How Well Does Tax-Loss Harvesting Work?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Investors have access to multiple personalized indexing products, a key benefit of which is to allow for tax-loss harvesting (TLH). I analyze when TLH works and how helpful it is to returns.

Taxes are a fact of life, and for investors capital gains taxes are as well. In some years – when highly appreciated investments are sold – capital gains taxes can represent a large hit to investor’s post-tax income. An important aspect of capital gains taxes is that capital losses can offset current or future capital gains and up to $3,000 of current regular income. This feature of tax law creates an incentive for investors to “harvest losses,” that is to sell positions in securities that have lost money from when they were initially purchased (their tax basis).

An important consideration for tax-loss harvesting is the wash-sale rule, which says that once a security has been sold at a tax loss, that security and “substantially identical” securities cannot be bought for a period of at least 30 days before or after the tax-loss sale. (For example, SPY and VOO, both S&P 500 ETFs, would probably be considered substantially identical. Some further thoughts on this are in this article by Morningstar.) Such a purchase within this 61-day window counts as a wash sale. If a wash-sale occurs, the associated tax-loss is disallowed and is added to the cost basis of the bought security, which means the tax-loss is deferred rather than voided (unless the purchase takes place in an IRA account, in which case the cost basis is not adjusted).

TLH strategies involve selling securities at a loss and then replacing them in a portfolio with other securities that are not substantially identical, but are statistically similar (that have similar expected return, risk and correlation characteristics to the sold securities). TLH can be done at the ETF level, where one ETF is replaced with a similar, but not substantially identical ETF, or it can be done at the level of individual stocks using the same criterion. TLH strategies are typically run in separately managed accounts by large asset management firms (here is how Schwab explains the strategy). Such strategies can also be accessed through investment advisors via their custodian firms. TLH strategies are not relevant for tax-advantaged accounts like 401(k)s or IRAs.

As an aside, TLH is not free of controversy, as this recent Financial Times article explains.

Understanding tax-loss harvesting

My firm recently put out a white paper on the topic of tax-loss harvesting. Our approach involved simulating the outcomes of TLH strategies, starting from very simple ones, and building to more complex and realistic examples. Our simulations used the following assumptions:

- When a stock is sold it is assumed that we can buy the same dollar amount in another stock that is statistically similar to the old one but is not substantially identical. For example, say we sold $100 worth of a company that made fertilizer, and then bought $100 of another fertilizer company that has the same expected return, volatility, and correlation structure to the one we sold. This would not be a wash sale, since these are different securities, but it would also not meaningfully change the risk or return profile of our portfolio. This assumption is at the heart of why real-world TLH strategies work: There is usually some other, statistically similar stock to the one that’s being harvested.

- We assumed that the tax rate applying to all capital gains during the life of the strategy is 30%. We assumed that the tax rate that applies to all capital gains at the end date of our analysis – when the portfolio is liquidated – is either 0% (donate wealth to charity or have it pass to the next generation as an inheritance) or 20% (approximately the long-term capital gains rate). See the discussion of tax rates below.

- We assumed that there is no additional investment into the portfolio. The portfolio is purchased and then held until an assumed maturity date. There are no external cash inflows. Stocks are only purchased when other stocks are sold to realize capital losses. When this happens, the proceeds are allocated equally across all existing stocks. In our simulation, this includes the stocks that were harvested. For this to not violate wash-sale rules, we assume the existence of statistically similar stocks to those that were just sold. We didn’t keep track of separate tax lots, but assumed all shares of a given stock are held at the average cost basis.

- In some of our simulations, we assumed that realized losses from TLH were carried over to the end of the simulation period and were applied only to capital gains resulting from the end-of-simulation portfolio liquidation. In other simulations, we assumed that the realized losses can be used to offset other capital gains coming from the investor’s outside trading accounts.

- Finally, in some of our analysis we assumed that annual stock returns of all stocks held in the portfolio have a correlation of 40%. This is in line with historical evidence on average stock-to-stock return correlations.

Tax rates

Before continuing with our analysis, let’s briefly discuss capital gains tax rates and why these can vary across individuals and time.

Federal short-term capital gains (those resulting from securities sold after being held for a year or less) count as regular income, and taxpayers who make above $250,000 per year have to pay an additional 3.8% net investment income tax (NIIT). Long-term capital gains are taxed on a special schedule, and also include the 3.8% additional NIIT. Furthermore, states have their own capital gains taxes. In our simulations, we assume an effective tax rate on intermediate-realized gains – those taken before the portfolio is liquidated – of 30% and a final tax on wealth of either 20% or 0%. The 20% rate corresponds roughly to a long-term capital gains tax rate for affluent households. The 0% tax rate applies if the portfolio is either given to a charity or a charitable remainder trust, or if it is passed on to your estate’s beneficiaries because they receive a step-up in basis (i.e., the cost basis resets to equal the stock price) upon inheritance.

