and Kevin Zhu.

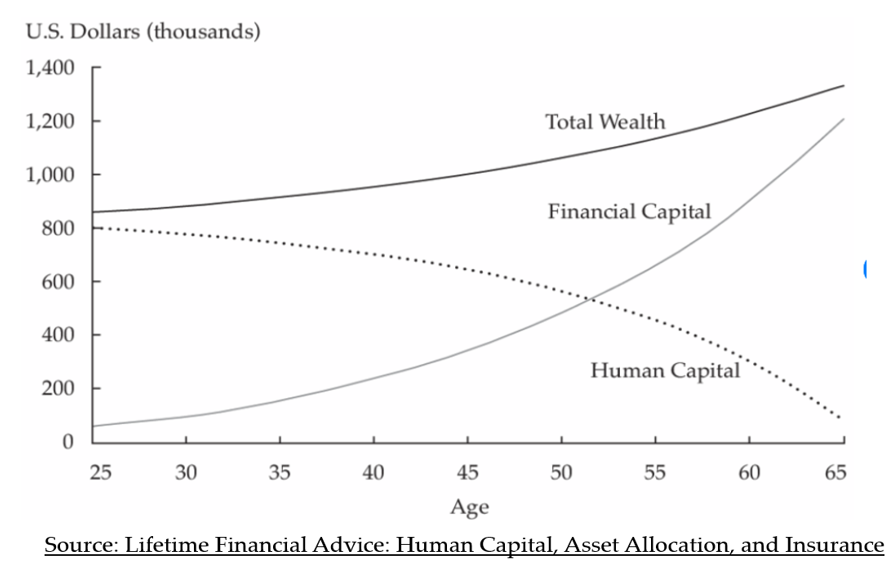

Lifetime-investment theory integrates human capital (the present value of future earnings) with financial capital, as shown in the following image that is commonly displayed by TDF providers.

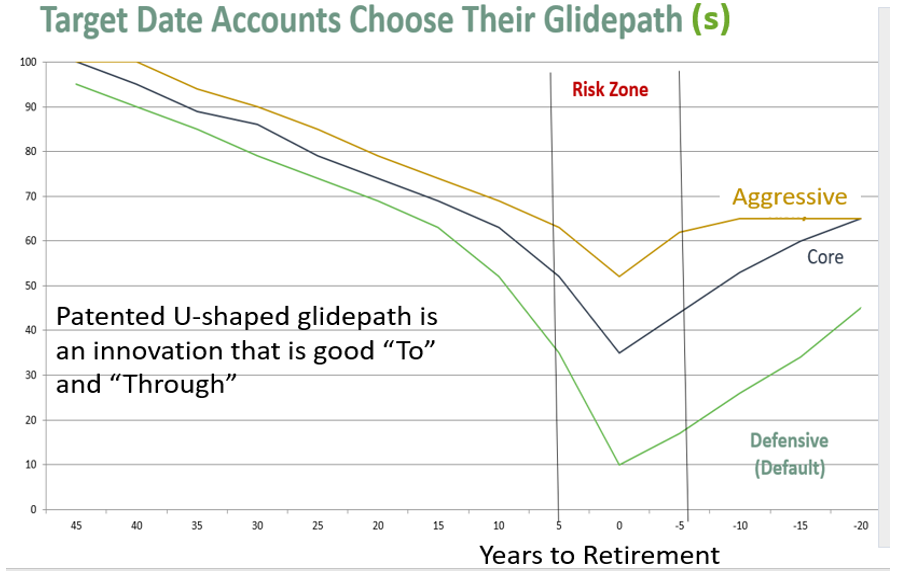

The book is 104 pages. The most important graph is shown below. It prescribes the path for financial capital. The book shows the allocations to two assets – risky and risk-free. I take the view that equities and long-term bonds are risky while Treasury Bills and intermediate Treasury Inflation-Protected Securities (TIPS) are safe.

Lifetime-financial advice is 80% risk-free at retirement, but that’s much more conservative than typical TDFs.

TDF practice is 90% risky at all dates

TDFs no longer “glide.” They “hover” at a constant 90% in risky assets at all ages. By contrast, lifetime-financial advice reduces risk over time.

Long-term bonds are no longer “safe,” although their value increased consistently for the 40 years from 1981 to 2021. But that’s changed, as the world deals with inflation caused by very expensive quantitative easing coupled with the fight against COVID. Unlike the previous 40 years, interest rates are more likely to go up rather than down. Bonds are risky.

