Investing for Income: A Personalized Approach

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

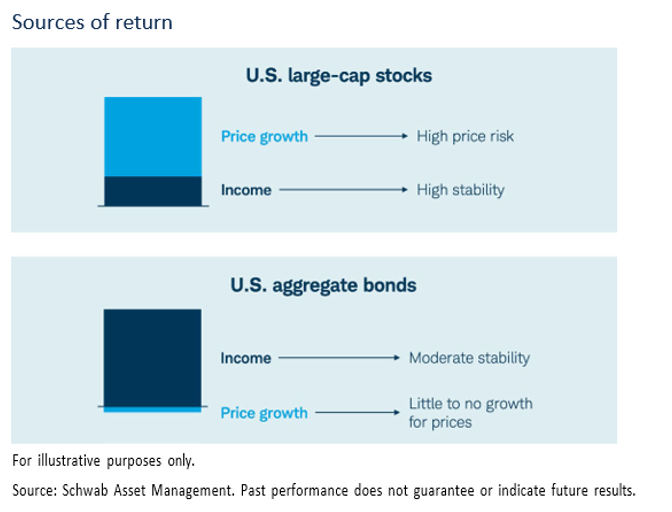

While the typical goal of investing is to grow wealth and assets, for others, a desired outcome is a steady and predictable stream of investment income. Income is a by-product of investing, as most companies pay dividends to shareholders and most bonds make periodic coupon payments and return par value at maturity. Returns from investment income are generally more predictable and stable than those from market price appreciation; although, companies do sometimes reduce dividends, and issuers can default on their loan obligations. And, with notable uncertainty around price return, one could understand why, all else equal, investors might prefer to have a larger component of their total return coming from investment income as opposed to price return. This is true particularly during the retirement phase when investors may rely on their assets to sustain their lifestyle and standard of living in addition to growing for future spending or goals.

Using investments to support spending, interest and dividends are the obvious first choice. Another form of income generation can be through sale of investments, including price growth, and what is commonly referred to as the total-return investing approach. Proponents of a total-return approach for income generation may favor investments that are expected to provide the highest combination of price and income returns rather than investments chosen only for higher income (i.e., yield). Interest and dividends can either be withdrawn as a first source of income or reinvested to take full advantage of the power of compounding. Assets can then be sold, as needed, for liquidity or cash-flow needs.

Behaviorally, however, investors may be reluctant to sell capital (even when market values have appreciated) and generally prefer the stability of investment income and may seek investments with higher income. In addition, uncertainty associated with price returns may lead to fear of faster capital erosion during prolonged recessions or periods of heightened equity market volatility. Stable dividends or coupon payments can help reduce that fear.

Which school of thought is correct? Like most things in life, we believe the answer is not either/or.

Our view on income investing

We believe that a successful income strategy starts with a personalized plan, where financial goals are prioritized and expected spending needs are assessed. This budgeting exercise sets the foundation and can help answer key questions such as immediate versus longer-term preparedness, as well as essential versus more discretionary cash flow needs and, for a retiree, how long his or her money may need to last.

Once income needs and goals are established and prioritized, we believe that the next key step is selecting investments that fit the plan and can meet spending needs while also maintaining a balance between liquidity, stability, income, and growth. Investors can use a variety of strategies, such as so-called “flooring” or “bucketing” approaches, where shorter-term and more stable investments or guaranteed sources of income are earmarked for immediate and essential spending needs, and longer-term and more volatile investments are set aside to meet discretionary or future spending needs, depending on their preferences. Behaviorally, some investors may find it beneficial or convenient to “bucket” their investments in different accounts, each with a different purpose or time horizon, while others lump all investments into a single or few accounts – the choice is largely a preference and exercise in mental accounting.

Once an investment plan is implemented, it’s time to turn these investments into cash flow to meet spending needs. As mentioned above, there are many ways to generate retirement income and, for most, we believe that a balance between investment income and sales of capital and then monitoring a plan based on market performance and other factors, can be appropriate. The “bucketing” approach mentioned above, which segments and dedicates assets for immediate versus longer-term cash flow needs, is an example of a withdrawal strategy that incorporates aspects of both traditional income investing and total-return investing. Retirees should be mindful of the tax implications of different sources of retirement income, and the impact that required minimum distributions (RMDs) or other taxable income can have on things like the taxation of Social Security benefits.1

As with all financial plans, income and investment plans should be revisited periodically – at least annually – to ensure they remain in alignment with the investor’s needs, time horizon and potential changes in circumstances and market conditions. Many plans or “rules-of-thumb,” such as the so-called “4% rule,” may turn out to be more conservative in how much can be withdrawn, if investments perform as expected or better. Monitoring and adjusting a plan annually based on how investments perform can help an investor stay nimble and adjust, to both maximize spending (if appropriate) while aiming to make sure that savings lasts.

Planning for, generating, managing, and withdrawing money from savings in retirement can feel complex, but they are important and common goals for investors’ overall retirement portfolios. Following the steps above to create a personalized plan can help investors create a personalized balance two of the most critical retirement investing challenges: principal protection and a reliable monthly cash flow.

Inga Rachwald is a senior investment portfolio strategist in the income solutions and thematic strategies group at Charles Schwab, and Rob Williams, CFP®, RICP®, CPWA® is a managing director, financial planning, retirement Income and wealth management at the Charles Schwab Center for Financial Research.

Investing involves risk including loss of principal. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Investment returns will fluctuate and are subject to market volatility, so that an investor’s shares, when redeemed or sold, may be worth more or less than their original cost. Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab Asset ManagementTM is the dba name for Charles Schwab Investment Management, Inc, the investment advisor for Schwab Funds. Schwab Funds are distributed by Charles Schwab & Co., Inc. (Schwab) Member SIPC. Charles Schwab Investment Management, Inc. and Schwab are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation.

1023-3S1C

1 Schwab Center for Financial Research Wealth Management Insights, “Tax Efficient Withdrawal Strategies”, released August 2022.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All