Some of the tax rules involved in this analysis are quite complex. Please consult a tax professional to understand how these tax rules apply to a given situation.

Summary of results

With the prior assumptions, we can analyze the benefits of tax-loss harvesting. To summarize:

- TLH makes no difference if the realized losses are simply carried over to the end of the portfolio simulation. I refer to this as TLH invariance. The reason is that any realized loss decreases the overall tax basis of the portfolio by the dollar amount of the loss. At the end of the simulation period, the realized losses which are carried forward are exactly equal to the higher realized gains upon portfolio liquidation which result from the lower cost basis. Unless there are intermediate capital gains that can be offset by the realized losses, TLH has no impact. A lower cost basis is the hidden cost of tax-loss harvesting.

- When realized capital losses can be used to offset realized capital gains, there are two benefits from tax-loss harvesting:

- The higher the difference between the current capital gains tax rate and the future capital gains tax rate (for example, due to short-term versus long-term capital gains tax rules), the greater the benefit of TLH;

- Harvested losses can be invested and the investment gains on the saved tax payments can be very valuable.

- The higher the current tax rate relative to the tax rate that will be paid when the portfolio is liquidated, the higher is the benefit of TLH as long as there are offsetting realized capital gains.

- The higher the correlation between stock returns, the less valuable is tax-loss harvesting. If all stocks perfectly comove, then there will be many scenarios where there are eventually no losers to harvest since stocks go up over time. When the correlation between stock returns is low, there are many outlier stocks that do poorly when the rest of the space is doing well, and these can be used for TLH.

- Importantly, there is a strong seasoning effect in TLH. The longer a portfolio is held with no new cash inflows, the less benefit is derived from TLH because the cost basis becomes low relative to the current market prices of stocks due to stock price appreciation over time.

Intuition for the invariance result

Our white paper analyzed each of these points, first using a very stylized set of examples, and then using a richer, but more complex, simulation exercise, which I will discuss momentarily.

The main intuition for the TLH invariance result is the following. Say that stock ABC is trading at $8 and you bought it at $10. The cost basis is therefore $2 above the market price. You sell the stock and re-invest the $8 into another stock, XYZ, which is statistically similar to ABC. You now have a $2 realized loss. But let’s assume that there are no offsetting realized capital gains to which this loss can be applied. Instead, you wait for a few years, at which point the entire portfolio is liquidated. And you carry forward the $2 realized loss and use it a few years later to offset realized capital gains which happen when the portfolio is liquidated.

Let’s say that from today onwards, the $8 invested in XYZ and an $8 investment in ABC (which you no longer have) behave in the same way and both appreciate to $14. If you hadn’t ever sold ABC, you would now sell one share of it at $14 which, relative to the initial $10 cost basis, would generate a $4 capital gain. But you did sell ABC, and now own XYZ stock. You then sell the XYZ stock at $14, but the cost basis for XYZ is $8. You now have a $6 realized capital gain. But the $2 tax loss that was generated when ABC was sold can be used to offset this capital gain, making the net capital gain equal to $4, exactly the same as if you had never sold ABC in the first place. The tax implications of either strategy – selling ABC at a loss and reinvesting in XYZ or just not selling ABC – lead to identical capital gains tax outcomes.

To break the tie, you needed to have existing capital gains available at the time that ABC was sold. Then the ABC realized loss could have been used to offset these gains, which would have resulted in immediate tax savings. For example, say that at the time ABC was sold, you had a realized capital gain (from another trading account) that could have been offset by the $2 ABC loss. If your capital gains tax rate at the time was 30%, this would have resulted in $0.60 tax savings. This money could then have been invested for the subsequent few years until the portfolio was ultimately liquidated, and the return on this money would have been yours to keep (after paying capital gains taxes, of course).

Now there are subtleties with this scenario because of the lower tax basis from buying XYZ stock (the white paper gets into in more detail) but the intuition is clear. Intermediate capital gains are needed to monetize capital losses before the portfolio is liquidated for TLH to be valuable.

