Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

"For me context is the key - from that comes the understanding of everything." – Abstract Artist Kenneth Noland. That holds true for me as well! Proper context is required to know if market narratives accurately describe the truth.

For example, in Moody's recent decision to put the United States government on credit watch negative, the context driving its decision was not necessarily run-away deficit spending, as most investors believe. It made its decision within the context of high interest rates:

In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues, Moody's expects that the US' fiscal deficits will remain very large, significantly weakening debt affordability.

Make no mistake, large fiscal deficits and accompanying Treasury debt issuance are a problem. But the downgrade was directly attributable to the level of interest rates. The concern will vanish quickly, regardless of debt-issuance patterns, if interest rates fall appreciably.

At zero-percent interest rates, Uncle Sam, or for that matter you and I, can borrow trillions upon trillions of dollars and not have to worry about making good on the interest payments.

Let's provide context and facts to assess better if the latest bond market bear narrative claiming that higher yields are a direct function of massive Treasury debt issuance is logically defensible.

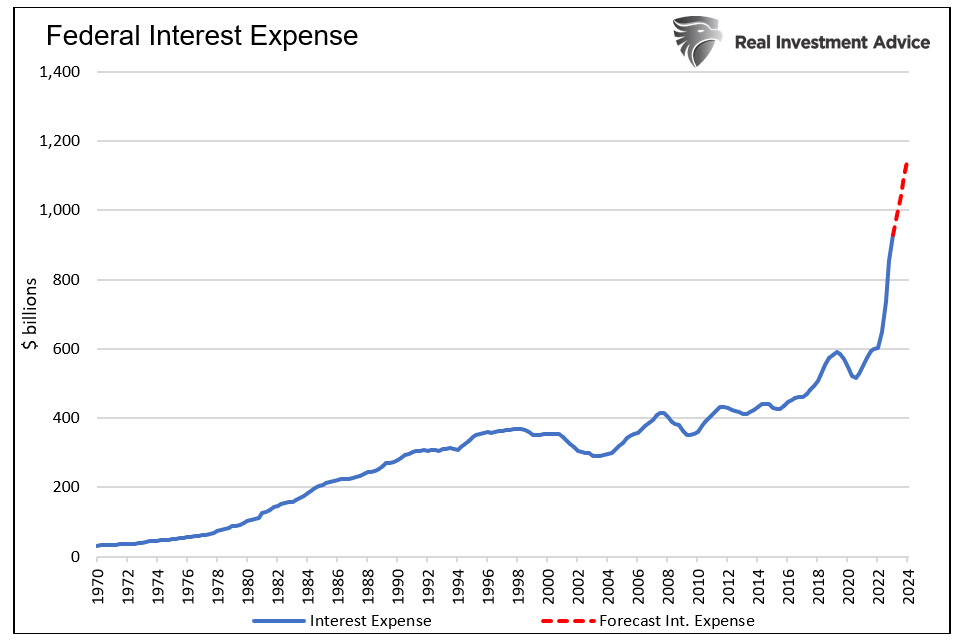

Surging government interest rate expense

My article, The Government Can't Afford Higher for Longer, discussed how higher interest rates are and will potentially affect federal interest expenses. To wit:

Total federal interest expenses should rise by approximately $226 billion over the next twelve months to over $1.15 trillion. For context, from the second quarter of 2010 to the end of 2021, when interest rates were near zero, the interest expense rose by $240 billion in aggregate. More stunningly, the interest expense has increased more in the last three years than in the fifty years prior.

Let's reread the last line – "More stunningly, the interest expense has increased more in the last three years than in the fifty years prior."

