The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

Clients sometimes have very concentrated positions, typically from their employer or former employer in the form of vested restricted stock units (RSUs). As financial theorist William Bernstein puts it, “they have won the game” if they can diversify, since a single stock has extremely high undiversified risk. Unfortunately, the tax bill is typically huge.

Some will hold the stock until death and borrow against the concentrated stock in order to get the step-up basis. Bernstein and I wrote a joint article entitled Buy, Borrow, Die: Why This Popular Tax Strategy for the Rich Doesn’t Work. Even the largest companies, such as General Motors and Eastman Kodak, can and do go belly up and file for bankruptcy, putting a wrinkle in that strategy. Also, 96% of publicly held companies earn an average return equal to a one-month Treasury Bill.

Common Ways to Diversify

Before I explore new ways to diversify, I’ll do a brief review of common methods to diversify from a concentrated position. Let’s use a $50 million position in Nvidia (NVDA) as an example.

Sometimes a tax problem is a nice thing to have. I often recommend that the client sell some stock that has the highest cost basis. It’s rarely a binary decision, meaning the client opts to hold all or to sell all in one transaction. Often, a schedule of periodic sales to reduce exposure is recommended. If the client has charitable intent, donating the shares with the lowest cost basis to a charity or donor-advised fund (DAF) makes sense.

Another commonly used method is a Charitable Remainder Trust (CRT). An example is a Charitable Remainder Unit Trust (CRUT) under which the Nvidia stock is placed in an irrevocable trust that pays the beneficiary a fixed percentage of the trust’s value each year, with the remaining assets going to charity after the trust ends. However, I’ve analyzed this option several times and found it’s more tax-efficient to gift the most appreciated shares to the charity or DAF and then sell the shares with the highest cost basis.

Equity collars use options to manage risk. One buys a put option to set a minimum sale price (downside protection) and sells a call option to cap the potential upside gain. The premium from selling the call covers the cost of buying the put, resulting in little to no cash outflow. This doesn’t diversify but may result in downside protection for the concentrated position.

Direct indexing harvests tax losses, allowing one to sell some shares of the concentrated position. Unfortunately, in an up market, I’ve found tax losses dry up quickly and only the fees and complexities remain.

An exchange fund can also diversify. It’s a pooled investment vehicle — usually run by a financial institution — in which investors contribute concentrated stock positions and receive a diversified portfolio in return, without triggering immediate capital gains taxes. After a required seven-year holding period, investors receive a basket of more diversified securities instead of their original concentrated stock. They are typically expensive, and diversification may be limited as tech stocks generally have the largest unrealized gains due to their surge over the past decade.

Two New Ways to Diversify

There are now two new innovative methods to diversify while deferring gains.

Method 1 - Use an exchange fund as seed money for a new ETF.

The first new diversification strategy converts a concentrated position to a low-cost diversified stock ETF. It uses a combination of rule 721 (exchange fund) and section 351 (tax-free conversions) which allows investors to contribute appreciated assets into a corporation in exchange for stock without triggering capital gains taxes. I spoke to Wesley Gray, CEO of Alpha Architect who explained the rules as it relates to seed money for a new ETF.

- 50%/Top-Five Rule: The top five contributed securities cannot exceed 50% of the total portfolio’s value. (Contributed ETFs are viewed on a look through basis, so it’s the underlying holdings that are used to meet this test.)

- 25% Rule: No single security can dominate the portfolio (generally must be less than 25%), ensuring meaningful diversification.

The Alpha Architect U.S. Equity ETF (AAUS) was recently launched with some seed money using this rule and has a 0.15% expense ratio. ETF Db reports it has 275 holdings, and Morningstar shows the portfolio exhibiting characteristics similar to the S&P 500. Unfortunately, using a stock as seed money for the next Alpha Architect ETF won’t work for someone who has a single concentrated position since neither of the two rules above would likely be met by the investor.

That’s where the exchange fund comes into play. An exchange fund may not be as diversified as a broad index fund, but holds enough stocks to meet the above section 351 requirements. In other words, the top five stocks comprise less than 50% and no single stock represents more than 25% of the exchange fund’s value. Once in the ETF wrapper, the creation and redemption structure allows the manager to sell those holdings, without passing through a tax bill, to the holders of the ETF.

Gray referred me to a San Francisco based firm, Cache, which uses both the 721 code to create the exchange fund and 351 tax code to use the exchange fund as seed money for a new ETF. I spoke to Srikanth Narayan, the firm’s founder and CEO. He explained that they have exchange funds that track different indices, including one that tracks the S&P 500. Every two weeks, the fund, structured as a partnership, opens up to new limited partners contributing their concentrated positions.

Narayan noted that they structure the exchange fund’s portfolio to have similar characteristics to the S&P 500, but would also complete the portfolio using some of the exchange fund’s holdings as seed money for the creation of new ETFs like Alpha Architect’s AAUS, which is one of their 11 ETFs totaling over $12 billion in assets. Cache has no ETFs of their own. Cache’s annual fees range from 0.95% for $100,000 minimum down to 0.40% for amounts over $25 million.

After seven years, one can exit the partnership, still deferring taxes, taking their share of the underlying positions of individual stocks and the new low-cost and diversified ETFs. Narayan stated that the goal is not to have all ETFs, so risks include tracking error of the underlying positions of individual stocks and ETFs to the S&P 500. Admittedly, the 10 most valuable U.S. companies comprise 47% of the S&P 500, so it’s not as diversified as it used to be. Narayan used the Cache exchange fund himself to diversify out of a stock concentration in Uber, a previous employer.