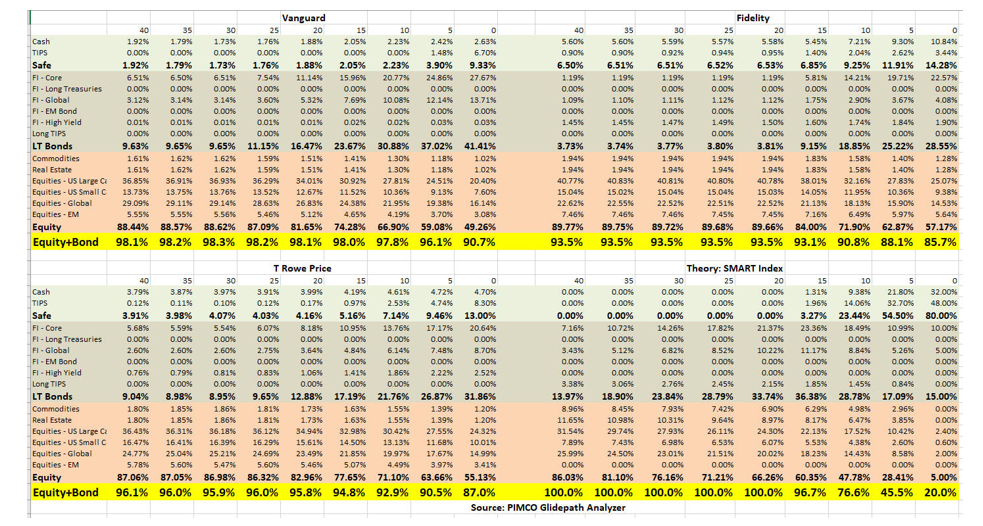

Glidepath details are provided in the following tables where the allocations to risky assets (equities plus long-term bonds) are highlighted in yellow.

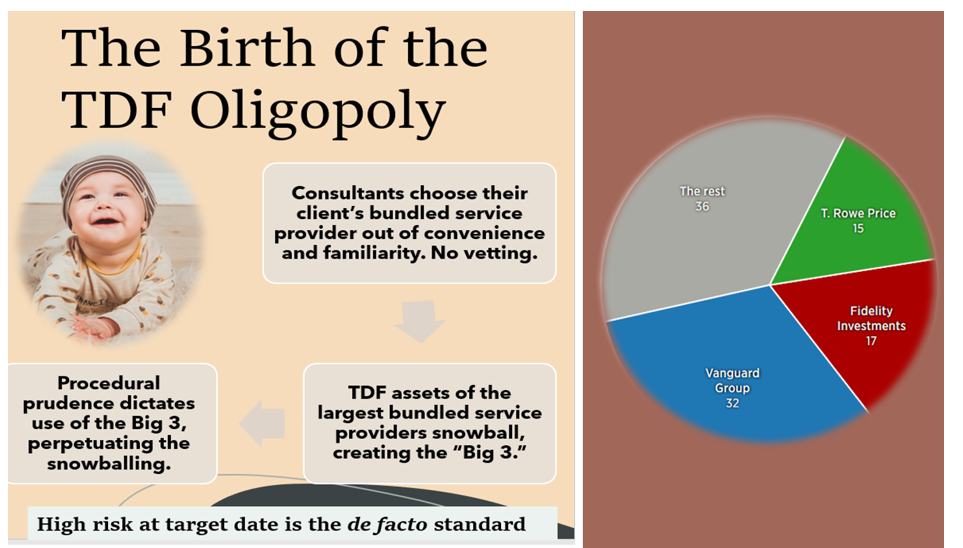

High risk is here to stay if the TDF industry is dominated by just a few firms that dictate investment strategies.

The oligopoly

Of the $3.5 trillion in TDFs, 65% is managed by just three firms – Vanguard, Fidelity and T Rowe Price.

Oligopolies are never good for consumers because they block new entrants and stifle innovation. Oligarchs like the status quo, so they protect it. Lawsuits could change all that.

Excessive-risk lawsuits

The next market crash will expose fiduciaries to lawsuits for excessive risk in default investments. Throwing a dart at the dartboard of QDIAs doesn’t fulfil the fiduciary duty of care – the responsibility to protect our children from harm. Where there’s harm, there’s a foul. “Good heart but empty head” is not a defense, nor is procedural prudence. Excessive fees were procedurally prudent until successful lawsuits changed that. Substantive prudence rules.

Even if lawsuits aren’t filed, employee morale in companies sponsoring 401(k) plans will be crushed, and employers will be blamed. As we learned in 2008, many defaulted participants think they are guaranteed against loss as they near retirement.

The oligopoly could end.

The safe group of TDFs

Not all TDFs are 90% risky. A few follow lifetime-investment theory, including the Federal Thrift Savings Plan (TSP), the office professional’s union OPEIU, the SMART Target Date Fund Index1 and some PTDAs. They exist.

Help is on the way

The future of QDIA investments lies in PTDAs that solve the problems in TDFs, especially the one-size-fits-all shortcoming.

TDFs are popular because of their lack of customization and buy-and-hold approaches, but that causes them to be bad fits for many. So the TDF industry has sought solutions to this and other problems like all-proprietary investing.

One promising solution is a PTDA that blends managed accounts with target-date glidepaths, where several glidepaths are provided from which non-defaulted participants can choose. Non-defaulted participants are provided guidance in this selection through education and a managed-account construct. They can move to any combination of glidepaths at any time.

The QDIA remains one-size., but approximately one third of the assets in TDFs are from non-defaulted participants.

Conclusion

The big fat 401(k) fake out is exposing defaulted participants to excessive risk as they approach retirement. Innovations like PTDAs address this and the one-size-fits-all problem, but innovations rarely gain acceptance in the presence of an oligopoly. Excessive-risk lawsuits could make innovations more attractive.

In the meantime, if you or your clients are invested in a TDF, consider moving out of it as you approach retirement and moving to safety. Help is on the way, but it will take a while.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show.

His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book Baby Boomer Investing in the Perilous 2020s and he provides a financial educational curriculum.

1 I have a personal stake in this company and its products.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.