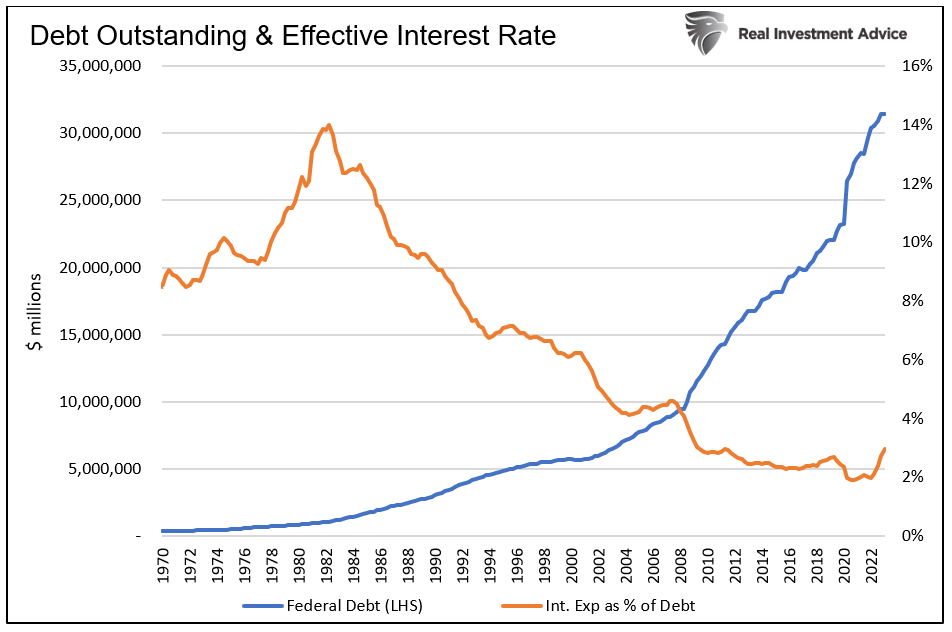

Since 2020, the federal debt has risen by $9 trillion. In the 50 years prior, federal debt grew by approximately $24 trillion. That $9 trillion is significant and fiscally imprudent. But the primary culprit behind the sharp upturn in the nation's interest expense is interest rates, not debt issuance.

The graph below shows that the weighted average interest rate on all government debt has increased by about 1% over the last three years. If interest rates had not risen, today's interest expense would be a little over $600 billion, not $1 trillion as it is. In that scenario, it would only be up by about $50 billion since the eve of the pandemic.

The bear narrative du jour

A popular bond bear market narrative claims exceptional debt issuance is behind the soaring bond yields. Many bond bears believe that even if inflation falls back to the Fed's 2% goal, interest rates will stay high due to current levels of debt issuance.

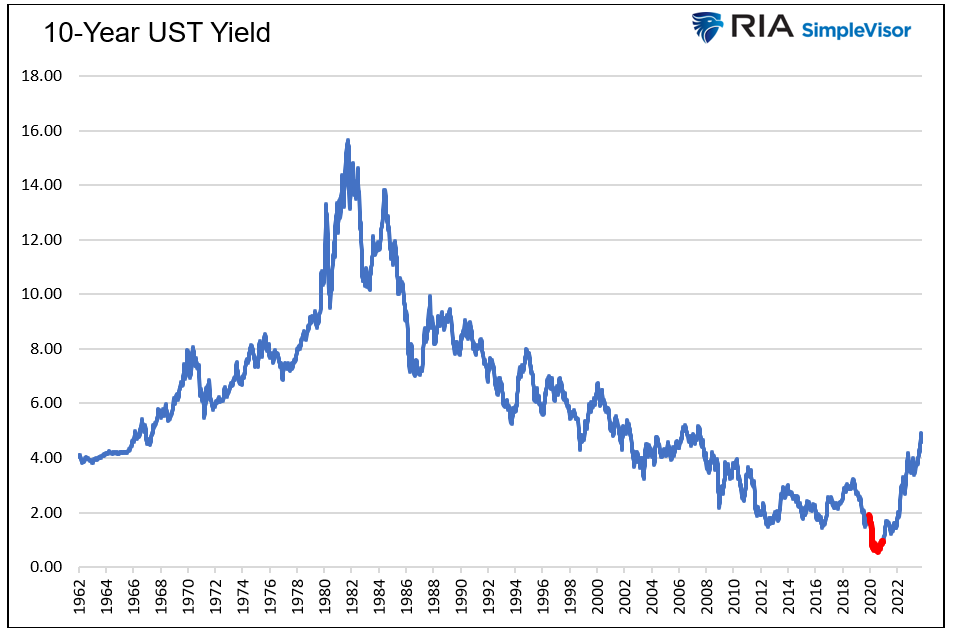

In 2020, the government's debt outstanding grew by $5 trillion, including a whopping $3.25 trillion in the second quarter alone. In 2020, the average 10-year UST yield was 0.92%. During the second quarter, when the market was digesting years' worth of issuance in three months, the average yield was 0.69%.

