Last week, the SEC approved the trading of spot bitcoin ETFs. Immediately thereafter, 11 funds, including ones from Fidelity and BlackRock, began trading. I asked our authors and guest contributors the following question:

Given the availability of spot bitcoin ETFs, would you recommend them (or any other cryptocurrency allocation) to your clients?

Below are the responses in alphabetical order:

Jon Adams, CFA senior vice president, chief investment officer at Calamos Wealth Management

The availability of spot bitcoin ETFs is an important development for investors. We are carefully assessing the space and considering adding capabilities to our roster of managers. As always, we recommend a well-diversified portfolio to our clients. Correlation with other asset classes is an important consideration when looking at any new investment and if we were to add cryptocurrency strategies to our platform, we would likely advise a relatively modest allocation given its limited track record in various economic scenarios.

David Blanchett managing director, portfolio manager and head of retirement research at PGIM

Generally, no. I have a hard time with the investment thesis behind owning cryptocurrencies, even bitcoin, especially the valuation component. To borrow from the title of a piece some PGIM colleagues put together recently, I think of cryptocurrencies more as “portfolio kryptonite” versus a “powerful diversifier.” But since not all investors are totally rational (FOMO can definitely be a thing with investing), I can see a behavioral argument towards allocating a small portion of a portfolio to speculative assets, including cryptocurrencies. To be clear, I don’t believe this is something investors should generally do. But for certain investors who are more speculative in nature who are especially drawn to assets with positive skewness, I can see small allocations to assets like cryptocurrencies to make the investor more likely to stick with a portfolio for the long run with only a minor decrease in efficiency. Having cryptocurrency ETFs available obviously makes it much easier to purchase bitcoin using traditional funds and therefore I’ll be curious how the financial advisory community, and investors more generally, respond to this development!

Scott Bondurant founder and CEO, Bondurant Investment Advisor

Bitcoin is a currency. Currencies do not generate any cash flow. Over time, this means they do not provide investors with a real return compared to stocks and bonds that do. In addition, bitcoin is speculative and volatile; two characteristics that are best avoided.

Nathan Dutzmann chief investment officer for Round Table Investment Strategies

Run-ons ahead! Let us take a moment and acknowledge the wonderful irony of “a purely peer-to-peer version of electronic cash [that] would allow online payments to be sent directly from one party to another without going through a financial institution” - the first line of Satoshi Nakamoto’s original bitcoin whitepaper - being made available in a wrapper that involves (at least) an exchange, a market maker, an authorized participant, a fund sponsor, a TPA, a transfer agent, a clearinghouse, a trade desk, and a custodian as intermediaries (but hey, at least they’ve disintermediated the futures exchange!), because that’s just so much more convenient and easier for most investors to deal with! But to answer the actual question, while I’m intrigued by the possibility of crypto becoming a meaningful alternative investment vehicle for real-world projects, the only argument for investing in what has thus far proven to be an enduring but almost entirely self-referential and self-contained ecosystem, with minimal interaction with the real economy and no clear fundamental justification for any particular valuation, is the very reason the SEC called out as a poor investment rationale: fear of missing out. Namely, for those few who will lose more sleep by missing large gains than by absorbing large losses, buying some crypto with money you don’t need, and leaving it there, will likely ensure positive net utility, given the virtual certainty that violent swings in both directions will be experienced.

Ric Edelman founder, Digital Assets Council of Financial Professionals (DACFP)

These comments are full of strong conviction, both favorable and unfavorable. Interestingly, some advisors have made factually incorrect statements to support their opposition. Eventually, all of them will allocate to crypto - and the clients of those who dawdle will pay the price.

Michael Edesess adjunct professor and visiting faculty at the Hong Kong University of Science and Technology

No, I would not recommend any allocation to any cryptocurrency because none of them have a means to generate earnings that accrue to their investors.

