Why Momentum Has Failed

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Momentum is a strategy designed to profit from “herd behavior” – the tendency for high- (low-) performing stocks to continue to go up (down) as investor enthusiasm for them rises (declines). But as the recent regime changes between value and growth illustrate, momentum is unlikely to be successful in the long term.

Momentum is a strategy designed to profit from “herd behavior” – the tendency for high- (low-) performing stocks to continue to go up (down) as investor enthusiasm for them rises (declines). But as the recent regime changes between value and growth illustrate, momentum is unlikely to be successful in the long term.

Stock price trends can last a long time and then shift abruptly. And then they can enter a period of random back-and-forth, frustrating trend-followers who are waiting for the next longer-term move.

That’s why the momentum factor worked well in the aftermath of the financial crisis through the COVID-lockdown period when growth stocks thrived with nary a setback, but it has faltered since.

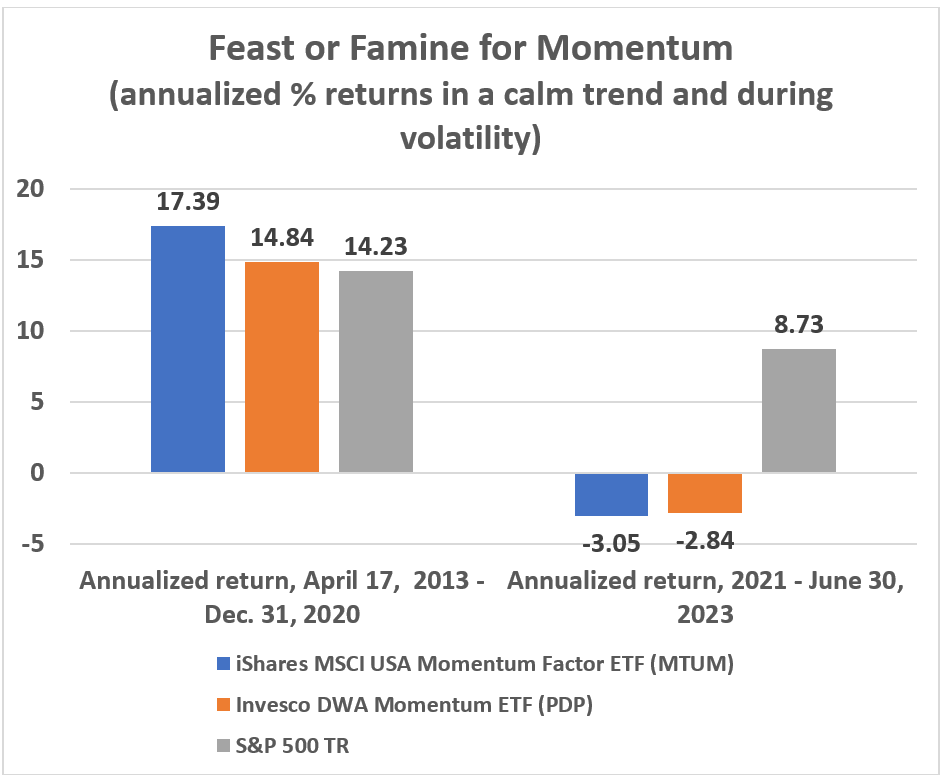

I tracked the two largest momentum funds, the $9.1bn iShares MSCI USA Momentum Factor ETF (MTUM) and the $1.1bn Invesco DWA Momentum ETF (PDP) from April 16, 2013 (the inception of the iShares fund) through the end of 2020 and then for the 2.5-year period from 2021 through June 30, 2023 when trends shifted, to show the discrepancy. (The Invesco fund began operations on March 1, 2007.)

During the first period, when growth pummeled value without a major reversal, momentum funds caught the trend. The iShares fund was up 17.39% on an annualized basis, and the Invesco fund was up 14.84%. Both funds beat the 14.23% annualized return of the S&P 500, though the Invesco fund barely squeezed out its victory.

But from the beginning of 2021, when value stocks regained some of their mojo but abruptly lost it, momentum funds have been disappointing. From 2021 through June 30, 2023, the S&P 500 is up 8.73% on an annualized basis, while the iShares fund is down 3.05% and the Invesco fund is down 2.84%.

The two funds have struggled with the value resurgence in 2022 and the growth snap back in 2023.

Missing the 2021-2022 value resurgence

A big part of that underperformance is that both funds failed to capture the shift to value stocks that began in 2021 and gained momentum through 2022.

For example, MTUM started 2021 with Tesla, Apple, Microsoft, Amazon, and Nvidia as its top-five holdings, occupying around 25% of the fund. That’s understandable because technology stocks had done so well previously.