Apparently, tremendous debt issuance was not problematic in the bond markets then. Might the level of yields and the ensuing interest expense matter a lot more than the amount of debt issuance?

Japan adds credence to that thought. It has a debt-to-GDP ratio of more than double that of the U.S., yet even with inflation rising, it has interest rates of 1% and lower.

Massive debt issuance put into context

I searched Twitter for "massive Treasury issuance," and the quotes below, all from the last six months, are just a few of the many I found:

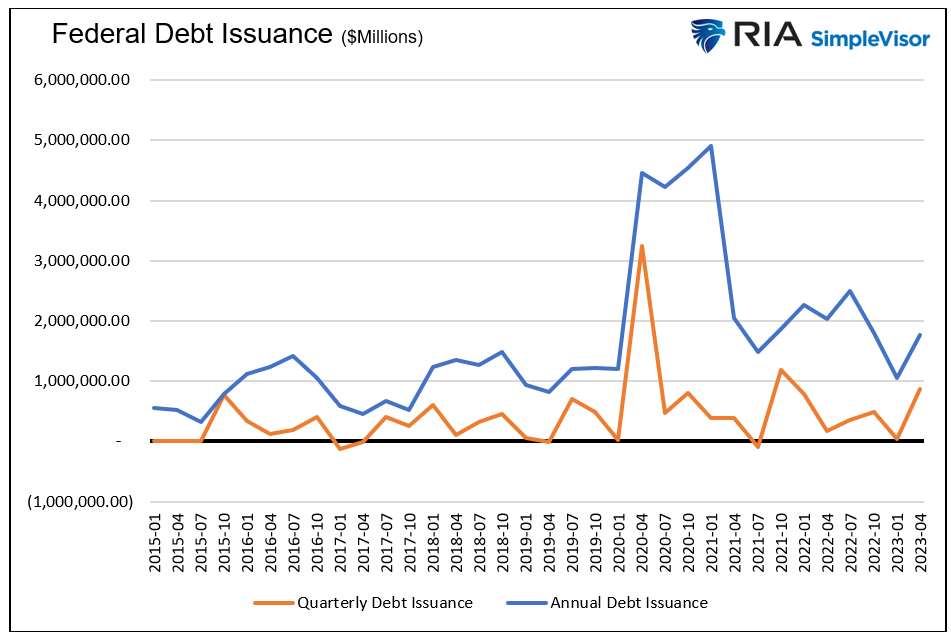

The following graph shows quarterly and annual Treasury debt issuance. The bulge in 2020 and 2021 is prominent. But is the massive debt issuance we are currently experiencing that different from pre-pandemic periods?

Again, proper context is needed to answer our question. Since 2020, the economy has grown by about $5.5 trillion, about 25%. Over that period, the government's tax receipts have increased by 33%.

