Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

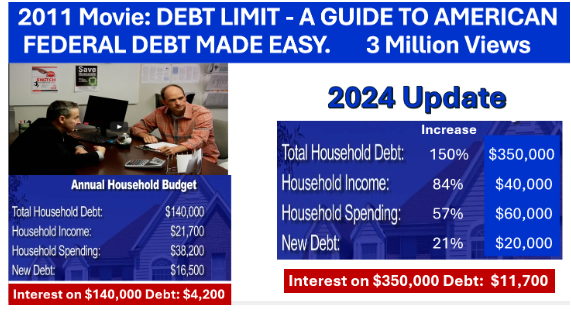

12 years ago, Debt Limit USA posted this video that has had three million viewers. Please watch this three-minute video – it’s great. Here’s a brief synopsis:

The movie opens with a borrower (a surrogate for the U.S. government) sitting across the desk from a bank loan officer, requesting a loan increase despite the fact that he is grossly overextended and has no collateral.

The loan officer denies the loan. The borrower bemoans that his baby daughter will be disappointed, to which the loan officer responds, “You have kids?” The next scene shows the baby daughter scribbling a crayon signature on a contract that obligates her to pay the loan ; she obviously represents future taxpayers.

Updating the movie to reflect 2024

If a sequel to the movie were released today, it would show the following worsening situation:

Can you imagine a bank that would lend you more money when you cannot afford even the interest on your current loan that requires one fourth of your income? Or owing nine years’ worth of your income? Something has to change.

The numbers in the movie are in fact actual government debt figures scaled back by 10 million, so for example the 2024 total household debt of $350,000 is our current $35 trillion national debt, “Household Income” is tax receipts, “Household Spending” is annual government spending, and “New Debt” is the annual government deficit of $2 trillion.

Paying the interest on our humongous debt

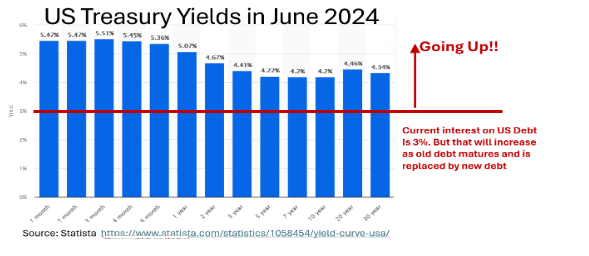

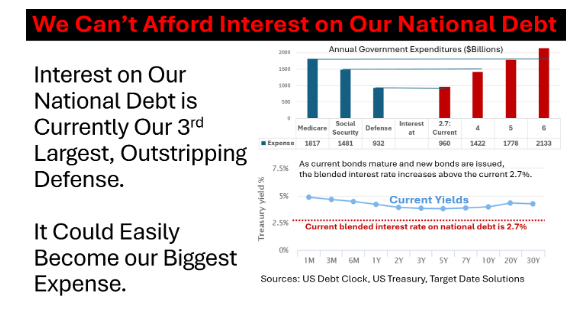

Our national debt is $35 trillion and growing by about $2 trillion per year. We don’t “feel” that number, but we do feel interest on that $35 trillion. Fortunately, for now, most of that debt is financed with old Treasury Bonds and Bills, so the current blended interest rate is a little less than 3%. At 3% interest, our current interest expense is a little under $1 trillion per year. That makes it about the same as the spending on national defense, our third largest expense, and it is getting worse.

Interest rates are currently materially higher than 3%, so interest expense on our national debt is heading higher as current Treasury loans mature and are replaced with newer loans.

This increasing interest expense will crowd out other government expenses and will become our largest expense when interest on the debt reaches 5%.

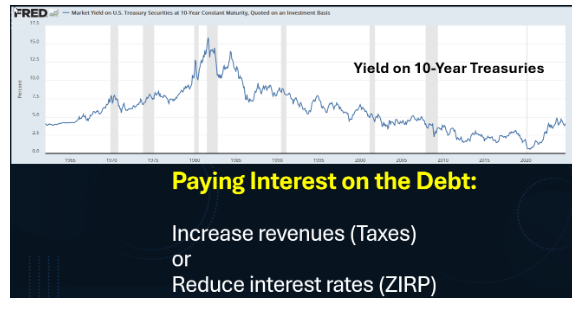

We are in a debt spiral that the Fed is dealing with by lowering interest rates in a growing economy that does not need stimulation. This decision will reignite inflation if for no other reason than the government needs to print money to suppress long term interest rates – the Fed buys the Treasury’s long-term new issues.

Even more debt

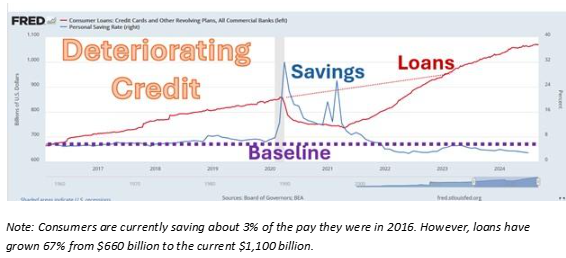

The off-balance-sheet debt for Social Security and Medicare is twice our $35 trillion official debt, and personal debt now exceeds $1 trillion. It’s incredible.

Consumers are spending more than they earn. It won’t take much longer for them to be tapped out, which will slow the growth of the economy. Perhaps that’s why the Fed is lowering rates now?

Classic inflation

It will be tempting to “monetize the debt” by printing more and more money like Argentina and Venezuela. Even resource-rich countries can experience hyperinflation. The alternatives are not politically attractive. That’s why we don’t hear the words “balance the budget.” But the U.S. is very resilient, so maybe there will be a way out. Or perhaps it will take longer than our lifetimes to get hyperinflated – then it will be the grandkids’ problem.

Conclusion

Inflation threats are real. Protect yourself with Treasury Inflation Protected Securities (TIPS), precious metals, certain real estate like farmland, and other real assets. I’d include stocks in this list, but they are extremely expensive now, perhaps because they are being bid up as an inflation hedge.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.