Michael Finke professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security Research at The American College of Financial Services

Making it easier to invest in bitcoin through ETFs increases its legitimacy as a portfolio asset. Whether an investor should contribute to a scheme that uses more energy than the country of Argentina to produce random sequences of code that allow individuals to store value outside of traditional currencies is both an ethical and a financial question. Traditional investment provides capital to businesses to create new goods and services that makes life better for consumers. Bitcoin takes wealth and uses it to burn energy for no reason other than to create an alternative source of value to circumvent traditional markets. In the aggregate, bitcoin makes life worse by destroying energy for no reason, enabling crime and corruption, increasing wealth inequality, incentivizing political instability, and pulling wealth out of the economy that could otherwise be put to productive use. It is easy to create a model that demonstrates how adding bitcoin to portfolios would have improved performance over the last decade. That’s not enough to convince me that I should be contributing to a scheme that makes society worse even if it could potentially make me wealthier.

Jon Henshue VP director of alternative strategies at Johnson Financial Group

We remain interested observers of bitcoin and the larger digital-asset ecosystem given the tremendous potential amidst our increasingly digital world. Despite that curiosity, we remain cautious regarding the long-term investment case for such digital assets and regard them as too speculative to invest in on behalf of our clients.

Suzanne Highet financial advisor at Core Planning and independent investment consultant

I am not recommending cryptocurrency to clients, but I do have clients interested and some already holding positions. I continue to offer the same guardrails I always have for any niche or concentrated position: Don't bet more than you can afford to lose (or do without for years at a time) on any single idea. Personally, I have a contributed capital position in crypto equivalent to what I would take to the tables in Las Vegas for an evening, and consider it an entertainment, not an investment. (Below – I'll be curious to see how long the dogecoin continues to exist.)

For clients or advisors interested in the new crypto spot ETFs, I would encourage a careful comparison of the newer mechanisms, as well as the fees (which are surprisingly varied, from 0.2% to 1.5%. (That link is a great intro article!) Risks could include over-concentration at CoinBase, drift from spot value due to trading inefficiencies, and of course, the unknown unknowns. Treat it like habanero salsa – a tiny bit will add a lot of spice to a portfolio.

Rick Kahler founder of Kahler Financial Group

The bitcoin ETFs have not changed my attitude as an advisor. I view digital currencies as speculations, not investments. A true currency is stable and is widely accepted as payment in exchange for goods and services. Eventually, I hope digital currencies achieve the goal of being a reliable storehouse of value. I don’t ever see them being an asset class that I will include in client portfolios.

Fizza Khan CEO of Silver Regulatory Associates

The SEC’s approval of U.S.-listed spot ETFs to track bitcoin is a significant regulatory shift towards the acceptance of and legitimizing bitcoin as an asset class. Further, the regulatory approval signals that both retail and high net-worth, institutional investors are able to add digital assets to their portfolio within a regulated, approved product, which may provide some level of risk mitigation around a class of assets that is typically shied away from because the assets are not widely understood. But this approval does not consider the regulatory risks still prevalent around digital assets as a whole. The SEC has opined that bitcoin specifically, is not a security, which perhaps allowed a bit more comfort by the SEC to approve the bitcoin ETF. But this approval does not eliminate the outstanding question surrounding other digital assets: do these assets meet the definition of a “security” as provided by the Howey test? Perhaps it is not as important to determine this answer, given the approval of the bitcoin ETF, however the next step by financial firms who have requested approval of the bitcoin ETF is to create an ETF of other digital assets.

The potential outcome of the SEC’s approval of a bitcoin ETF is more capital inflow and increased legitimacy for digital assets. But uncertainty remains whether a bitcoin ETF will encourage public acceptance of digital assets as a means of exchange, rather than as a speculative investment. My firm, Silver, does continue to see a steady increase in the number of private fund managers who include digital assets as part of their portfolios, presumably a sign that investors are still keen on the crypto and digital asset space. It will be interesting to see how both institutional and retail investors will react to this latest regulatory development and if it will encourage more retail investment in what is otherwise an asset class geared towards sophisticated investors.