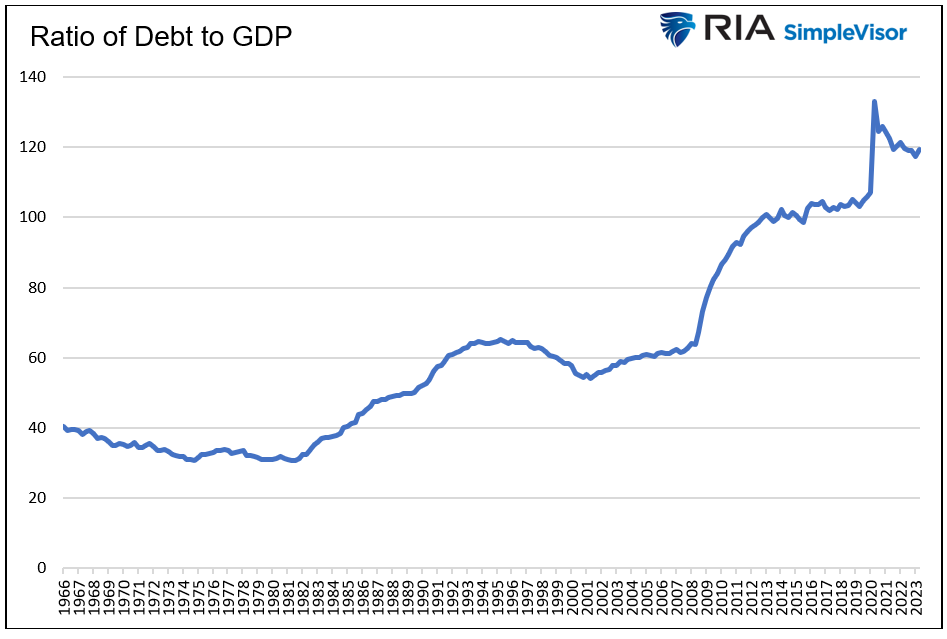

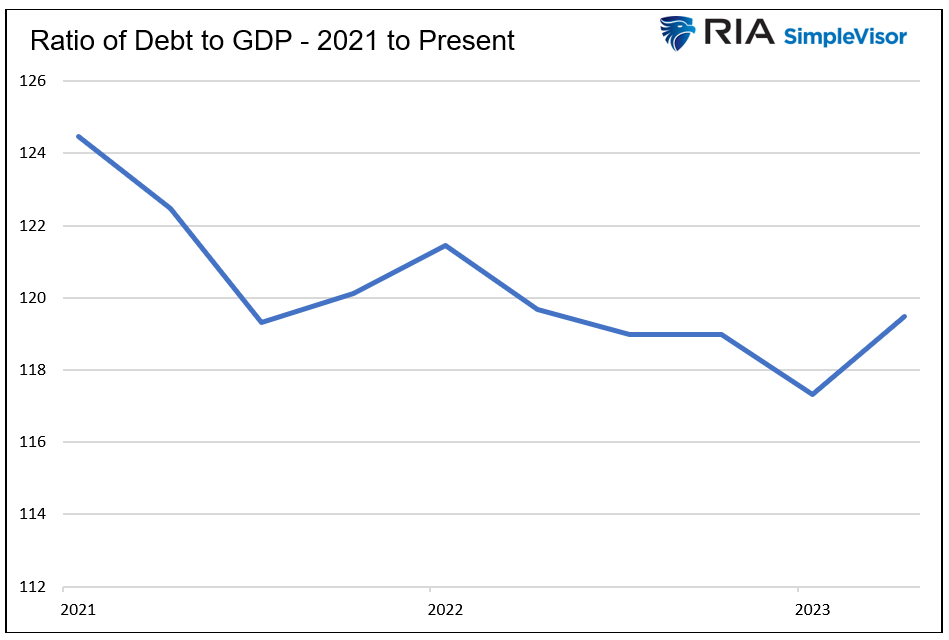

The graph below shows the longer term increase in the federal debt-to-GDP ratio and the surge occurring during 2020. But look at the recent trend, which I enlarged in the second graph. "Massive" debt issuance is not problematic in the context of the size of the economy and the tax base.

The real problem

As Moody's noted, the problem is not a deficit or a debt issuance problem. It's an interest rate problem. Regardless of logic, markets often trade on false narratives for short periods. So, let's assume the narrative of massive debt issuance continues to weigh on the bond market. What might the Treasury or Fed do to lower rates?

Each day interest rates are high, the interest expense will keep rising. Treasury debt with low interest rates matures and is refunded with higher interest-rate debt. As such, higher interest rates feed the narrative, increase the pressure on the bond markets, and boost funding needs.

The Fed can sway long-term rates lower with operation twist. Such allows it to continue to do QT, but all the while selling short-term bond holdings and buying long-term bonds. While not likely in the near term, it can also buy bonds (QE). The risk is that doing so would be perceived as inflationary and might cause investors to push yields higher.

The Treasury is already trying to limit its long-term debt issuance. As I wrote in the November 2, 2023 Daily Commentary:

The Treasury is favoring shorter-term debt as it likely wants to avoid locking in current yields for long periods. Consequently, less than 10% of the debt increase will come from the 10-30 year sectors. Long-term Treasury note and bond investors should like the Treasury's stance.

Additionally, the Fed and Treasury can change bank regulatory and capital rules to make it more advantageous for banks and other financial institutions to hold Treasury debt versus other assets.

Summary

Fiscal imprudence is a big problem, and I am not making light of it. I have written volumes on how unproductive government spending ultimately weakens our economy and reduces citizens' wealth.