A closer look at portfolio seasoning

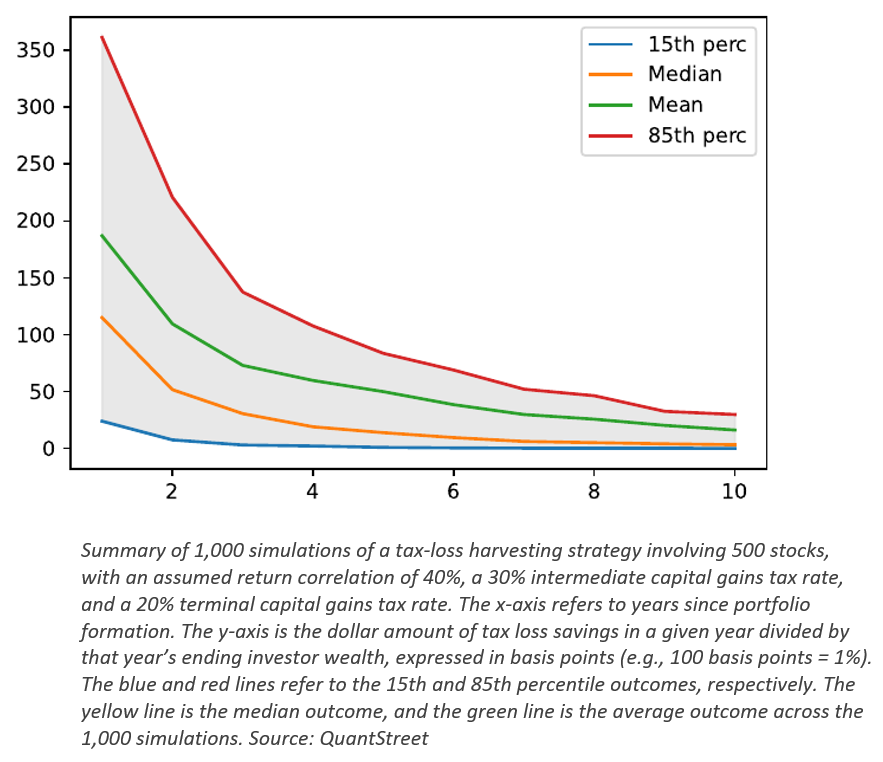

To take a closer look at the tax savings that TLH generates, the figure below shows the outcome of a simulation study we performed in the white paper. The portfolio is assumed to be held for 10 years and then liquidated at the end of year 10. We assumed there are no additional cash inflows that go into the portfolio after it’s been formed.

The x-axis of the figure refers to the number of years that passed from the time of portfolio formation. The values on the y-axis correspond to the dollar amount of tax-loss savings in a given year divided by the end-of-year pre-tax portfolio wealth, expressed in basis points. Tax savings result when losing stocks are sold and when the proceeds from these sales can be used to offset existing capital gains coming from the investor’s outside trading accounts. For example, if there are $10 of capital losses which can be used to offset $10 of existing capital gains, for an investor with a capital gains tax rate of 30%, the tax savings would be $3, an amount which is assumed to be equally reinvested in all existing stocks in the portfolio. (In the second part of the ABC-XYZ example, the tax savings were $0.60.)

This figure demonstrates that tax savings from TLH strategies accrue largely in the first few years after portfolio formation. These are the prime TLH years because at this point stock prices are near their cost basis – prices start out being equal to the cost basis – and regular stock return volatility pushes many stocks below their initial purchase prices, thus allowing for TLH to take place. As the portfolio seasons, since stock prices go up on average (we assume they go up 8% per year on average in our simulations), market prices drift away from the cost basis, which makes it less likely that regular stock price fluctuations will push stock prices below the investor’s cost basis.

If we let the simulation run for more than 10 years, this problem would become even more pronounced. But if the portfolio was receiving new cash inflows, this would mean more stocks are being carried in the portfolio at a cost basis closer to current market prices, which would create more opportunities for TLH.

Summary

TLH needs two ingredients to work: There must be intermediate capital gains that can be offset by the realized losses. Without this, the tax benefit of realized losses upon portfolio liquidation is exactly offset by the tax liability that arises from a lower cost basis. Second, either the tax savings generated from offsetting intermediate capital gains must be reinvested and earn a positive return over time, or the capital gains tax rate at the time of portfolio liquidation must be lower than the capital gains tax rate applied to offset intermediate capital gains. The following all increase the tax benefit of TLH: lower stock return correlation, fewer years elapsed from the portfolio formation date, and a larger differential between intermediate and terminal capital gains tax rates (with the terminal tax rates being lower).

Tax-loss harvesting is a complex strategy that is not suitable for everyone, though it makes sense for investors in high capital gains tax brackets who also have offsetting capital gains. Please consult a financial advisor and a tax professional to fully understand how these strategies apply to your individual case.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

A message from Advisor Perspectives and VettaFi: Advisors who don’t grasp the implications of artificial intelligence (AI) risk being left behind. Join VettaFi for an AI Symposium on August 30th at 11 am ET and hear from thought leaders and experts about how AI will transform the way investing works. Register here!

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All