But while those stocks performed well in 2021, all of them except for Nvidia, which surged 60%, did worse through June 30, 2023 than ExxonMobil. Tesla, Apple, Microsoft and Amazon returned between -8.5% and 19.7% annualized, while Exxon delivered a 53% annualized return over the period.

PDP began 2021 with a more eclectic portfolio. It owned Enphase Energy and Mirati Therapeutics at the top of its portfolio. Apple, Amazon, Tesla and Nvidia were still among the top-15, however.

For the two-year period (2021-2022), Exxon Mobil was up 87% annualized, and the S&P 500 energy sector was up more than 64% annualized. By contrast, the S&P 500 information technology sector was down nearly 28% on an annualized basis. Apple, Amazon, Alphabet, Tesla, Meta, Nvidia, and Microsoft were down between 26.4% (Microsoft) and 65% (Tesla) for the two-year period.

Missing the 2023 growth snap back

This year, growth stocks have snapped back to lead the index’s 16.89% surge through June 17. And that has caused problems for the funds again – especially MTUM.

MTUM is down 0.21% through June 30, while PDP is up 14.34%. The latter’s performance is much better than the former’s, of course, but it still lags the index.

MTUM started the year with pharmaceutical and healthcare stocks at the top of its portfolio. Eli Lilly, UnitedHealth Group, ExxonMobil, Chevron, and Merck were the fund’s top-five holdings, occupying nearly 25% of its assets.

Not one of the big tech names cracked the portfolio at all. (Tesla is technically a consumer-discretionary company, but, because of its electronic-battery technology, is often lumped together with large-tech names.)

PDP started the year with O’Reilly Automotive, Mastercard, and commercial casualty and specialty insurer WR Berkley at the top of its portfolio. The three stocks combined to occupy around 9% of the fund’s assets.

Apple made an appearance in the seventh slot, occupying 2.56% of assets. Microsoft was in the 80th slot, taking up 0.59% of the fund’s assets, while Alphabet was in the 93rd slot, taking up 0.49% of assets.

How the funds operate

MTUM’s literature says it screens for six-month and 12-month risk-adjusted price momentum in assembling its portfolio.

Currently, the fund is in Morningstar’s large-growth category, though it has 11.6% of its assets in industrial stocks compared to 6.3% for its peer-group average. It also has 5% of its assets in energy stocks and 2.8% in financials compared to 1.9% and 9.6%, respectively, for its peer-group average.

Top holdings now are mostly technology names, including Nvidia, Meta Platforms, Microsoft, and Broadcom, but also energy giant Exxon Mobil.

The portfolio was last rebalanced last November, and the prospectus states that “[v]olatile market conditions may trigger ad hoc rebalances of the underlying index, and the fund anticipates higher portfolio turnover under such conditions.”

The prospectus also states, “Stocks that have previously exhibited high momentum characteristics may not experience positive momentum in the future or may experience more volatility than the market as a whole. The Index Provider may be unsuccessful in creating an index that emphasizes momentum securities. “

PDP, by contrast, invests at least 90% of its total assets in the Dorsey Wright Technical Leaders Index, which includes approximately 100 US companies from the Nasdaq. Dorsey Wright defines price strength in relative terms or “as compared to the performance of all other securities in that universe.” The fund and index are rebalanced and reconstituted quarterly.

Its orientation around a technology index explains why the fund could handle a snapback of technology better.

Like its iShares rival, the fund lands in Morningstar’s large-growth category. It has 6% energy exposure compared to 1.9% for its average peer and 26% industrials exposure compared to 6% for its average peer. Its light on healthcare (8.6% versus 14.8%) and communications services (less than 1% versus 9%) compared to the category average.

O’Reilly Automotive is still its top holding.

PDP’s better performance this year could turn sour if this year’s growth rally is a blip within a larger value rebound. Because the fund tracks a momentum index of 100 Nasdaq firms, it would have trouble capturing a longer run of value stocks.

That’s likely why for the 2021-2022 period, before this year’s growth snap back, the fund suffered a 9.79% annualized loss against MTUM’s 3.69% annualized loss.

The underlying problem with momentum-based investing is that it requires a market-timing decision: when to abandon strong-performing stocks in favor of ones that appear to be gaining the market’s favor. This algorithmic decision is based on historical patterns. But, like any market-timing strategy, there is neither a guarantee that the future will behave like the past nor a likelihood that an algorithmic decision-making process will deliver market-beating results.

John Coumarianos manages a registered investment advisor, Mindful Advisory, LLC, in Northern, NJ. He was previously a Morningstar analyst, a writer at Capital Group, and a freelance contributor to the Wall Street Journal.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All