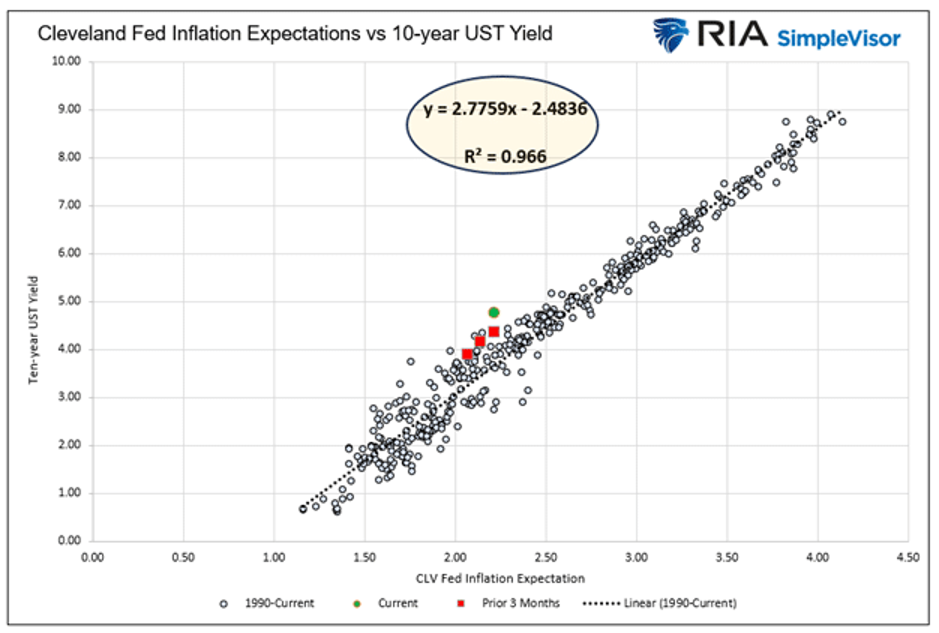

But as bond investors, I and my firm need to understand what drives bond yields and what doesn't. Having debunked the "massive debt" narrative, I end with a reminder of what drives bond yields.

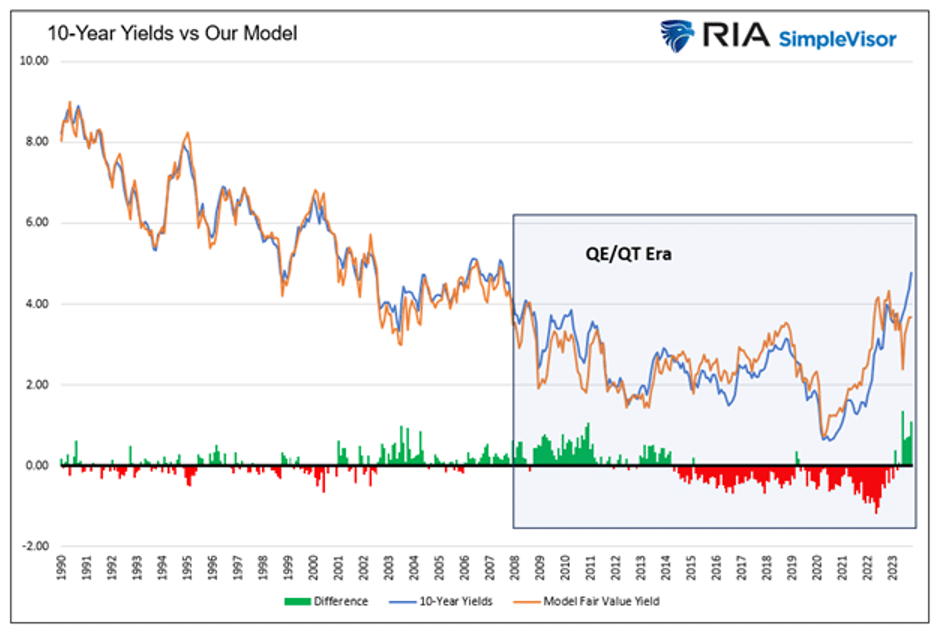

The graphs below, from my article Bond Market Noise Hides Tremendous Opportunity, show the near-perfect correlation between Treasury yields versus inflation and inflation expectations.

I end this article with a quote from the article:

The noise in the bond market is thunderous these days as inflation is still well above norms, deficits remain high, and the Fed continues to promise higher rates for longer. Noise creates differences between the yield on bonds and their true fair value.

Noise is hard to ignore, but it can create tremendous opportunities!

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information contact him at [email protected] or 301.466.1204

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

More Exchange-Traded Products Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.