Why Bond Traders Have it All Wrong

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part one of a two-part series. Part two will appear next week.

“China, Japan, inflation, deficits, and QT, oh my!” – The chant of bond traders watching yields creep higher.

Despite the highest yields in 15 years, some bearish bond traders think they can go much higher. In their minds, China, Japan, burgeoning fiscal deficits, inflation, and QT, are tailwinds for much higher yields.

I have written several articles explaining why entrenched long-term economic growth trends and low inflation, coupled with high and increasing leverage, all but ensure lower interest rates. This article defends my thesis and helps us better appreciate the bearish concerns weighing on bond traders.

As the quote below from Peter Atwater states, the "easiest explanation" is usually the most popular, but that doesn't make it correct. The concerns I cited make for good headlines and may temporarily affect bond yields, but are they worthy of much higher yields?

My bullish bond thesis

I have written extensively on my bullish thesis for bonds. Before reviewing the recent concerns of bearish bond traders, here are links and quotes from my most recent bond articles:

As Rates Rise, Why I Personally Doubled Down on Bonds 8/19/2023

Over the last couple of weeks, I have discussed bonds and why the many concerns of higher, sustained interest rates are not likely. I hope this week's newsletter better clarifies why I am willing to place a longer-term bet on that outcome.

Stocks Versus Bonds: Allocating For The Next Ten Years 8/2/2023

History, analytical rigor, and logic argue that long-term buy-and-hold investors should shift their allocations from stocks toward bonds.

The Government Can't Afford Higher For Longer, Much Longer 7/26/2023

If you disagree with our economic rationale for lower rates, this analysis may persuade you that the Fed and government don't have any options but lower interest rates.

Government Bonds or Stocks? 8/15/2023

In other words, the most hated asset class of 2022 may perform much better than stocks when a recession occurs. So, yes, individuals have a significant value opportunity to buy government bonds today.

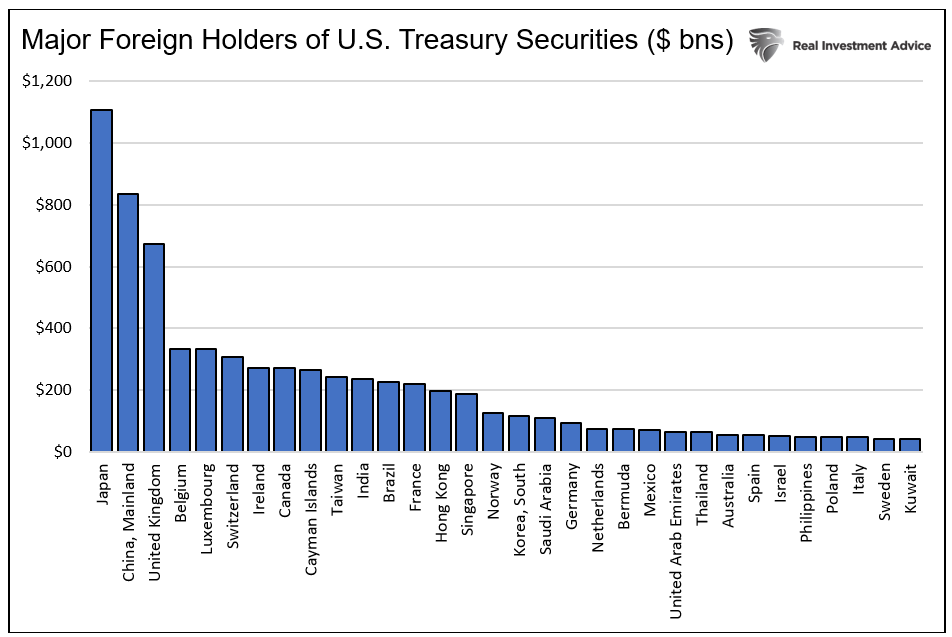

China

Rumors are circulating that China will sell U.S. Treasury securities to support its currency. China is the second largest foreign holder of Treasury bonds.

Might China sell some of its Treasury securities? Yes, its holdings of U.S. bonds fluctuate all the time. But such action could do more harm than good for China.

The yuan now sits at 2007 lows. (The graph below charts how much yuan it costs to buy one dollar. Therefore, the recent upward trend is a devaluation of the yuan.)

Unlike the post-pandemic U.S. economic surge, China's recent reopening has done little to revitalize growth. In mid-August, China unexpectedly cut interest rates to spur activity. China's struggling economy and actions to combat it further weakened the yuan.

China risks further currency devaluation if it stimulates economic activity with lower rates and fiscal spending. A weak yuan versus the dollar is good for China as it promotes exports.

But it also incentivizes capital outflows, putting additional pressure on the yuan. If, instead, China decides to support the yuan, it will likely have to sell Treasury securities. Such could prove detrimental if U.S. bond yields increase, further enticing capital outflows.

Currency manipulation would not likely be prolonged or entail too much Treasury selling. Further, China will probably sell short-term bills to limit realizing losses on its long-term bonds. Additionally, Treasury securities make up a quarter of its foreign reserves, meaning it has other dollar assets to sell beyond Treasury securities.

Bottom line

Even if China sells bonds, the effect will be temporary, and it would likely sell short-term bills that have little impact on long-term yields. If it instead focuses on the economy, a weaker yuan will stimulate their economy and increase capital flows from China, which could bolster U.S. bonds on the margin.

Japan

The Bank of Japan (BOJ) recently changed how it manages yields, a.k.a. yield-curve control (YCC). It will now conduct "flexible" market operations. The BOJ had a hard cap on 10-year yields at 0.5%. Consequently, it would intervene in markets when yields hit 0.50% to ensure they did not rise above 0.5%.

The new policy increases the cap to 1.0% but allows it to manage markets so yields don't immediately rise to 1.0%. Given Japan's high indebtedness, rising inflation, poor demographics, and negligible economic growth trends, it risks economic catastrophe if it loses control of yields.

Over the last 20-plus years, the BOJ has used massive amounts of liquidity to keep interest rates extremely low. Low Japanese yields, and poor stock market returns, incentivized many Japanese individuals and pension funds to buy U.S. assets. Many such investors bought U.S. Treasury bonds. Additionally, a weak yen and meager rates allowed hedge funds to borrow yen, convert to dollars, and buy U.S. assets in a carry trade. Some of this capital from Japan ended up in the U.S. Treasury markets.

Bottom line

Higher yields in Japan may cause some Japanese investors to sell U.S. bonds and buy Japanese bonds. But even at 1%, the yield is still woefully below U.S. bonds at 4-5%. Further, the yen has been weakening. A weakening yen incentivizes Japanese investors to keep money in dollars. Lastly, the carry trade is often short-term in nature. Short-term borrowing rates in Japan are still near zero percent. Unless that changes, most carry trades are likely to persist.

Summary

China and Japan may cause temporary dislocations in the bond markets. But any such events are likely to be very short-lived with inconsequential longer-term effects.

Further, if their actions create liquidity issues or bond yields spike, the Fed and Treasury may take action to minimize their effect on bond markets.

I maintain a strongly convicted view that bond yields will fall in the medium term. It's highly doubtful that monetary or currency policy actions taken by China or Japan to stabilize their economy or markets will alter my view.

Part two will focus on the domestic factors that give bearish bond traders hope that higher yields are in order.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information contact him at [email protected] or 301.466.1204

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All