Method 2: Direct Equity Active Long Short (DEALS)

This strategy uses an SMA (separately managed account) structure combining a concentrated stock with a market neutral long-short strategy. It can be thought of as direct indexing on steroids. In the example, the $50 million of Nvidia is used as collateral for a long-short strategy that may hold, for example, 130% long and 30% short positions. As such, the account would have $50 million of Nvidia, $15 million of diversified long positions, and $15 million of diversified short positions.

Unlike traditional direct indexing, the tax-loss harvesting continues even in an up market, since the short positions continue to generate losses that would hopefully be matched by gains. For example, the SMA could short ExxonMobil and hold Chevron long. As the losses are recognized, the Nvidia shares with the highest cost basis would be sold.

Two firms that offer this strategy are Quantinno and AQR. A paper on AQR’s website estimates a 100% tax loss (allowing for the sale of all Nvidia stock) could be recognized over seven years using a 150% (150% long and 50% short) strategy. I spoke with Hoon Kim, Quantinno’s founder and CEO, who estimated a 130% strategy would take about nine years to fully liquidate a concentrated position with a near zero cost basis, depending upon market conditions. He said Quantinno’s fees typically run about 0.50% annually. In addition to the management fees, there are financing costs for both margin and shorting, as well as trading costs of the underlying positions.

One downside of this strategy is that, unlike method one, it will take several years to diversify. Should Nvidia stock plunge, the margins could be called and Nvidia stock could be sold. The 50% short strategy in the previous paragraph seems risky to me. I’d prefer the 30% short strategy. Fees, of course, are another downside. Finally, any position that is shorted theoretically has the potential for unlimited losses since any one stock could skyrocket. But, like any SMA, one should be able to exit, taking the positions with them, at any time.

Conclusion

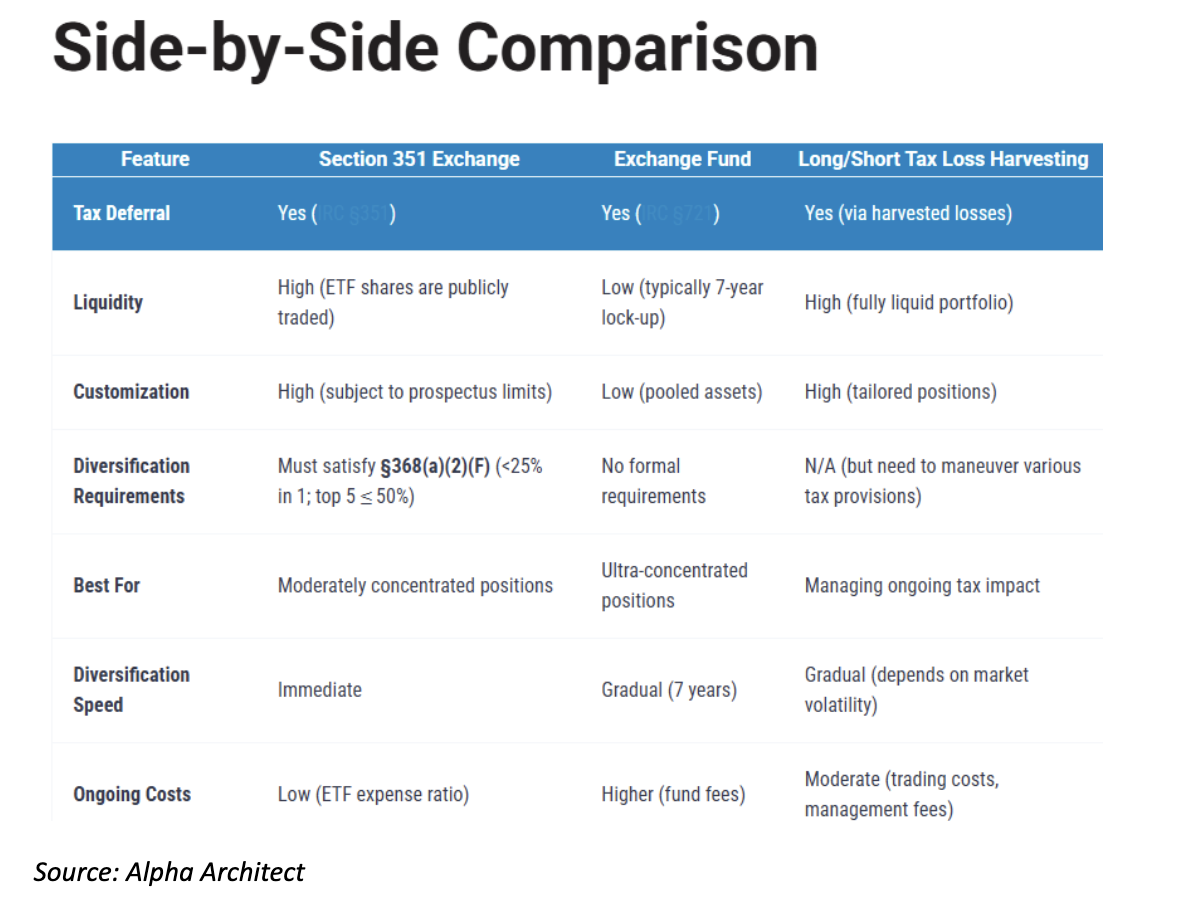

I’ve always said investing is simple but I never said taxes were. Both of these new methods are brilliant but not without risk, including the possibility of being challenged by the IRS. That’s an argument to perhaps use a combination of both of the new methods if the IRS challenges one. Alpha Architect summarizes the strategies below, with method one being a combination of the exchange fund and section 351.

My advice is to read the fine print and understand the total costs, risks, and exit strategies. I’ve merely scratched the surface on the complexities. Both strategies only defer the taxes, and capital gain tax rates could be higher in the future. Death is the only way to escape paying taxes, and even the law allowing a step-up basis to heirs could change.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.