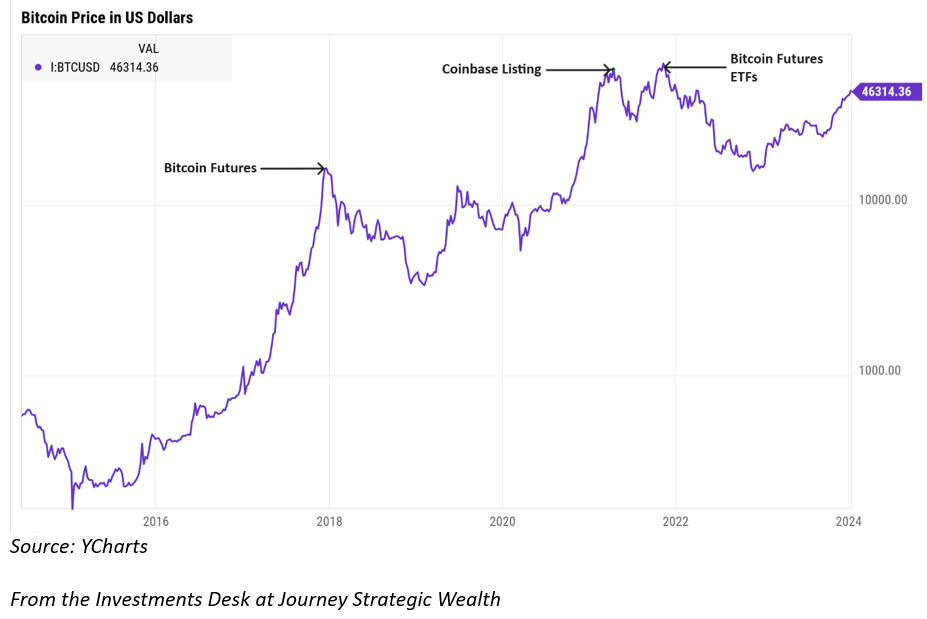

Mark Lebida CFA, managing director, investments of Journey Strategic Wealth

“Bitcoin is like anything else: it’s worth what people are willing to pay for it”

-Investor & Philanthropist Stanley Druckenmiller

While the launching of these new ETFs goes far to legitimizing the merits of investment in bitcoin, we do not anticipate making an allocation to our portfolios currently for two main reasons. First, the low correlation argument tends to go away when accessing capital markets, so the release of these new ETFs could tighten correlations moving forward. Second, the performance in bitcoin over the last eight years or so has peaked around the launch of a new product or influential company and the price of bitcoin has immediately retreated in the past.

Scott MacKillop CEO of First Ascent Asset Management

Bitcoin, like all cryptocurrencies, is like a trip to the casino. Its value is driven by the unpredictable supply and demand appetites of the market. It has no independent value. If a client wants to spin the wheel or roll the dice, so be it, but I would encourage them to keep such mad-money bets small. But I would not include a spot bitcoin ETF in a serious client portfolio.

Harry Mamaysky professor at Columbia Business School and a partner at QuantStreet Capital

Basic economics suggests that the introduction of a new financial product will increase the price of the underlying security if it shifts the demand curve to the right (assuming the supply curve stays fixed). The introduction of bitcoin spot ETFs will push the bitcoin demand curve outward if there are investors who would like to invest in bitcoin and can trade the new bitcoin spot ETFs, but are unable to invest in bitcoin through other channels (which include bitcoin futures and a bitcoin futures ETF). My sense is that the number of such investors is vanishingly small. Any individual or institutional investor who wanted exposure to bitcoin prior to the introduction of bitcoin ETFs was already able to achieve such exposure through multiple channels. This brings us back to the question of what problem bitcoin is trying to solve. It remains a highly inefficient method of electronic transactions. Yes, it allows individuals to bypass some legal and regulatory frameworks, but such individuals are unlikely to invest in mainstream bitcoin ETFs. It just feels like a mini-bubble building on top of a larger one.

Andy Martin CEO of 7Twelve Advisors

The answer is “yes.” Despite being a vocal critic of bitcoin (it's too volatile, not an asset class, and too opaque), the advantage in the ETF is that inside a brokerage account, it is easy to trade, easy to see, and it comes with something bitcoin does not – SIPC protection. Thus, strictly on an un-solicited basis for a HNW existing client, with a less than 5% investable assets allocation, I would.

Dan Pazar executive vice president at Taiko

The new approval from the SEC for spot bitcoin ETFs doesn’t change our opinion that BTC is not a strategic, core investment holding given the associated volatility and lackluster risk-adjusted performance. The frequency and magnitude of the boom-bust cycles will be interesting to watch given the significant expected capital flows into the asset over the next year or two (some are calling for $50 billion!). If that plays out from a retail perspective and price really moves, violent reversals could be more prevalent if/when capital flows move counter to prevailing trends due to the behavioral aspects of market participants with an already volatile asset.

Potential positive developments are lower fees and greatly improved accessibility as there is a race to the bottom (pricing) occurring with ETF providers. Previously, one of the few ways to obtain exposure without owning your own keys was through Grayscale’s listed trust ($28 billion AUM) that charged a 2% fee. This will be moving to 1.5% (upon its conversion to an ETF) which is still more than a full point higher than newer ETF entrants that are charging 20 – 50 basis points (Fidelity, iShares, Ark, Invesco / Galaxy, Van Eck, Franklin to name a few). The other aspect of this is the easy accessibility and tight price tracking that it offers end investors and advisors that have clients who are steadfast on wanting bitcoin exposure. With Grayscale, the price often deviated from NAV and had a high fee making it a difficult sell for advisors with clients who really wanted it. The other main way of owning bitcoin was buying on an exchange and storing it, either on the exchange or personally which has its own set of challenges. Most participants are completely unaware of the difference between blissfully storing on an exchange (and risking theft) vs. utilizing a private, secure wallet where the owner has the keys. Even then, owning your own keys is no walk in the park – recovery phrases, insanely long passwords, and emergency recovery seeds limits ownership to those who are technologically savvy and organized (if you lose your passwords, you are out of luck); this was/is a nightmare scenario for advisors involving regulatory issues around custody and security. The low-cost ETF offerings solve for this to an extent, mainly through lower expenses, assuming you/client are comfortable not owning the asset directly. The purists will tell you that if you don’t personally hold your keys, you don’t truly own the coin which is true given constant hacking and poor custody controls we have seen in the past.

To wrap, we have a more efficient way of gaining access to a highly volatile asset class that may or may not be, one day, more widely used as a medium of exchange. Some will make a lot of money, some will lose, traders rejoice, investors beware.

Tony Petsis financial consultant at Anthony Petsis & Associates

While spot bitcoin ETFs offer an easier and more regulated way for investors to gain access to bitcoin, for most of our clients that are in retirement or planning for retirement, they are not a suitable investment. Many of our clients in this stage of their financial journey require more conservative and income-producing investments, neither of which are represented by spot bitcoin ETFs. As exciting as this news is to many investors, we are fiduciaries and need to continue to do what is in the best interest of our clients.

William Reynolds fiduciary wealth manager with G5 Financial Group

The bitcoin ETF approval was met with little enthusiasm from the investing public. Bitcoin was priced at roughly $46,000 a coin on 1/12/24 and now it is at roughly $43,200 a coin on 1/16/24. Many people hypothesized that the financial firms buying bitcoin would drive up the price due to the limited supply, but I feel all the gains were made on the speculative runup prior to the approval. Now we are most likely seeing profit taking. I don’t think it is something I would allocate to now. I may consider it in the future for a small allocation for aggressive clients.

Allan Roth founder of Wealth Logic, LLC

A spot bitcoin ETF is so much better than the previous futures-based ETFs. Still, I won’t’ be recommending them to clients. I don’t recommend bitcoin or any crypto to a client, but I also tell them it’s okay to carve a small amount of money out of their portfolio to buy whatever they want, including crypto. But, like any investment, an investment in bitcoin should be long-term rather than day trading. So, it’s far more cost effective to buy the bitcoin and hold it. It’s the same reason I don’t believe in gold ETFs but at least those ETFs have a far lower expense ratio. I applaud Vanguard for not launching a bitcoin ETF and they are not depriving investors of anything.

Scott Salaske CEO of Firstmetric

It's just nothing. Just a rock. Leave it on the doorstep.

Chris Shuba founder & CEO, Helios

Over time, I foresee bitcoin playing a role in the alternative section of a portfolio. But I’m hesitant to recommend these ETFs at this time, and I doubt many portfolios or models will embrace a significant allocation to bitcoin immediately – unless highly speculative return seeking is the primary goal of the strategy. The due diligence process for a novel ETF like this becomes a challenging task, perhaps challenging enough to scare potential investors away for an extended period of time. Conducting due diligence for cryptocurrencies, including bitcoin, is exceptionally tough due to the absence of a proven method for determining its intrinsic value, massive volatility, and the spotty track record of futures-based liquid ETF’s impact on retail investor’s appetite. Additionally, the global perception of cryptocurrencies as a potential threat to sovereign national security and its role as a facilitator of illegal activities adds complexity to the evaluation. As mentioned, any thorough due diligence must consider the substantial opportunity for massive volatility, as witnessed multiple times in the lifespan of bitcoin. All that being said, my long-run expectation is bitcoin will settle into a series of patterned data relationships that make portfolio allocations easier and in-line with the need for alternative models to seek lower correlations.

Oscar Skjaerpe financial planner, ProVise Management Group

We view all cryptocurrencies as speculative assets and for most clients, we would not recommend cryptocurrency since it does not fit their risk tolerance and goals. But for clients with long time horizons and aggressive risk profiles who have asked us to include bitcoin in their portfolio, we believe a 1-5% allocation would be an appropriate allocation. We always advise our clients of the inherent risk that they take when investing in this asset class.

Ron Surz president of Target Date Solutions

I’ve written -- and broadcast – about cryptocurrencies with a focus on the definition of money as (1) a store of value and (2) a means of exchange. I believe we’re in for serious inflation, despite popular opinion to the contrary, so the dollar will become a poor store of value. Gold is the traditional answer, but it is not a good means of exchange, although goldbacks (paper money with embedded gold) are a (pricey) possibility. Cryptos are a reasonable alternative to fiat currency.

So, “yes,” I do recommend bitcoin, and am comfortable doing so.

Bob Veres publisher of Inside Information

I’m writing an article on bitcoin (and crypto generally) for my next Inside Information issue. It’s a very deep rabbit hole, including the history of money, the history of banking, geopolitics, the constant flux of reserve currencies over different political regimes, etc. etc.

But the bottom line is that the responses from my readers will be: “No,” I’m not recommending any allocation to bitcoin.

Brad Wales founder of Transition to RIA

The existence of bitcoin ETFs does not automatically translate to availability of bitcoin ETFs for brokers. As is the case with leveraged or inverse products, I suspect broker/dealers will add substantial guardrails.

Rick Wedell chief investment officer at RFG Advisory.

I am firmly in the “bitcoin is heroin” frame of mind, and this isn’t the first time the SEC has approved an investment product for something that has somewhat limited utility in a traditional retirement portfolio. Certainly there are clients with specific needs and objectives where this may be appropriate, But cryptocurrency has 100% become what it sought to prevent in the first place. If you can’t appreciate the irony of the FTX fraud being driven by a currency that was supposed to be “manipulation proof,” I don’t want to be your friend. Buying on leverage, making money on an exchange, making money on the ETF – it certainly seems like the only people who are excited about bitcoin from a business perspective are the folks who are excited about how they can make money off the transactions as opposed to anyone who wants to use it to do their daily shopping. Investors should view it as a commodity from an allocation standpoint, and I have concerns about its stability and economic exchangeability. Our analysis suggests using caution and fully analyzing the risks involved in the product as well as the specific needs of the client before recommending spot bitcoin ETFs or any cryptocurrency allocation to clients, with emphasis on the speculative nature, potential for fraud, and the shifting dynamics within the cryptocurrency landscape. For context, the Matt Damon “fortune favors the brave” commercial has got to go down as one of the most unintentionally hilarious advertisements in history. We get to see Matt walk by all these different explorers who presumably have done amazing things and then we’re told to be brave! You know what history is littered with? Dead explorers! That’s not the payoff structure we recommend for a traditional retirement portfolio.

Helen Yang founder and CEO of Andes Wealth Technologies

I wouldn't recommend bitcoin ETFs to clients because bitcoin has no inherent value (see article for more). But if the client wants, it is okay for them to allocate no more than 3% of "play money" to bitcoin at their own risk.

Thomas Young economist and running for Utah State House District 40

I would recommend allocating 5-10% of a portfolio to cryptocurrencies. They offer a hedge against governments, and likely have a stronger future in transaction volume. I think a portfolio with a bitcoin ETF would be thoughtful, although owning the actual asset is a better long- term play.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more articles by Robert Huebscher